If you’re worried that you’ll struggle to profit from stocks for the next few years, you shouldn’t. There are still plenty of outsized gains waiting to be had—and today I’m going to show you exactly how to get in on the action.

First, we need to talk about what’s making stocks harder to invest in these days. It boils down to two points:

- Valuations are high.

- Interest rates are rising.

When stock valuations rise too far, they inevitably come back to earth. The S&P 500 is now trading at a price-to-earnings ratio of almost 25—the highest level in a generation except for two other times: 2000 and 2007.

That’s right—just before the last two big crashes.

This has a lot of pros worried. As my colleague Brett Owens recently pointed out, “bond god” Jeffrey Gundlach is joining several Wall Street banks in recommending investors short the market altogether!

And it’s true—a lot of Americans would probably be better off staying out of the market, because they can’t find winners as easily as they did back in 2012, when the S&P 500’s P/E ratio was a measly 14.

But that doesn’t mean you and I should give up. No way!

Because we can do far better than most folks. In fact, we can easily grab 7% dividend yields right now and 13% annual total returns for the next 5 years or more.

Here’s how.

A Clear Path to 13% Annual Returns

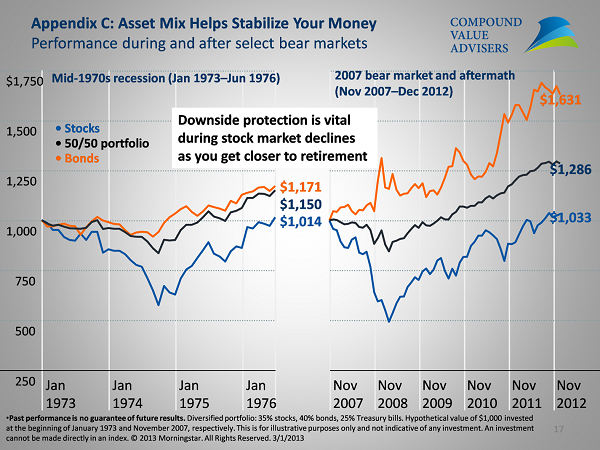

The key to getting a strong return when stocks are overvalued is simple: you need to be selective, and you need to diversify into other investments. If you choose stocks that can withstand a correction, you’re going to protect your portfolio; if you add other assets, like bonds, your portfolio is going to grow—even during a bear market.

That’s the conclusion of Compound Value Advisers, which looked at the performance of a pure stock portfolio versus a diversified stock portfolio that also includes bonds. Our stock-only investor lost out because of the downturns that hit the market every so often:

A Mix-and-Match Portfolio Wins Every Time

We can take this one step further, slashing our risk to the bone by choosing a variety of funds that go up when the stock market goes down. And we can add more insurance by investing in funds that give us a high rate of current income through dividends.

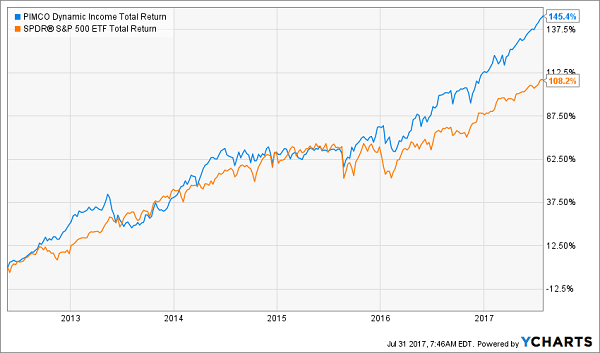

Take, for instance, the PIMCO Dynamic Income Fund (PDI), which has had a whopping 18.5% annualized return since inception. Thanks to its 8.6% dividend yield, much of that return is safe from market volatility because it comes to you in cash.

With the S&P 500’s paltry 1.9% dividend yield, much of your returns are coming as capital gains, which only exist on paper and can disappear in the blink of an eye. PDI’s “cash advantage” is why it has crushed the S&P 500 since its IPO in 2012:

Cash Is Still King

This clearly demonstrates a crucial point most folks miss: dividends aren’t just about getting cash every month; they also cut the risk in your initial investment by helping you cash out some of your returns on a regular basis.

This is why professional investors love preferred stocks, like the Goldman Sachs (GS) preferreds Warren Buffett bought during the financial crisis—and which went on to hand him a double-digit annual return over several years.

The real secret behind that return was the dividends. Goldman agreed to pay out a special 10% annual dividend payout just for Buffett’s preferred shares—which means he was getting $500 million a year on his initial investment until Goldman repurchased those shares in March 2011. Investors who tried to replicate Buffett’s investment with common shares of GS didn’t do so well:

Chasing Buffett—Without Big Dividends

Those GS shareholders weren’t getting Buffett’s 10% dividends, so of course their returns wouldn’t be as good.

Fortunately, we can easily replicate Buffett’s strategy with a closed-end fund like the John Hancock Premium Dividend Fund (PDT), which has returned 13.9% annually over the last decade while paying a 6.9% dividend:

PDT Rides Its Dividend Higher

And, as you can see from the chart above, that’s exactly how PDT has had double the total return that stocks have had over the last decade—and was even outperforming stocks during the dark days of 2009.

3 Easy Steps to 13% Returns Every Year—Forever

Preferred stocks and bonds are just the start. To really protect ourselves from stocks’ high valuations and low expected returns, we need to build a portfolio of high-dividend-paying funds that are attractively priced now and ready to hand us some of our gains in cash on a regular basis.

Fortunately there are hundreds of closed-end funds that aim to do exactly that—and many of them even pay dividends monthly! Plus, a lot of those funds have beaten the S&P 500 over the last few years, some for a decade or more!

So what do we do? It’s as easy as 1-2-3:

Step 1: You invest a set amount of cash in a group of high-yielding closed-end funds when they’re attractively priced. This immediately gives you a 7% income stream.

Step 2: Over time, your account’s cash balance will grow to the point where you can add to the portfolio by choosing funds that are attractively valued at that time.

Step 3: As you build up your portfolio by buying more funds, you’ll be more diversified and you’ll be getting a growing income stream, thanks to the power of compounding.

Invest Like a Billionaire and Grab 7.6%+ in CASH Now

By following the simple steps of buying, collecting dividends and buying again, you’ll easily set yourself up for double-digit annual returns year in and year out (including your growing cash payouts) while shielding yourself from market crashes.

You can start with the 4 funds I’m pounding the table on today. They pay SAFE 7.6% CASH dividends—the kinds of yields superstars like Buffett regularly grab with their “billionaire only” deals!

The difference? You and I can get in on the action easily, just like we’d buy any other stock!

And 7.6% CASH payouts are just the start. I’ve got all 4 of these hidden gems pegged for easy 20% price gains, too! They’re so cheap that their upside is practically locked in, no matter what happens with the market, the dysfunction in Washington or the Federal Reserve.

Recent Comments