Look, I know it’s heartbreaking to invest in this dumpster-fire market. Heck, even if you do everything right and only buy top-quality dividend stocks, they still seem to plunge a day (or two at most!) later.

This is why, in last Tuesday’s article (the first in a series on how my proven “Dividend Magnet” plan can boost your returns), I urged folks to keep a healthy cash pile to invest on the other side of this crash—and that time will come! I’ll tell you when we’ll fully deploy our hoard in my Hidden Yields dividend-growth service.

Meantime, we’ll continue to trade lightly—buying only in small lots and only for the long haul. But for the cash we do deploy today, what exactly should we be looking for?

Beyond P/E Ratios

One thing we do not want to do is put too much stock (sorry, I couldn’t resist!) in the one measure that’s practically a religion to many folks: the price-to-earnings (P/E) ratio. Many investors look for a stock with a P/E they think is “cheap”—below 10 or whatever.

And in this mess of a market, sub-10 P/Es abound!

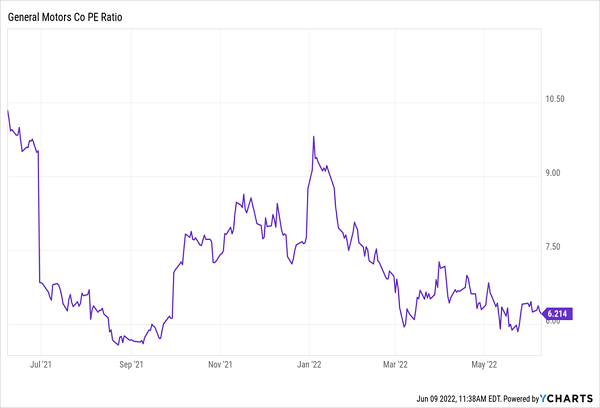

Trouble is, a “cheap” stock can always get cheaper. Consider General Motors (GM), which always boasts a tempting P/E. A year ago, you could’ve picked it up at 10-times earnings. An incredible deal on a legacy American company, right?

Sure. Except today its P/E has fallen to a dismal six (six!) times earnings.

GM Shows a Cheap Stock Can Always Get Cheaper

Do I hear three?

Look, I’m not saying you should throw P/Es out—not by a longshot. But we need to bear in mind that they are just one piece of the puzzle. Another, more important, predictor of share-price growth is one that few people pay attention to: dividend growth.

I know that sounds weird. Most folks see dividends and stock prices as independent of one another. Worse, many ignore dividends altogether (the meager 1.5% yield on the typical S&P 500 stock is the main reason why—especially with inflation roaring north of 8%).

But as Hidden Yields members know, the current yield is pretty much useless to us on its own. Far more important are: 1) Whether you reinvest your payouts over the long haul, and 2) The rate of payout growth, which is tied into the share-price gains I mentioned a second ago.

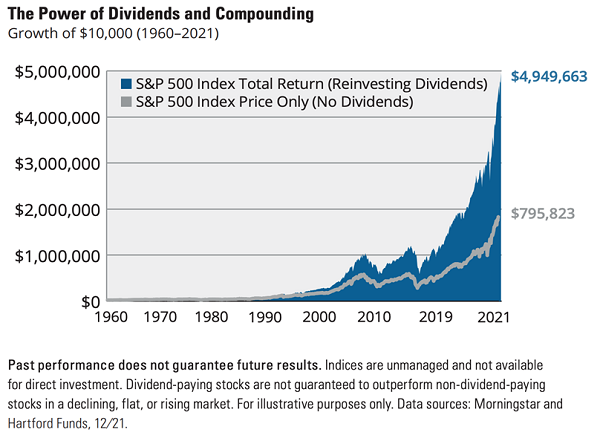

Dividend Reinvestment Can Deliver Millions More in Gains and Payouts

We’ll dive into that dividend-growth/share-price relationship shortly. First, a quick aside on dividend reinvestment. Because if you roll your dividends back into your portfolio (perhaps through an automatic dividend reinvestment plan, or DRIP), the power of compounding kicks in.

When I say “power,” I’m not kidding. Hartford Funds looked at the 60 years between 1960 and 2021 and found something shocking: an investor who put $10,000 into the S&P 500 back then would have $795,823 at the end of the period, based solely on price gains.

That’s not bad: a 7,858% increase. But if they’d reinvested their dividends, the magic of compounding would have left them with $4,949,663, or nearly $4.2 million more!

Most folks stop here when thinking about dividends and stock returns (if they even get this far!). But they shouldn’t, because it’s just Act 1. You can position yourself for even stronger profits if you buy stocks whose dividends are not only growing but accelerating.

The relationship between fast-growing dividends and share prices powers my “Dividend Magnet” strategy, which is the secret behind the gains we’ve seen in Hidden Yields.

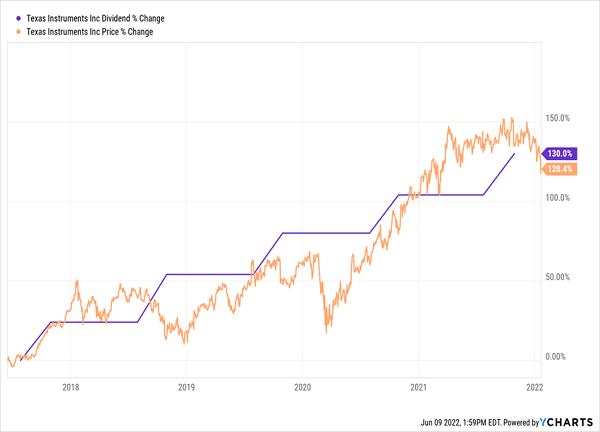

TXN’s “Accelerating” Dividend Powered Us to a 148% Return

To see what I’m getting at, consider Texas Instruments (TXN), whose dividend soared 120% when we held it from June 2017 until early-2022, or just under five years, bagging a 148% total return (with dividends reinvested) in the process.

