In September, the S&P 500 logged its worst performance since 2002. And after further pain to start October, stocks touched on a two-year low.

Many investors are convinced that the worst will be over soon, and then they can get right back to the business of reaping 25% to 50% a year in Big Tech stocks the way they used to in the good ol’ days.

Fat chance.

The sheer volume of naïve investors out there, full of excuses and wide-eyed optimism about the market, is staggering.

They say the war in Ukraine that began last winter was a once-in-generation conflict, and it’s only a matter of time before Big Tech comes roaring back…

They shrug at 500-point declines in the Dow, pointing out that at least things aren’t as grim as they were during the financial crisis or the dot-com crash…

And when all else fails, they point out that, hey, at least we aren’t living through another Great Depression.

When did people just stop caring about a 30% crash in the markets? Did their brains just short out after seeing too much red ink in their portfolio statements, or did they just stop paying attention?

It’s true that markets never move higher in a straight line. And yes, every portfolio has its periods of red ink.

But bubbles, busts and crashes are not acceptable. They are not simply the “price of doing business.”

I refuse to accept those kinds of losses – ever.

And you should, too.

Move Beyond Boom, Bubble and Bust

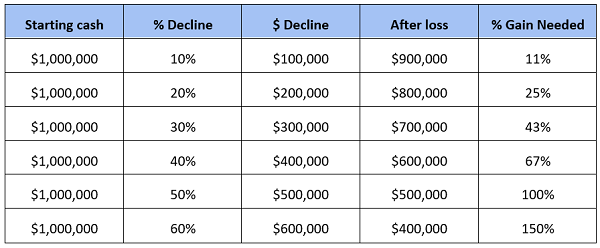

Here’s a hard reality about investing, which sounds strange to many people until they see the math… a 50% loss by a 50% gain doesn’t get you back to break-even. In fact, it can leave you significantly behind.

If you doubt the truth of this, consider the following math: If you have a $1 million portfolio and lose 50%, you wind up at $500,000 in total value after the decline. And if you then experience 50% profits after arriving at this low point, you make back just $250,000 – for a grand total of $750,000, not $1 million.

That leaves you $250,000 short. Hardly break-even, is it?

It seems odd, but it’s the cold, hard logic of numbers at work here. The deeper your declines, the bigger the gains you need to recover.

I don’t know about you, but I have no interest in ever being in a position where I need 100% or 150% gains just to get back to where I started. Those kinds of returns are possible, but they certainly aren’t probable.

So I refuse to participate in the fashionable trades that are part of the boom, bubble and bust cycle. Instead, I focus on stable companies that will last. I rely on a portfolio that doesn’t depend on best-case scenario returns to offset the natural losses of high-risk investments. Instead, it is designed to perform well even if the worst case scenario comes to pass.

And that’s exactly the kind of investing investors like you should be doing right now, too.

You should be positioning yourself in defensive stocks that will deliver consistently for years to come – a low-risk, income-rich strategy for the long haul.

And you should stick with it, regardless of whatever fancy IPOs and fintech spinoffs and biotechnology start-ups are on everyone’s lips over at CNBC.

Defensive is not flat – it’s 10% to 15% in consistent annual profits

Most investors intellectually understand the importance of low-cost, defensive strategies.

They just get distracted by the latest flashy fads along the way.

They know that active managers who quickly turn over their portfolio wind up doing more harm than good and racking up high fees in the process. And they know that diversification across sectors and geographies is an important way to smooth out any potential bumps in the road to retirement.

Dangle a high-flying tech stock in front of them, though, and many folks just can’t resist.

But being defensive doesn’t mean you have to settle for 1% or 2% annual returns. You can invest responsibly and with an eye towards capital preservation but still harvest 10% or 15% a year – or more!

That’s the approach I use in my personal portfolio, and the approach we embrace with our Hidden Yields advisory service. We use a quantitative and qualitative approach to analyze the relationships between dividends and price performance to return 15%+ returns per year from conservative, crash-proof investments.

That may not sound like a lot, compared with stocks that are supposed to deliver 100%, 200% or 300% annual return… but I promise you that these returns are a heck of a lot more consistent, without the big-time declines that come from chasing aggressive tech stocks.

And besides, if you invested $100,000 in our strategy and realized 15% gains for 15 years… you’d turn that nest egg into more than $900,000 when all is said and done.

Or put another way… That’s enough to double your portfolio’s value every five years!

Wall Street may look bleak right now, but this elite portfolio of recession-proof dividend stocks isn’t just surviving—its positioned to thrive for the rest of 2022, into 2023 and beyond!

To be clear, these aren’t your garden variety tech stocks. These are niche midcaps and downright boring S&P 500 components that you’ve never heard of.

And that’s the point.

These “Hidden Yield stocks” offer investors a port in the storm amid current stock market volatility, and significant total returns when you add up their share performance and consistent dividends.

This rock-solid portfolio is built on three core pillars:

Pillar #1: Consistent Dividend Hikes

Pillar #2: Lagging Stock Price

Pillar #3: Stock Buybacks

Selecting companies with a proven track record of stability is the safest, most reliable way to get rich in the stock market. While other investors are chasing the boom, bubble and bust cycle… you’ll be harvesting consistent double-digit returns to provide you peace of mind as well as big-time profits!

Let us show you how it’s done. Click here to get a copy of our 7 Recession-Proof Dividend Stocks With 100% Upside, including full analyses of each pick … and a few other bonuses, too!

Recent Comments