I know it’s hard not to worry about your portfolio, and income stream, these days, but we will make our way through this crisis. When we do, your holdings will bounce back—and likely faster than the market if you hold strong dividend stocks.

And, when the time is right, I expect we’ll get a chance to snap up some huge dividends for dimes on the dollar. I’ll keep you posted on when we’ll move—and what to buy—in my Contrarian Income Report service.

(These are the types of dividend bargains that are only available once a decade. I’m talking about the post-crash worlds of 1987, 2002, 2009 and, coming soon, late 2020.)

But if you insist on deploying some cash now, I’ve got you covered there, too. In a second, I’ll give you two strengths you must demand in anything you buy in the coming weeks, along with three stocks with recession resilience in spades.

But before we get to that, let’s talk about when we can expect this market to finally bottom out.

When Will Stocks Bottom? Here’s What History Says

As I wrote on April 1, it’s possible the S&P 500 already bottomed on March 23, when we hit the low of this crisis. But that’s unlikely, because forming a bottom takes time, with stocks first setting a new low, then testing (and retesting) it—and sometimes breaking through that low to set an even lower one.

You can see that in the 2008 crash, with its W-shaped bottom and recovery:

2008/09’s Rocky Bottom

I sometimes hear from folks kicking themselves for not buying in October 2008, but let’s not forget that the drop from the October 1, 2008, low to the ultimate bottom on March 9, 2009, was a grinding 41%. Many folks threw in the towel on that last leg down.

Of course, no one knows if that will happen this time, but I am anticipating at least a retest of our March lows. So if you’re intent on buying now, be careful. Let’s cover the two things a stock needs to hold its own if we do take out the March low.

April Buy “Must-Have” No. 1: A Low Beta

A stock’s beta is a handy volatility indicator. You can find it on any screener, including Yahoo Finance and Google Finance.

Here’s how it works: the “beta” of the S&P 500 is always 1. So a stock with a beta below 1 is less volatile than the market. Betas above 1 are more volatile. (Since different screeners measure beta over different timeframes, you might see varying numbers from one to another.)

Consider the first stock I want to talk to you about today: Crown Castle International (CCI), a cell-tower owner I cited as one of three “recession-fighter” tech dividends in my March 31 article. As I write this, CCI’s beta, measured over the past five years, is 0.28, meaning CCI has been 72% less volatile than the S&P 500.

You can see its steadiness in this pullback: year to date, CCI’s stock price has slipped only about 2.9%, compared to a 22% plunge for the S&P 500:

CCI’s Low Beta Shines Through

Crown Castle’s low volatility makes sense: the real estate investment trust (REIT) forms a big part of America’s communication backbone, with its 40,000 cell towers and 80,000 route miles of fiber-optic cable.

REITs have been hammered in this downturn, and the pain got worse on April 1, when millions of people told their landlords they can’t pay the rent. CCI doesn’t have that problem, with cell service critical in this period of isolation, and among the last things cash-strapped consumers will cut.

That means the company’s clients, including Big 4 US telcos Verizon (VZ), AT&T (T), Sprint (S) and T-Mobile US (TMUS), are unlikely to leave CCI holding the bag. Combined, these four supply 74% of CCI’s site-rental revenue, a high concentration that actually provides a measure of safety these days. The company also gets revenue certainty from its long-term leases: as of November 2019 CCI had a weighted average remaining lease term of five years.

But we’re getting off track—let’s move on to my second “must have” that any stock on your shopping list needs to have today.

April Buy “Must Have” No. 2: A Safe—and Growing—Dividend

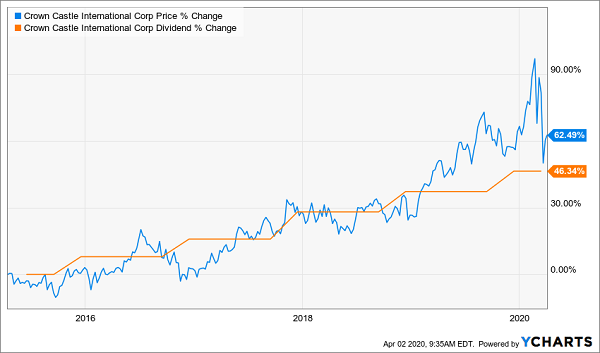

I’ve written before about how a rising dividend can pace a company’s share price higher. This crisis has “broken” many of these charts (for now!). But that’s not the case with Crown Castle—it’s a great example of how a company’s “dividend magnet” can pull its share price higher.

You can clearly see the stock price increase with each payout hike:

CCI’s Dividend Powers Its Stock Through the Crash

Of course, a history of dividend growth isn’t enough, because as we’ve seen recently, several companies that have made steady payouts for years have hit the brakes on them, and there are more to come, with Goldman Sachs (GS) recently saying it expects dividend payouts to fall 25% this year.

