The market looks like it’s about to fall apart. Which means we contrarians will step in, and smartly bank more dividend for our dollar.

Some of us park our dry powder in cash. Others stash in conservative bond funds to juice a bit more yield out of our savings. Let’s talk about these bonds because this is an ideal time to say goodbye to them (for a while!)

As dividend investors, we are naturally allergic to cash. After all, why leave money in dollars earning nothing when we can move it to a stock or fund yielding something?

As I write our Contrarian Income Report portfolio yields 6.3%. And our ten biggest payers dish 7.6% dividends. Both numbers are certainly better than zero.

New subscribers who are actively deploying funds into our CIR (or Hidden Yields, or Dividend Swing Trader) dread a 0% yield on capital. So, we naturally hear from folk who want a safe place to park cash and earn something.

From time to time, we’ll chat here about funds like the iShares Core US Aggregate Bond ETF (AGG). It is the bellwether ETF of fixed income, the easiest way to buy a basket of safe bonds.

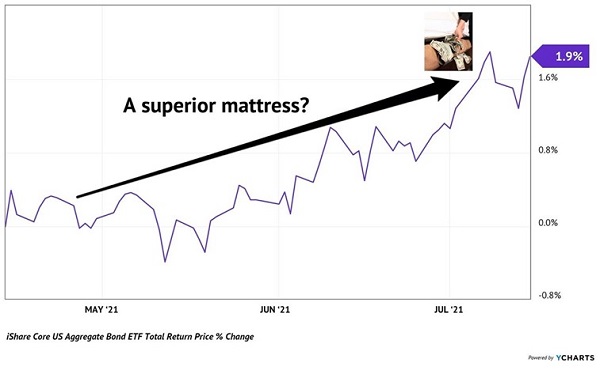

As I write, AGG yields 1.3%. Not much, but better than the proverbial mattress.

Plus, over the past three months, AGG has delivered 1.9% total returns (including dividends). That annualizes to about 8%, which is certainly better than no-yield cash:

AGG’s Been Better Than Nothing

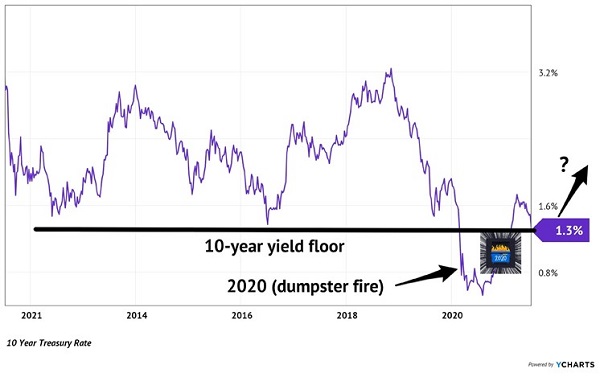

However, there’s a reason for the outperformance. The 10-year Treasury rate declined from 1.6% to 1.2% during this three-month span.

As the 10-year yield lowered, the bonds in AGG’s portfolio became more valuable. This has recently been a nice tailwind for many bond funds—especially low yielding varieties. Problem is, the winds will quickly flip if rates rise!

And we’re at a natural place for the winds to reverse. We may have reached a near-term “floor” for the 10-year yield.

Exactly five years ago, the 10-year yield bottomed at the levels we saw last week. For the past decade, in fact, 1.3% served as a reliable floor. Last year was the exception, but hey, when wasn’t last year the exception? My bet is that the floor holds, and we see a bounce in yields:

A Likely Place for a Rate Bounce

(As we went to print, the 10-year yield has dipped to 1.2%. This short-term move does not negate the presence of this long-term floor.)

The consumer price index (CPI) is up 5.4% year-over-year. And this number is probably understated because it doesn’t include housing prices, which have soared 24% over the past year!

With 5.4% inflation and a 1.2% 10-year rate, something has to give. Which is another reason I’m expecting real yields to rise. If and when this happens, anyone holding the Vanguard Intermediate-Term Bond ETF (BIV) will wish they sold when they read this. BIV holds US government debt and similar types of high-quality fixed income. It’s a big liquid fund that yields 1.5% today.

On the surface, 1.5% is more than 0%. But this modest yield comes with risk. If the 10-year rate reverses course, as I’m expecting it to, then BIV’s portfolio will lose some value.

Now, it’s not going to get crushed. Year-to-date the 10-year yield is 40% higher, and AGG and BIV are only down 1%. That’s not bad, but -1% is less than zero, which cash “earned.”

So, with the 10-year yield at a multi-year floor, I don’t think it’s worth reaching for cash alternatives. Keep the cash under the mattress until it’s “go time.”

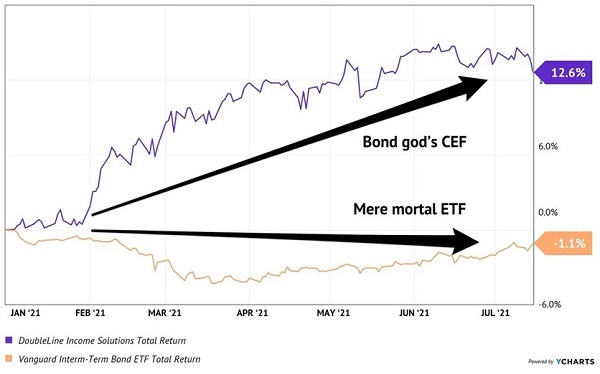

A better bond bet—whether rates are rising, falling or grinding sideways—is the DoubleLine Income Solutions Fund (DSL). It has several major advantages over an ETF.

First, the fund pays a juicy 7.5% today. The 10-year yield could double and it would still be no competition for the DoubleLine fund.

Second, DSL is managed by the “bond god” Jeffrey Gundlach and his all-star fixed income team. He’s called that because Gundlach took the bond crown from Bill Gross many years ago thanks to consistent outperformance.

His team at DoubleLine scours the world for the best bond deals. No wonder three of their top five holdings are overseas offerings that we mere mortals can’t access. Oh—and they have coupons above 7%!

Third, when we entrust our capital with the bond god, we are able to do so at a discount to net asset value (NAV). As I write, DSL trades at a 3% discount to NAV. Why? No idea. But I’m happy to buy world-class expertise for 97 cents on the dollar.

DSL has crushed the likes of BIV year-to-date, returning 12.6% to BIV’s -1.1%. I expect the outperformance to continue, regardless of where rates go.

When We Were Bond Gods

In fact, during an inflation retirement storm—like the one that is brewing right now—we need to avoid these types of bond funds altogether. This is a 50-year financial event, driven by the Federal Reserve’s unprecedented money printing, and quite honestly it is setting up the biggest retirement disaster in history.

Yields are at all-time lows while inflation is running as hot as it has since the 1970s. This is a brutal “stagflation” combination. Not only is it challenging to find income, but keeping capital growing ahead of inflation is a double whammy!

The real—and only—income answer is to start collecting monthly dividends that add up to 6%, 8% or more every year. While, of course, protecting your nest egg against soaring prices. Click here and I’ll share my favorite inflation dividend investments.

Recent Comments