We’re heading towards the most telegraphed recession of all time. At least in recent memory.

So should we sell everything? Not exactly. Granted, recessions are usually bad for stocks. Vanilla investors who own nothing-but-ETFs are in a tough spot.

But since you’re reading this, I assume:

- You pick stocks better than a robotic ETF.

- You’re not scared of a stinkin’ recession. You’re here looking for high-yield exceptions to the “sell everything” rule.

I appreciate that about you, my fellow contrarian. If I thought rules applied to me, I would have made it past age 26 in Corporate America! This is why we get along so well.

So, let’s talk recession-resistant exceptions. There are dividend stocks that should skate through a slowdown just fine, but also others that should have been sold last week!

First, the backdrop. When the economy slows, interest rates fall. This can be quite bullish for dividend stocks. Especially “safe havens” like utilities and even select real estate investment trusts (REITs). Really, anything safe that pays.

High-paying cash equivalents and bonds are competition for dividend stocks like REITs. When investors can get 4% in a money market fund, they are less inclined to reach for Vanguard Real Estate (VNQ), which yields 3.7% today.

But if the economy tanks and rates go back down to 1%? Then VNQ’s dividend is going to look pretty sweet.

Provided that its constituents can hold up in a recession. Some can, but some can’t.

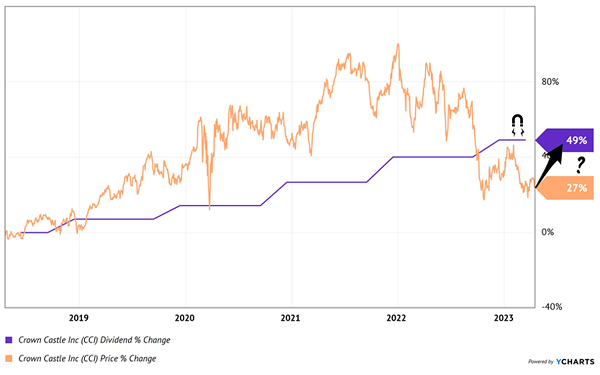

Last week we highlighted Crown Castle (CCI), VNQ’s fifth largest holding, as a REIT likely to roll through a recession. The cell-tower operator is a landlord for mobile phone traffic, collecting rents via its 40,000 towers (from carriers such as AT&T and Verizon). It’s one of the three major cell-tower landlords in America.

While consumers cut back during recessions, the last bill that will go unpaid will be the cell phone bill!

CCI has hiked its dividend by a dynamic 49% over the past five years. The company is basically a “growth utility” stock in that it’s a toll booth for cell phone traffic. CCI builds the cell towers and then rents them out—a business that turns from capital intensive to cash cow over time.

The stock rarely yields this much (4.8%) and rarely trades below its dividend line. But today, we find ourselves on the profitable underside of the magnet:

CCI Will Sail as Rates Cool

This is exactly the type of recession-proof bargain we want to buy now!

Office REITs, on the other hand, we should generally avoid. It’s a terrible time to be a commercial landlord, to say the least.

Nobody wants your Class A office space, bro. We all work from our kitchen tables. Still.

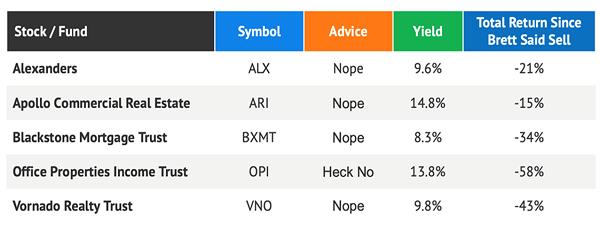

Last August, I wrote to you asking that we avoid five office space peddlers.

Let’s not be fooled by these placid-on-paper book values. The book is stale. These stocks are sicker than they look.

They sure were! Look at the deep red since:

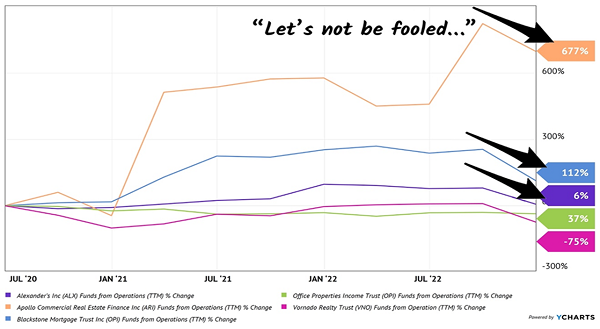

Sweet crystal ball, huh? Well, when it comes to REITs, forecasting is straightforward. Funds from operations (FFO) drive dividends—for better or for worse. When FFO is climbing, it’s all good. When FFO is about to drop, avoid!

Hence the timeliness of my warning last summer. FFO was fine until it wasn’t for these five landlords. Common sense was our edge!

The Common Sense Crystal Ball

These yields have climbed even higher because, well, the stock prices have plummeted because the dividend payments are not sustainable. Avoid!

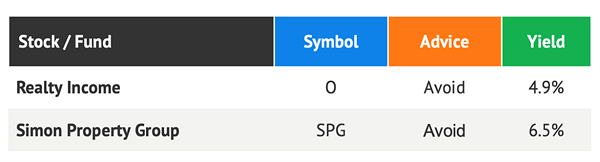

Retail REITs are dicey too. VNQ’s sixth and seventh largest holdings are Realty Income (O) and Simon Property Group (SPG). They lease brick and mortar buildings for the purpose of shopping.

That’s right. In-person shopping. (Crowd groans)

Granted, not as dead an activity as going to an office. Retail will be around for a while. But landlording over it is not a business I would choose.

So sure, the 4.9% and 6.5% headline yields on O and SPG respectively attract attention. And O pays its dividends monthly, which earns the stock brownie points with dividend investors. (In fact, they call themselves “The Monthly Dividend Company.” Great marketing, sure, but read on—don’t buy the stock.)

These two stocks are still growing FFO. So what gives?

I’m worried this “dividend disaster duo” boasts cash flow on the edge of a cliff. Today, they sit where our office REITs were perched late last summer.

These payout engines have stalled. Brick and mortar retail? C’mon man. This is not a growth business. It’s stagnant at best but likely to be worse in the near-term as people cut back their spending.

Yes, retail REITs have staged an admirable comeback since 2020. But the party is about to stop. Avoid O, SPG and the rest of their ilk. And VNQ, because its human handlers don’t consider second-level analysis like this!

Retail buying slows during slowdowns. This is what always happens. So, let’s avoid these stocks! And choose recession-resistant REITs instead.

And we have plenty of monthly dividend payers that fit this bill. No need to reach for O when we have these 7%+ yields that get paid every 30 days!

Recent Comments