Real estate is getting thumped, which means real estate investment trusts (REITs) are a bargain once again.

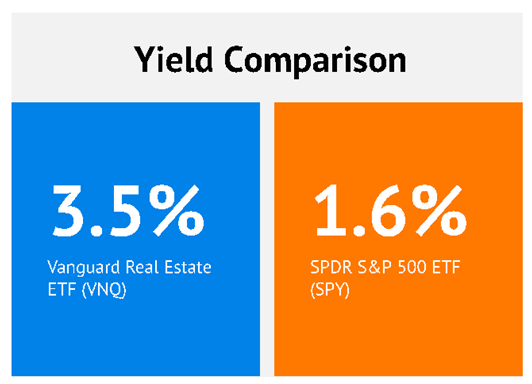

Finally! REIT yields are back to where they ought to be—(land)lording over the vanilla S&P 500:

We contrarians, of course, can do even better than the popular Vanguard Real Estate ETF (VNQ). While 3.5% isn’t bad, it pales in comparison to the 12.7% “headline yield” we’re about to discuss.

Why are REITs cheap again? Simple: The Fed.

As I mentioned months ago, higher interest rates mean not only higher costs of capital for REITs (and all other companies, for that matter), but also more competition for income as bond yields become increasingly competitive.

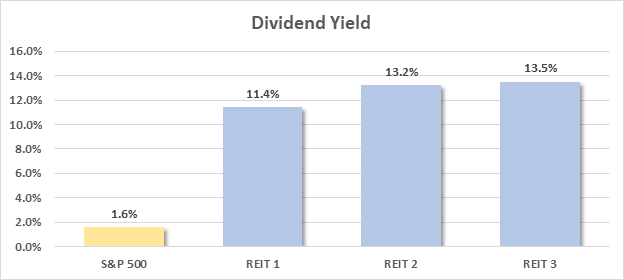

REITs have, indeed, behaved exactly as we expected:

Interest Rates Up, Real Estate Down

Big picture, though, we’ll look back at this period as one of the best times to buy REITs at cheaper prices and much higher-than-average yields.

Where should we start? Let’s discuss that three-pack of REITs, yielding 11.4% to 13.5%.

Necessity Retail REIT (RTL)

Dividend Yield: 13.5%

I have a bit of a soft spot for Getty Realty (GTY), a single-tenant specialist that fits the “boring is beautiful” mold by leasing out its properties to what I’d call “necessity” retailers: gas stations, convenience stores, auto-parts shops, you get the picture.

Given that, I’d have to love a real estate firm that calls itself Necessity Retail REIT (RTL), right?

Necessity Retail owns more than 1,000 single-tenant and “open-air power, anchored and grocery centers” in 48 states that are net-leased on primarily long-term deals. Its tenants come from 44 different industries—including gas/convenience, healthcare, and quick-service restaurants—with no one industry comprising more than 8% of straight-line rents.

Why does such a large REIT sound so unfamiliar? Well, only a year ago, it changed its name from American Finance Trust (AFIN)—a name I explored in 2020. I noted that its heavy exposure to restaurants, entertainment, retailers, and office properties a “liability” amid COVID, but that it could end up looking like a bargain buy because of the potential of a COVID recovery snap-back.

RTL Got That Snap-Back, But It Didn’t Last

Fast-forward to today, and RTL has a much different problem—namely, debt.

Near the end of 2021, it announced a $1.3 billion acquisition of 81 retail assets from CIM Real Estate Finance Trust, as well as the divestiture of three non-core office assets.

The good news? RTL lowered its top-10-tenant concentration and reduced its exposure to office space from 7% to 1%. The downside? A big debt burden only got bigger. This REIT now has $2.8 billion in net debt, which is nearly 10 times its adjusted EBITDA and more than three times its market cap!

For what it’s worth, dividend coverage here isn’t a glaring concern, with the dividend representing just 83% of trailing 12-month adjusted funds from operations (FFO). But the high debt load and lack of obvious catalysts do give me a bit of pause about RTL.

Global Net Lease (GNL)

Dividend Yield: 11.4%

Global Net Lease (GNL) is a commercial REIT that, as the “Global” in its name would imply, operates not just here in the U.S., but in 10 other countries, including the U.K., Netherlands, Finland and France. It owns 311 properties leased out to 140 tenants in 50 industries, though industry concentration is a little higher—financial services (13%) and auto manufacturing (12%) are both double-digit slices of the portfolio pie.

The other part of its name is “Net Lease,” which, like with RTL, is a reason to like it. Net leases, as a reminder, are “net” of insurance, maintenance and taxes, meaning it just collects rent and leaves everything else to the tenants to figure out. That means fewer variables for GNL investors to worry about; profits are more predictable and reliable than they would be with traditional leases.

So, what’s wrong with GNL?

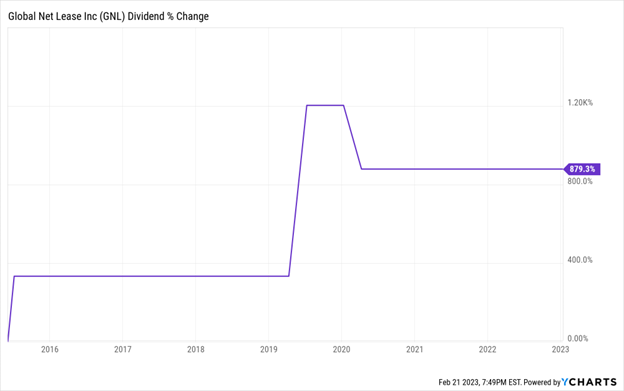

For starters, Global Net Lease was among the many REITs that cut into their dividends because of COVID. Specifically, the company cut its payout by 25% to 40 cents per share in April 2020, and it hasn’t looked back.