For extra insurance, then, we need to look at other factors, including a stock’s payout ratio. For a REIT, that means dividing the annualized dividend into the last 12 months of adjusted funds from operations (FFO)—a better measure of REIT performance than earnings per share. In the case of CCI, we get a payout ratio of 84%, which is plenty safe for a REIT with long-term, predictable revenue streams.

2 More Steady Dividend Growers for Volatile Times

Have you noticed that spices are in short supply at your local grocery store? With restaurants out of the picture, everyone is cooking at home—and flavorings and condiments are in high demand.

That’s great news for McCormick & Co. (MKC), which cranks out spices under the Club House brands, as well as honey (Billy Bee), mustard (French’s), hot sauce (Frank’s) and plenty of other names you’ll find in any kitchen cupboard in America.

McCormick boasts an ultra-low five-year beta of 0.25, and has outperformed the S&P 500 in the crash, falling less then half of the market, showing its stability and setting up a nice potential entry point to buy shares.

McCormick’s Hearty Stock Performance

As with CCI, McCormick’s rising dividend has also supported its stock price, and we can expect that to continue, thanks to its ultra-low payout ratio, with 44% of earnings and a similar amount of free cash flow going out the door as dividends.

A Pinch of Dividend Growth Spices Up MKC

The extra kick? (Sorry, I couldn’t resist.) McCormick boasts a strong balance sheet, with $4.4 billion of long-term debt, a very reasonable portion of its $19-billion market cap.

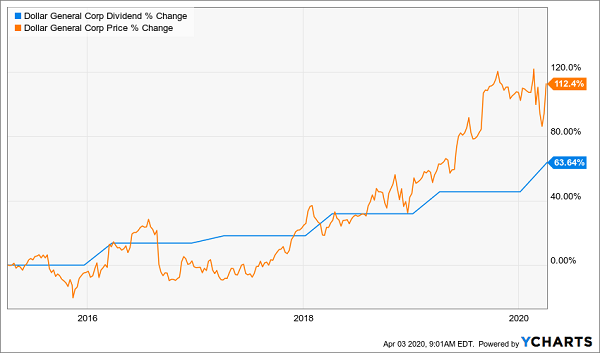

Finally, Dollar General (DG) isn’t the place to go shopping for yield—the stock pays just 0.9% today. But the dollar-store chain, with more than 16,000 locations in 45 states, peddles big dividend growth, having hiked its payout 63% since starting its five years ago; the yield on a buy back then would have more than doubled, to around 1.9% today.

The correlation between dividend growth and share-price growth is evident here, too.

Another Payout-Powered Stock

Dollar stores are the classic recession play, so you’re not going to get a screaming deal here—DG is only off about 2.9% from the February 19 peak. But you will get a steady share price, with extremely low volatility: the stock’s beta is a lowly 0.25.

The dividend is also backstopped by one of the lowest payout ratios I’ve seen—just 22.5% of free cash flow. In other words, DG could double its dividend tomorrow and still be well below my 50% dividend-safety line.

Two other bullish signals: DG already declared a big dividend increase (a 12.5% hike, to be exact) on March 12, even as the coronavirus emerged as a legitimate threat. And the company is one of the few on a hiring spree; it’s looking to add up to 50,000 workers to meet an expected surge in demand for the basics as people hunker down. That makes it a timely stock to consider now.

Your Crisis Survival Plan: 10% Dividends Paid Monthly

In a market like today’s, you need dividend income more than ever, not only for the valuable cash stream it provides, but to naturally hedge your portfolio, too.

Because when you get more of your return in safe cash dividends, you can worry less about the daily gyrations of the stock market. And if you hit the “income holy grail” of being able to live on dividends alone, you can tune out the market altogether. (As long as your dividends are safe, of course.)

This is exactly what I designed my “10% Monthly Dividend Portfolio” to give you. First up, as the name suggests, it hands you outsized dividend checks every month, not every quarter—perfect for paying your bills.

Or, if you just want to give your portfolio extra ballast (and don’t need to rely on it for income), you can simply hang on to the cash. That will naturally reduce your equity exposure—and your volatility—while building your cash balance. Fast-forward 10 years, and you’ll have recovered your entire upfront investment in cash dividends!

This is the way everyone should invest, but far too many people dismiss dividends, even though they’ve provided a large slice of the market’s long-term total return.

Don’t make that mistake! Instead, free yourself from financial worry with my 10% Monthly Payer Portfolio. I’ll share everything I have on this unique collection of income stocks—names, tickers, buy-under prices and my complete analysis of their sturdy payouts—with you right here.

Recent Comments