I know that no one wants to talk about the 2020/2021 lockdowns anymore. But those dark days did do one critical thing for the high-yield corporate-bond market: made these so-called “junk bonds” too big to fail.

And investors are just starting to come around to that fact.

The takeaway is that we’ve got a nice opportunity to grab historically large, and stable, dividends from corporate-bond funds, including a closed-end fund (CEF) we’re going to focus on in this article: the PIMCO Dynamic Income Fund (PDI).

Long-time readers of my articles here on Contrarian Outlook, as well as my CEF Insider advisory, will recognize PDI. It comes up a lot, for three key reasons:

- It yields 13.8% as I write this.

- Its dividend grows.

- It kicks out some nice special dividends regularly.

What’s more, it’s run by PIMCO, one of the highest-regarded CEF managers in fixed-income.

What’s happening with PDI—and with corporate-bond funds in general—proves the old adage that one man’s junk is, indeed, another’s treasure.

Bond Buyers Take Note of “Fed-Backed” Corporate Bonds

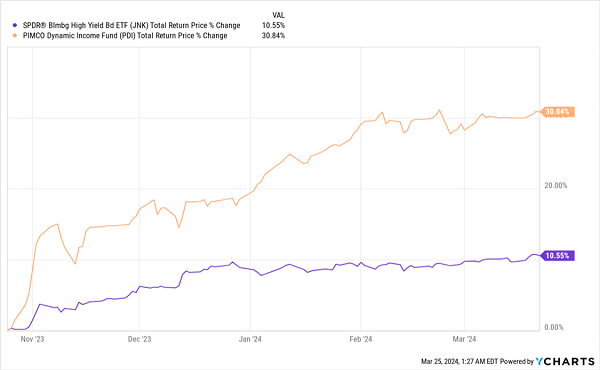

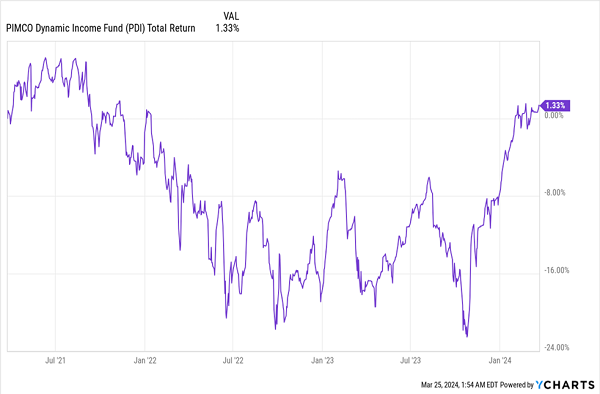

In purple above, you can see the performance of the SPDR Bloomberg High-Yield Bond ETF (JNK), the benchmark for corporate bonds, rising more than 10% in just five months. But the real story is the 30%+ gain in PDI.

About five months ago, in a November 2 article, we highlighted PDI’s value and sustainable payout, supported by its strong portfolio of high-yield bonds.

In that piece, I wrote that PDI was setting up for capital gains and that the fund was set up to give us at least $11,250 in monthly income over the long run on a million-dollar investment in what I referred to then as a “worst-case scenario.”

Well, as we can see in the above chart, those capital gains have now arrived, because the market loves these high-yielding, low-risk assets. Despite that strong performance, which is a good indicator of the kind of gains and upside you can pull from a high-yield-bond CEF these days, the “junk bond” moniker turns off a lot of investors, so let’s talk about that.

From “Junk” to Gems

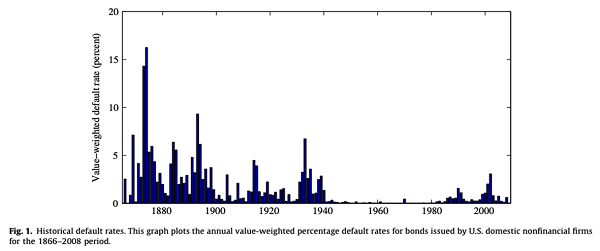

In the late 1970s, high-yield corporate bonds were virtually unknown until a Wall Street trader named Michael Milken (who is still active today) promoted them as an opportunity for struggling companies to raise cash and for investors to earn above-market returns. This worked for a while, but by the late 1980s, a combination of high inflation and big changes in the market meant a lot of these high-yield bonds performed poorly.

Source: Giesecke et al., “Corporate bond default risk: A 150-year perspective”

By the late 1980s and early 1990s, junk-bond defaults were a problem. The dot-com bubble made things worse, causing defaults to approach 5%.

