This onshoring trend is roaring—but we contrarian dividend investors still have time to cash in. I’ve got a “3-pack” of cheap stocks that lets us do that, with dividends that are surging (or are about to!) below.

The two latest signs we’re in the midst of “Industrial Revolution II” here in the US? According to new Census Department figures, Detroit, the HQ of industrial America, is seeing its population grow again for the first time since 1957!

The “OG” Industrial Boom

And the latest round in the tariff wars? They’ll almost certainly send more companies scurrying to America.

Think “Picks and Shovels” for the Best Plays on Industrial Revolution II

If you’ve been reading my articles for a while, you know I love “pick-and-shovel” stocks. This refers to the California Gold Rush, in which the businesses that sold miners supplies made the real money, not the gold-panners themselves.

So who are the pick-and-shovel peddlers of Industrial Revolution II? The owners of the warehouses, factories and shipping services manufacturers rely on. Many are cheap now because folks have overreacted to some temporary headwinds. Let’s get into them.

Industrial REITs—the Onshoring Plays Mainstream Investors Forgot

The biggest warehouse owner of them all, Prologis (PLD), may seem pricey by the measures most folks use. The real estate investment trust (REIT) does, after all, trade at 21-times the midpoint of its forecast 2024 core funds-from-operations (FFO). (FFO is the go-to metric for REIT profitability.)

But there are two other, far lesser-known factors pointing to a sweet deal here.

First, PLD ended its latest quarter with a strong 97.8% occupancy rate. Now granted, if you look the stock up online, you’ll see that management has revised its guidance lower for the full year, as higher rates (and their hit on goods spending) prompt some tenants, and potential tenants, to rethink their space needs.

But the midpoint of its new core-FFO forecast is still up a healthy 6% from 2023. And none of this comes close to justifying the stock’s 36% (!) drop from its all-time high in April 2022.

This is the first sign PLD is oversold. When rates move lower, more existing tenants will re-up and expand, and more new ones will sign on. Onshoring is an added upside kicker here.

And even if that bounce takes a while to arrive, the dividend only occupies 71% of management’s new core FFO forecast—very manageable for a REIT. That’s likely to keep the payout popping higher, too.

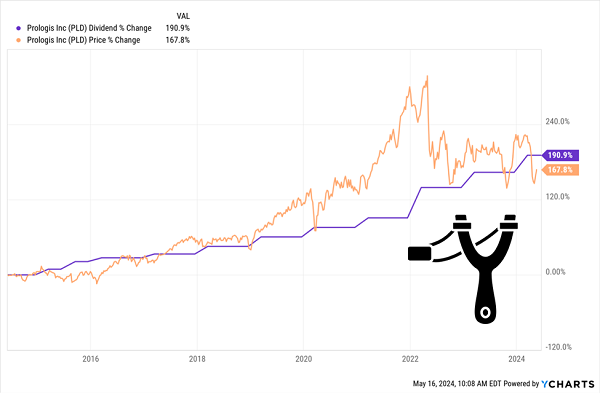

Here’s the second sign PLD is cheap: The stock yields 3.5%, nearly triple the S&P 500 average. As a result, investors mainly look to it as an income play—and bid the stock up every time management hikes the payout:

PLD’s Share Price Is Set to “Snap Back” Above Its Dividend

This effect is clear in PLD’s history, and the shares are primed to bounce back above the payout, as they’ve done every time they’ve fallen behind. That leaves a nice window to get in before they do.

Railways: The “Arteries” of the Onshoring Trend

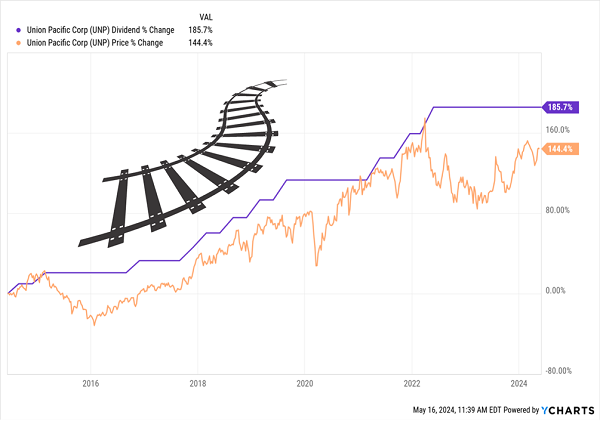

Railways are another onshoring beneficiary, and we’re looking at a “twofer” today: Union Pacific (UNP) and CSX Corp. (CSX). Between them, they span the country, with CSX’s network covering the east and UNP dominating West Coast ports.

UNP is off about 11% from its 2022 highs due to lower shipping activity spurred by, you guessed it, high rates. But as with PLD, that weight should lighten as rates decline.

That, in turn, would restart UNP’s dividend growth, which has been blowing off steam on a siding for nearly two years now. But as we see below, the stock is still well behind the payout’s rise, suggesting more upside, even if the dividend holds steady for a while yet:

UNP’s Dividend Lays the Track, Price Follows

Finally, UNP’s efficiency continues to improve, with an operating ratio (or operating costs as a percentage of revenue—the lower the better) of 60.7 in the latest quarter, down 10 basis points from a year earlier. That’s ahead of CSX, at 63.2, and Canadian Pacific Kansas City Southern (CP) at 63.4.

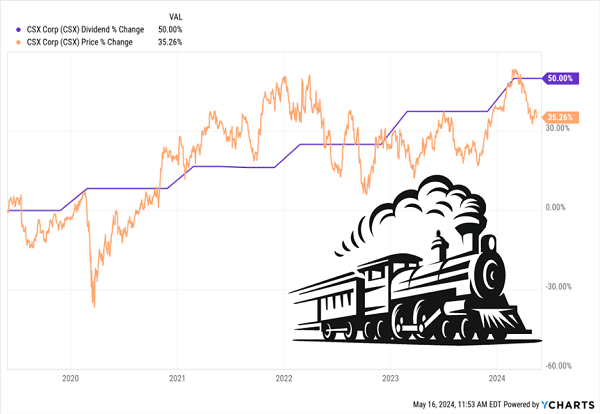

This is a good segue to CSX, which trails UNP on the current-yield front (2.1% to 1.4%) and, as discussed, in operating efficiency. But that just leaves management more room to goose profits as it catches up!

Moreover, CSX’s payout has grown like a weed: up 50% in five years, with a price gain that’s (almost) matched that rise. Here again, our “dividend gap” points to more upside:

CSX’s Dividend “Engine” Pulls Share-Price “Caboose”

CSX’s revenue declined 1% in Q1, but that was due to lower fuel surcharges, trucking revenue and export coal prices. Volumes actually gained 3%. And the coming decline in rates should push revenue, and volumes, higher from here.

That’s a nice opportunity for us, with the stock down 12% since March—especially when CSX is paying out just 30% of its free cash flow as dividends, leaving it plenty of room to keep the payout party rolling in the bar car!

5 More Surging Dividends to Buy Now (Before They Race Away From Us)

This “dividend-up, share-price-up” setup is the most powerful pattern I’ve seen in investing. It’s worked for my readers over and over again … so many times that I’ve come to one inescapable conclusion:

Dividend growth is the No. 1 driver of share price growth. Hands down.

I’ve got 5 more stocks to help you take full advantage of this proven pattern. They have the surging earnings and strong balance sheets they need to keep their payouts—and share prices—popping higher for decades.

I call these 5 names “Dividend Magnet” stocks, and the time to buy them is now. The longer we wait, the more dividends (and gains) we leave on the table!

Recent Comments