If you hold any of these five risky REITs, you should sell them immediately. And put that money into two recession-proof bargains (paying up to 8%) that we’ll discuss shortly.

REITs aren’t always as safe as their dividends appear on paper. Consider Investors Real Estate Trust (IRET), which slashed its dividend by nearly half late last year. This wasn’t a sudden decision – it followed years of share declines as falling oil prices crushed rents across IRET’s markets.

IRET has now lost 40% in four years and seen its high-single-digit yield reduced to less than 5%. Even IRET’s brief recovery after the dividend cut has withered away, and shares are off double digits in 2017.

These five problem children all have IRET-potential.

Annaly Capital Management (NLY)

Dividend Yield: 9.9%

Annaly Capital Management (NLY) is a mortgage REIT that doesn’t actually own or operate actual real estate or properties, but instead invests primarily in agency mortgage-backed securities (the lion’s share at $88.4 billion in assets), as well as commercial mortgage loans, non-agency residential credit and a small middle market lending business.

NLY shares have rocketed 22% higher in 2017, with most of that coming in the first few weeks of the year. More important is that those gains have come on top of operational performance that I would describe as so-so at best. The company recently made a switch to focusing on “core EPS,” but that core measure isn’t saying great things about the dividend. In its most recent quarter, core EPS came to 30 cents – enough to cover the 30-cent payout with no room to spare – and in Q1, core earnings of 29 cents came up shy.

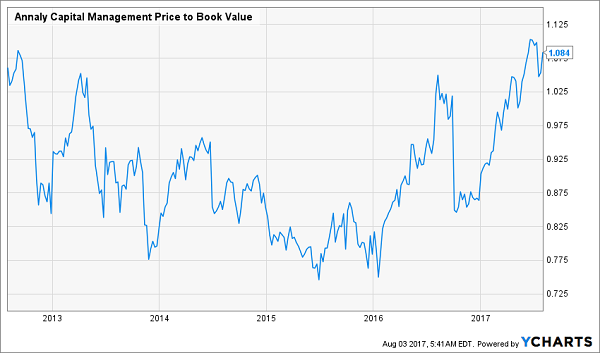

That’s troubling on its own. But combine that with a price-to-book ratio that currently sits at multiyear highs, and it’s clear that if you buy NLY right now, you do so at your own (high) risk.

Don’t Pay a Premium for Annaly’s (NLY) Barely Covered Dividend

Global Net Lease (GNL)

Dividend Yield: 9.7%

Global Net Lease (GNL) is yet another dividend coverage concern.

GNL is one of several “triple-net lease,” or NNN, REITs, are revered in the real estate world because of the structure of their agreements. Specifically, tenants are on the hook for taxes, insurance and maintenance, so they typically don’t charge tenants as much, but what they net out is expected to be much more predictable.

In GNL’s case, the company makes triple-net lease agreements on single-tenant commercial properties in the U.S., as well as European countries including the U.K., Germany, France and the Netherlands. Because Global Net Lease is an externally managed company, GNL must pay a number of fees for property management and other third-party service providers.

Hence, while the company is actually growing, it’s doing so with quite a bit of leverage, and that fee drag really does hamper funds from operations. Specifically, GNL paid out $2.13 per share in dividends last year – 97% of the company’s adjusted FFO of $2.19. And in Q1, it actually paid out 53.25 cents across three monthly payments, versus 52 cents in AFFO.

GNL’s High Dividends Can’t Even Match the Bleeding

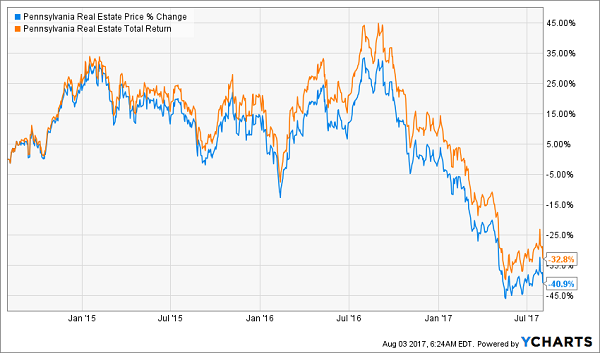

Pennsylvania R.E.I.T (PEI)

Dividend Yield: 7.4%

While I believe some retail REITs will be immune to the damage Amazon.com (AMZN) is doling out to brick-and-mortar businesses, it’s time to cut bait with those that clearly are right in the crosshairs.

Take Pennsylvania R.E.I.T. (PEI), which despite the name has malls not just in Pennsylvania, but also in the D.C. metro area, Northeast, Southeast and other geographical areas. The company’s portfolio of traditional malls is taking a beating, and the company is swerving hard toward “experiential” tenants like Dave & Buster’s (PLAY) to reflect a consumer shift away from traditional brick-and-mortar retailers, and toward experiences-based spending.

