Has this market gone too far, too fast? Is another crash coming? And what the heck should we be buying now?

I’ll dive into all three questions today, and I think my answer to that last one will intrigue you: it’s a tech-focused closed-end fund (CEF) paying a growing 7% dividend! This under-the-radar fund also employs an unusual strategy that hedges its downside if we do get another pullback.

The One Number to Watch Now

Let’s start with where I see the market headed from here.

At its worst point in this latest crash, the S&P 500 lost about 30% of its value, and it did so in less than a month, only to begin recovering a few weeks later.

Why 30%? Why not 80%, 60% or any other number? To answer that, we have to first keep in mind how stocks are priced: the price-to-earnings (P/E) ratio. The idea is that you pay a certain price for stocks relative to the total earnings those stocks earn through their operations. Go back in history and we see how this number can change.

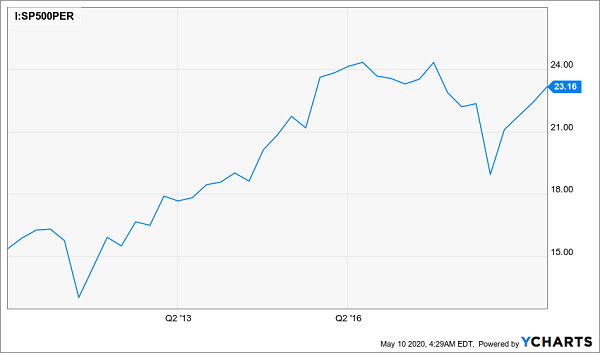

The Ebbs and Flows of the P/E Ratio

Over the last decade, the stock market’s P/E ratio has steadily risen because of two phenomena. First, companies have been able to increase earnings through a variety of cost-cutting measures. Second, and more important, the market has become more tech-heavy and less reliant on legacy companies like Exxon (XOM), whose earnings potential is limited because we’ve had an oil glut.

As the S&P 500 becomes more weighted to tech and valuations rise, the baseline P/E ratio for a fairly valued market rises, as well. This is bullish in normal times, but it’s even more bullish in the pandemic, where the world is more dependent on technology. It’s also why the tech-heavy NASDAQ 100–tracking Invesco QQQ Trust (QQQ) is up year to date.

Tech Still Rising

But that leads us to an important question: is tech now too expensive? Are stocks in general too expensive, too, if this lockdown keeps economic growth down for longer?

Valuing Stocks in a Lockdown

At first, that 30% drop in stock prices was the result of sheer panic. But it stopped at 30% for a simple reason that has to do with some basic back-of-the-envelope math.

When the crisis began, no one knew how bad things would get, but based on the experience of China and South Korea, it seemed apparent that we’d be looking at a four-month lockdown, spanning March, April, May and June. If you assumed this lockdown meant 100% of all economic activity ceased (a ridiculous assumption, but it was the starting point at that first point of panic), a four-month lockdown would result in a total GDP decline of about a third for 2020.

Now we know more—and what we know is more promising.

According to the Commerce Department, the first quarter of 2020 saw GDP decline 4.8%. Since the lockdown really got started in the second week of March, if we extrapolate from that data what a full lockdown lasting until the end of June would look like, we can estimate the US will see its GDP fall by about 5.2% for all of 2020—if we assume zero growth post-lockdown.

This is still a pessimistic assumption, but it would indicate that stocks should be down 5.2%, not too far off their current level. And keep in mind that companies saw flat sales growth in the first quarter of 2020, which would indicate that the real hit to firms from the crisis may be better than what the entire economy suffers.

While it may sound crazy to be optimistic about anything in this environment, the numbers do indicate that investors have now discounted the lockdown’s impact on stocks, making them more fairly valued than the pundits would like you to think.

The Hedged-Income Option

Intellectually, that’s all fine and good, but how should you respond?

Obviously, the need for technology in this economy makes tech stocks a great option, but market volatility may also make you hesitate to buy stocks outright. One solution is a hedged approach, which you can get with a CEF known as the Nuveen Nasdaq 100 Dynamic Overwrite Fund (QQQX).

This fund owns the stocks that make up the NASDAQ 100 index, such as Apple (AAPL), Amazon.com (AMZN), Microsoft (MSFT) and Visa (V), but it also writes call options, a kind of insurance on its portfolio, as these options rise in value when the stocks in QQQX’s portfolio fall. This helps protect you if the market takes another dip.

The best part? QQQX’s 7% dividend has grown 11.4% in just under three years.

That high yield and payout growth make QQQX a great option if you want cash in hand today—and who doesn’t?—while putting your money to work with less worry about where the market will head next.

4 MUCH Better Buys Than QQQX (Average Yield: 8.4%!)

If you’re interested in CEFs, your timing couldn’t be better, because I’ve recently released my 4 very best buys in the space. They throw off sparkling 8.4% average payouts! PLUS they trade at huge discounts to the value of their portfolios as I write this, while QQQX trades at a slight premium.

Just how cheap are these 4 income titans?

Big enough to ignite 20%+ gains in the next 12 months, even if the market only moves slightly higher from here. And if we do get a decline, these big discounts help keep our 4 funds’ market prices stable.

And we’ll enjoy their massive 8.4% dividends the entire time!

I can’t wait to show you these 4 “crisis-proof” 8.4%-paying CEFs. Everything you need to know is waiting for you here: names, tickers, buy-under prices, complete dividend histories—the works!

One thing you can count on? If you pass up this opportunity now, you’ll surely be kicking yourself in 12 months. Don’t miss out on the dividends and upside on offer with these 4 incredible funds. Go right here to get everything you need to know.

Recent Comments