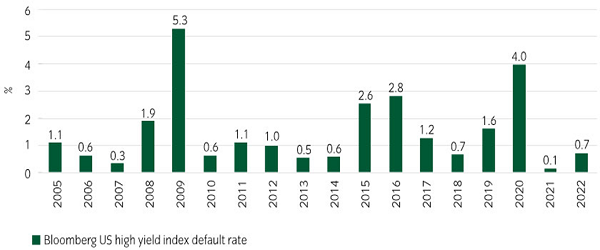

In 2009, however, the subprime-mortgage crisis prompted the Fed to buy bonds, essentially creating an implicit guarantee that junk bonds weren’t going to default at that rate again; the Fed wouldn’t allow it. And thus, default rates fell to less than 2% on average for a decade.

Junk Bonds’ Hidden Safety

Source: Insight Investment

When the shutdown of the global economy created a huge default risk in 2020, the Fed bought bonds again, bringing default rates down well below 1%. While higher interest rates in 2022 increased defaults (estimates vary, but we’re around 2.5% to 3% defaults today), the market priced this in at the same time.

Bonds Lose Their Luster

In 2022, investors sold off junk bonds for fear of a spike in defaults, but here’s the thing: They marked down a group of bonds over 12% because of a 3% default rate that, at worst, could climb to 5% in the next few months. These bonds, broadly speaking, were massively oversold.

While it’s taken a long time for the market to realize this, 2024 has been the year of realizing the benefits of junk bonds. Those include high yields, big discounts on bonds already issued into the market, a still-strong US economy and the implicit promise that the Fed will step in if things get too bad for junk bonds.

And make no mistake: the Fed will step in, because junk bonds, as I mentioned off the top, are too big to fail: At $2 trillion in market value, the junk-bond universe is now about 20% of the entire corporate-bond market.

Which brings me back to PDI. The fund goes beyond corporate junk bonds, investing in credit assets (government agency bonds, mortgage bonds and a mix of corporate debt at home and abroad) that are tightly correlated with junk bonds. It also finds a string of low-rated assets that have been oversold, buys them up, then hands the income over to investors until it eventually sells the bonds. It’s a strategy that pays serious dividends.

High, Stable Dividends—and a Raft of Special Payouts, Too

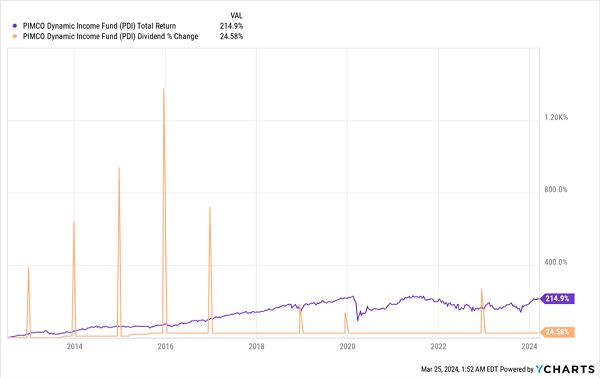

As you can see, PDI’s dividend has gone up over its history, but the real story is those orange spikes: Those are special dividends that PDI has paid out with income windfalls from its portfolio. Imagine nabbing a double-digit-yielding fund that not only doesn’t lose money or cut payouts, but actually grows them and pays special dividends along the way. That’s been PDI’s appeal for over a decade now.

To be clear, this doesn’t mean PDI is a great buy at all times. You can see that it hasn’t fully recovered from 2020, for example.

An Opportunity to Buy on the Upswing

But zooming in, we see that PDI has become particularly compelling in recent months, thanks to the market’s rediscovery of junk bonds—and the fact that they aren’t really junk at all.

Monthly Payouts and a 13.8% Dividend? That’s How Fortunes Are Built

One thing I forgot to mention about PDI is that the fund not only offers a monster yield, but it pays dividends every single month.

That’s where the magic truly happens with funds like this, because if you’re reinvesting your dividends, you can do so faster than you’d be able to with quarterly payouts. And you’re building your income stream fast, too, thanks to the monthly payouts and that huge 13.8% dividend.

This is, frankly, how fortunes are built. And PDI is far from the only CEF to offer monthly dividends—many do.

I’ve hand-picked my top 5 monthly paying CEFs and assembled them into their own “mini-portfolio.” They kick out a rich 9.2% dividend, and they’re all cheap now, so we can expect some nice capital gains upside here, too.

Recent Comments