Dividend coverage isn’t yet an issue, but it’s clear to see what an uphill battle PEI faces. AFFO plunged from 43 cents per share to 35 cents in Q1 of this year. Meanwhile, the payout has been locked in place for more than two years now – a worrisome sign for investors in most traditional REITs.

PEI’s High Yield Is Due to Hemorrhaging, Not Hikes

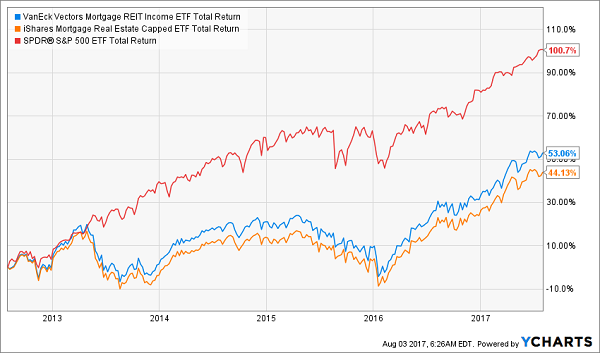

VanEck Vectors Mortgage REIT Income ETF (MORT)

Dividend Yield: 9.3%

The VanEck Vectors Mortgage REIT Income ETF (MORT) is an example of how even diverse ETFs can’t necessarily deliver the goods.

The mortgage REIT industry does in fact contain a few winners; Apollo Commercial Real Estate Finance (ARI) comes to mind. But if you think investing in an ETF to capture the return potential of those winners is the way to go, think again.

That’s because MORT and rival iShares Mortgage Real Estate Capped ETF (REM) are heavily weighted toward the larger but shakier mREITs in the space, such as Annaly and AGNC Investment Corp. (AGNC). In fact, both ETFs have nearly a quarter of their assets invested in just those two mREITs alone.

MORT and REM: High Income … But Low Returns

With MORT and REM, the losers overwhelm the contributions of the winners, leading to lackluster performance that can’t even keep up with the S&P 500 despite yields typically between 9% to 10%!

2 Dividend Growth REITs: Up to 8.2% Yields and 25%+ Upside

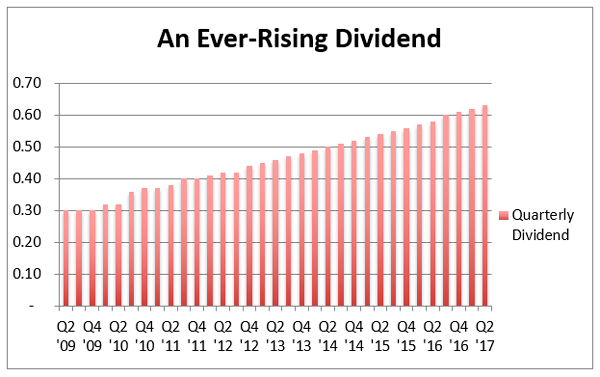

My favorite REIT today recently raised its dividend again by 4% over last quarter’s payout. This marks the 20th consecutive quarterly dividend hike for the firm:

It pays an 8.2% yield today – but that’s actually an 8.6% forward yield when you consider we’re going to see four more dividend increases over the next year. And the stock is trading for less than 10-times funds from operations (FFO). Pretty cheap.

However I expect its valuation and stock price will rise by 20% over the next 12 months as more money comes stampeding into its REIT sector – which makes right now the best time to buy and secure an 8.5% forward yield.

Same for another REIT favorite of mine, a 7.4% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years.

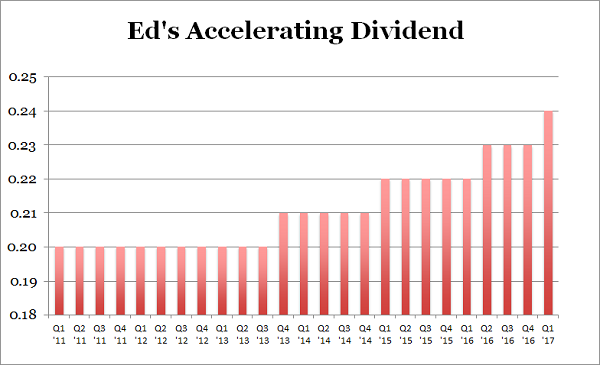

The firm’s investors have enjoyed 86% total returns over the last five years (with much of that coming back as cash dividends.) And right now is actually a better time than ever to buy because its growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

An Accelerating Dividend

This stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof,

- It yields a fat (and secure) 7.4%, and

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. And they can even enjoy price upside to boot, thanks to the bargain prices they’re buying at.

Remember, there’s never been a better time to buy REITs and live off their dividends. But it’s important to choose wisely. Retail REITs are dangerous, while other recession-proof issues are bargains. I’d love to share the latter with you – including specific stock names, tickers and buy prices. Click here and I’ll send my full 8% No Withdrawal Portfolio research you to right now.

Recent Comments