You can clearly see TXN’s Dividend Magnet going to work on its share price, point for point:

TXN’s Dividend Magnet Fires Up

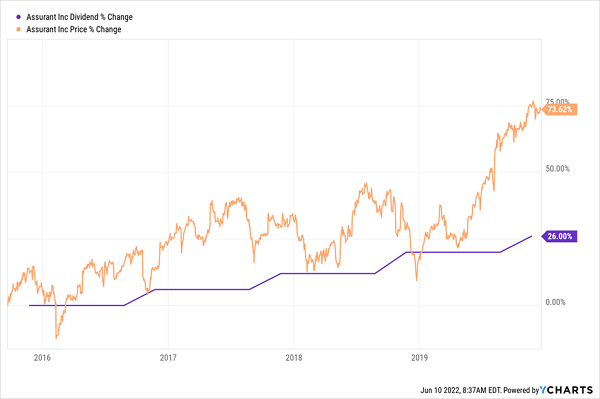

You can also see this pattern in the return of insurer Assurant (AIZ), which we Hidden Yielders held from September 2015 until December 2019. The stock returned 92% (with dividends reinvested), and you can see how the rising dividend threw a floor under the share price, and ultimately drove it higher:

Assurant’s Dividend Secures Its Share Price—Then Sends It Soaring

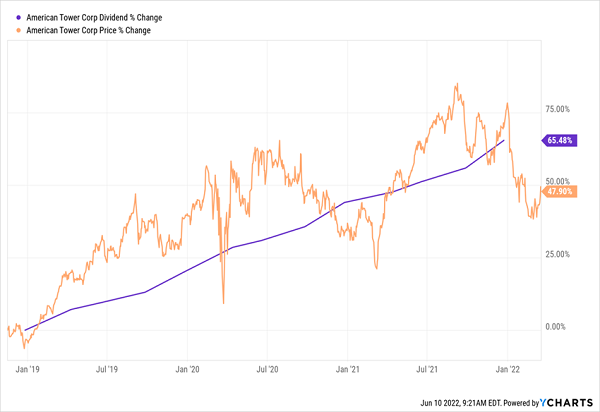

Then there’s American Tower (AMT), which we touched on in last week’s article. It’s a cell-tower “landlord” whose “tenants” include the biggest names in the space: AT&T (T) and Verizon (VZ) among them. AMT generates so much free cash flow that it raises its dividend every quarter!

We love a management team with that much swagger, so we bought in November 2018 (the last time the market sold off in a rate-driven panic) and rode AMT’s strengthening Dividend Magnet right through the COVID crisis, bagging a 57% total return, powered by 65% payout growth.

Here’s what the price-and-dividend action looked like. Again, our dividend-up, share-price-up pattern is glaringly evident:

American Tower’s Dividend Magnet Pulls Its Share Price Up

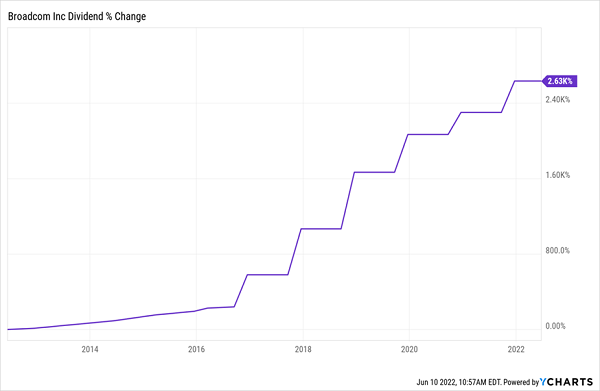

There’s an added benefit to my Dividend Magnet strategy, too: it is hands-down the safest way to build a huge yield over time. To see what I mean, consider semiconductor play Broadcom (AVGO), which grew its dividend an incredible 2,630% in the last decade.

Broadcom’s Dividend Soars 4 Digits—and Yields a Ridiculous 48%

Buying then would have fetched you a 1.3% current yield; the stock yields a little more than double that, 2.8%, today. That’s obviously much better, but it’s still pretty unexciting to us dividend fans. But get this: thanks to Broadcom’s ridiculous dividend growth, you’d be yielding an astonishing 48% on your initial buy today!

(Note that this is the second article in our series on how my “Dividend Magnet” powers share prices and dividend payouts. In two weeks, we’ll look at how you can use this proven approach to protect yourself from potential dividend—and share price!—cuts.)

7 Crash-Resistant “Dividend Magnets” That Are Absolute Must-Buys Now

As we discussed, any stock you buy in this grass-fire market must have a healthy—and growing—dividend, to set you up for gains and give you downside protection, too.

That’s because stocks with growing dividends tend to hold on to their shareholders through a crisis and bounce back fastest when the dust settles.

I’ve got 7 of these stocks that absolutely must be on your radar today. Thanks to their powerful Dividend Magnets, I’ve hand-picked them to deliver 15% annualized total returns in the long run. I want to share them with you now.

I also want to set you up with a 60-day no-risk trial to Hidden Yields, so I can help guide you through this market mess and over to the other side, with help from the most reliable—and fastest-growing—dividends out there.

Recent Comments