Preferred stocks often pay high-single-digit yields, with far less risk than their similar-yielding “common” stock cousins. While many 5% and 6% common payers are yield traps with broken business models, it is possible to find preferred payouts at these levels that are perfectly secure.

Not yet familiar with preferred stocks? With “common” shares paying so little, it’s time to get acquainted.

Most dividend darlings don’t pay much on their own common shares today. You’ll be hard-pressed to find a dividend aristocrat with a yield above 3% or a P/E ratio below 20.

On the other hand, a company will issue preferred shares to raise capital. In return, it will pay regular dividends on these shares – and as their name suggests, preferreds do receive their payouts before common shares. They typically get paid more, and even have a priority claim on the company’s earnings and assets in case something bad happens, like bankruptcy.

Preferred prices tend to be steadier than regular stocks, thanks to their big dividends. They’re also inconvenient to buy individually, so investors often turn to funds like ETFs and CEFs (closed-end funds) as ways to buy 5%+ paying baskets of preferred shares.

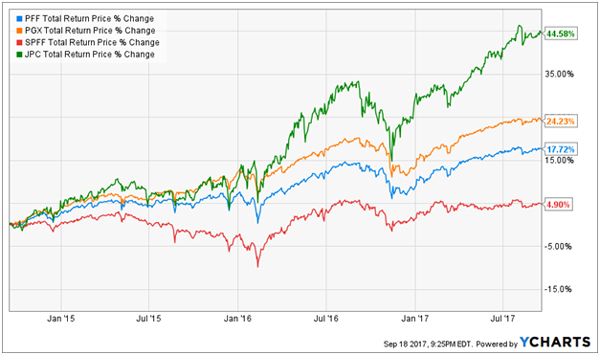

But not all funds are created equal. Let’s look at four of the most popular issues. The worst fund returned just 4.9% over the past three years – in other words, it lost more in price than it paid in dividends.

The best fund, on the other hand, delivered steady total returns (including dividends) of 44.6%. The difference? Better management, and better preferred stock picking:

4 Preferred Funds: From Dogs to Winners

Let’s break down these four popular preferred funds.

iShares U.S. Preferred Stock ETF (PFF)

Yield: 5.3%

Expenses: 0.47%

The iShares U.S. Preferred Stock ETF (PFF) is the most popular preferred-stock ETF on the market by a mile, with its $18.5 billion in assets coming in about $13 billion more than the next closest ETF, the PowerShares Preferred Portfolio (PGX).

It does its job, providing investors with access to more than 280 preferred shares from the likes of Wells Fargo (WFC), HSBC (HSBC) and Allergan (AGN). It’s built like a typical preferred fund, too, with the majority of its holdings in financials – specifically, 70% split among banks, diversified financials and insurance – about 10% in real estate and the rest split in trace amounts among a few other sectors.

However, PFF’s holdings are actually of extremely high credit quality, and that works against it, as its yield sits below many of its close competitors, hampering performance. Thus, this ETF might be a popular name, but it’s a middling preferred holding.

PowerShares Preferred Portfolio (PGX)

Yield: 5.5%

Expenses: 0.5%

PGX looks pretty similar to PFF, with nearly three-quarters of the fund dedicated to financials, and another 9% in real estate investment trusts (REITs).

However, while the PGX might be No. 2 in assets and even charges a couple more basis points in annual fees than PFF, it certainly has a couple edges over its larger competitor.

The most significant is yield. PGX typically offers a higher payout than PFF, and that’s currently the case by about 20 bps at present. That’s because PGX’s portfolio, while not dangerous, takes a bit more credit risk. The lion’s share of PGX’s 260 holdings (58%) have a BBB rating, while another 30% are rated BB. By comparison, just 30% of PFF’s holdings are in BBB and BB combined, with the biggest single credit allocation going to AAA-rated preferred stocks (34%).

That has helped provide PGX with a decent performance advantage over time. As far as straight-laced preferred-stock fund goes, PGX is simply a better play than PFF.

Global X SuperIncome Preferred ETF (SPFF)

Yield: 6.8%

Expenses: 0.58%

Of course, it is possible to stretch too far for yield.

The Global X SuperIncome Preferred ETF (SPFF) certainly lives up to its moniker, doling out nearly 7% in dividend yield that puts its ETF competitors to shame. And it does so with a fairly typical sector makeup that includes a 66% weight in financials such as Wells and Barclays (BCS) and 9% in REITs such as Vereit (VER).

Credit quality isn’t bad, per se – 35% of SPFF’s holdings fall in the BBB range, with another 30% in A and 15% in BB. However, nearly 20% of the fund falls into either B or “not rated,” and that risk is exacerbated given that SPFF holds just 50 preferred issues.

As a result, SPFF has been a total return laggard since inception. Avoid the siren song of its superior headline yield.

Nuveen Preferred Income Opportunities Fund (JPC)

Yield: 6.7%

Expenses: 1.33%

If you’re going to chase high yield in preferred stocks, you’re better off with a closed-end fund like the Nuveen Preferred Income Opportunities Fund (JPC). Yes, this is the priciest fund by far … but you can see in the chart below, unveiling our four mystery funds, that you’re paying for quality.

Closed-end funds operate somewhat like ETFs in that they trade on an exchange, but rather than create and redeem shares, CEFs start with a set number of shares for the life of the fund, and based on market demand, they can trade well above (premium) or well below (discount) net asset value.

JPC boasts nearly 220 holdings – mostly preferred stocks, though about 10% of the portfolio is invested in corporate bonds. There’s also international diversification, with about 25% allocated to foreign holdings, though top issuers are American financial giants Citigroup (C), JPMorgan Chase (JPM), Bank of America (BAC) and Wells.

Active management pays its way here, with efficient use of leverage resulting not just in a high yield compared to most preferred ETFs along with superior performance.

And My Favorite Preferred Share Fund Pays 7.3% Today

ETFs like PGX, PFF and SPFF often disappoint because their diversification actually expose you to unnecessary credit risk. The only way you lose with this vehicle is by giving your money to a driver who crashes your car. But the S&P 500 and NASDAQ are large enough that there’s usually a company financially crashing into a brick wall at any moment in time.

And if we include the brick wall the financial world ran into ten years ago, these funds haven’t even performed to their current yields.

I suspect PGX, PFF and SPFF probably won’t actually return 5% or 6% annually over the next decade, either. Which why I recommend moving past a broad-based ETF in favor of a fund with an active manager working for you. There’s extra yield to be had in preferred shares – but you should make sure you have an expert buying your stock to keep you safe and on the road.

My favorite preferred fund today – which I like even more than JPC – pays 7.3% today. It’s an excellent deal because it’s selling at a discount to net asset values (NAVs).

Why the buying opportunity? Recently, investors irrationally sold any and all closed-ends down to silly bargain prices. Some deservedly so, but this high quality preferred funds – with an excellent management team and track record – was swept away by the hysteria.

That’s great for us. Low prices mean higher yields plus some upside as these funds gradually close their discount windows. And this 7.3% yield nets us 20%+ more income, more securely, than its ETF counterpart. Plus, the fund has a history of actually delivering these types of returns over the long haul (unlike the more popular ETFs).

Lesser-known high income plays like these are the cornerstones of my “no withdrawal” retirement portfolio strategy. Why rely on stock price appreciation in an inflated market when there are secure, high paying dividends you can simply live off of and keep your capital intact?

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 7% and 8% yields to fund their lives.

That’s why I specialize in finding safe, under-the-radar high income options. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my favorite preferred fund for 7.3% dividends.

Recent Comments