GNL’s 2019 Hike Was Short-Lived

If there’s any upside to the cut, it’s that the current payout is more sustainable. The AFFO payout ratio is 93%, which is secure enough but bears will be watching closely in coming months.

Also, like Necessity Retail, GNL has pretty high debt of $2.2 billion. It’s not as bad, at least comparatively—it’s 8x adjusted EBITDA and 1.5x its market cap. And the weighted average interest rate it’s paying on that debt (3.5%) is a little better than RTL’s (4.2%).

So, Global Net Lease certainly has its warts. But for more aggressive dividend investors, GNL—which is a rare multinational real estate play that’s trading at attractive levels compared to both its AFFO and adjusted EBITDA—might fit the bill.

Office Properties Income Trust (OPI)

Dividend Yield: 13.2%

Sometimes, even the worst-looking situations can bear profitable fruit.

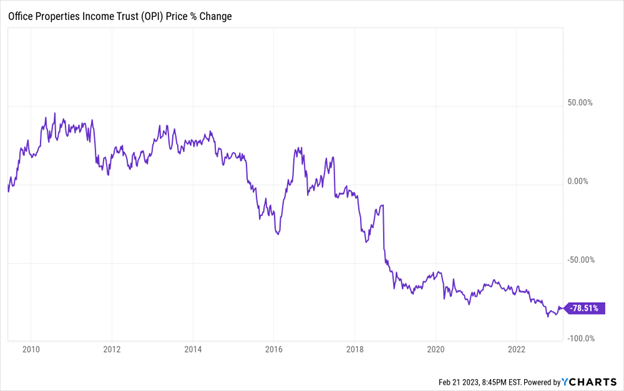

Take Office Properties Income Trust (OPI), for example. This REIT owns 160 properties that it primarily leases out to high-credit-quality single tenants—not just businesses, but also government entities. And back when I reviewed it in October 2022, it was mired in a decade-long decline that had really sped up of late—OPI shares had been cut nearly in half.

But as difficult as it is being an office-property landlord in these WFH times, OPI isn’t without its merits. And at the time, I mused that “perhaps the market is overselling OPI.”

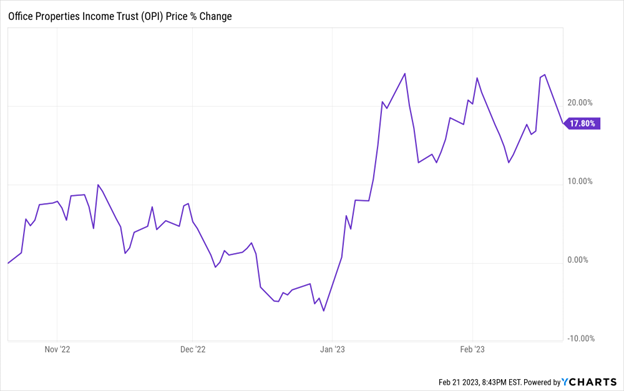

Indeed It Was.

Let’s be clear: OPI is fighting an uphill battle that began long before COVID.

The “Decline of the Office” Isn’t a New Phenomenon

The terms “WFH,” “remote work” and “telecommuting” might have hit the mainstream in 2020, but corporate America had been tilting more toward flexible work situations for years—COVID merely gave the trend a polite shove.

Still, betting against Office Properties Income Trust, at least right now, could be dangerous. While it has clawed back nearly 20% of its value over the past few months, the stock is still extremely cheap, at just five times CAD (cash available for distribution, an alternative profitability metric for some REITs). If you want to use a more traditional REIT metric, OPI trades at less than 4x its normalized FFO.

Moreover, OPI isn’t some New York City-based REIT that’s hemorrhaging tenants. It’s more suburban-based, with a current occupancy of 96%. Fully a third of its tenants are governmental entities or contractors—the kinds of tenants that are glued to their offices. And after a couple years of offering no-holds-barred flexibility, many employers are finally starting to push back and demanding workers spend a few days back in the office.

Your 2023 Guide to Retirement Riches: 7%-Yielding Blue Chips That Pay EVERY MONTH

However, I wouldn’t bet on OPI, either—at least not as a long-term retirement holding.

Yes, the dividend is high and the valuation is low. And for now, employers are pushing back in the other direction. But Office Properties Income Trust is swimming upstream against a formidable mega-trend making it near impossible to flourish in this industry, no matter how skilled OPI’s management might be.

That simply won’t cut it if we want to enjoy fat dividends and respectable share-price gains well into retirement.

For that, we need the “A” squad: diversified, reliable payers of mouth watering yet dependable income—preferably, those that don’t knuckle under every time the economy throws a fit.

And you can find these rare monthly dividend blue chips in my “7% Monthly Payer Portfolio.”

Many of the recommendations in my “7% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate massive yields, while also fostering the potential to generate aggressive price performance.

These dividends aren’t good. They’re not even great. They’re retirement-sustaining, all on their own.

Do the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $35,000 annual income stream.

That’s nearly $3,000 each month in regular income checks!

Even better? The current bear market has provided us with a rare gift, pulling many of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to learn everything you need about these generous monthly dividend payers right now!

Recent Comments