The stock market is probably going to be a mess this year. With the Federal Reserve taking away the punch bowl it’s been providing since March 2020, investors are likely to start selling once they begin sobering up.

This will likely be bad for speculations, such as profitless tech stocks and crypto coins featuring dog breeds. But it could be great for the dividend stocks we love, as “flights to safety” will naturally find refuge in our reliable payers.

We’ve already enjoyed some great dividend-powered profits from 2020 and 2021. And there’s no reason for us to cash in these profits just yet. It’s important for us to let our winners run and not sell until my preferred “traffic light” setup flips all the way to red.

Of course these “dividend doubles” begin with a flashing green light, our bat signal to buy a bargain.

Green: When the Dividend Outruns the Share Price, We Buy

My first tip will probably surprise you (unless you’re a regular reader of my articles, that is!): no matter what kind of market you’re buying in, be sure to always look closely at the dividend-growth rate of the stock you’re considering.

Because here’s something few folks realize: dividend growth is the No. 1 driver of share prices. So if you buy a stock with a payout that’s not only growing but accelerating, you can give yourself a nice upside pop.

And in a falling market, a rising dividend can help stabilize your stock’s price as more investors spot the growing payout and buy in.

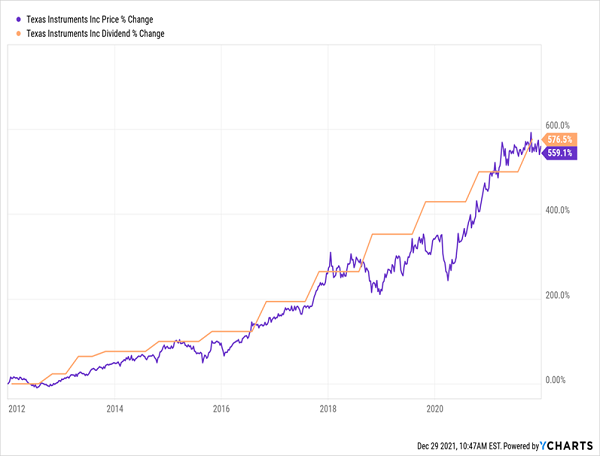

I’ve seen this pattern play out so many times it’s almost laughable. Just look at this chart of Texas Instruments (TXN), which has hiked its payout 577% in the last decade. It’s hard to argue that the company’s explosive payout growth hasn’t affected its share price: the stock is up almost the same amount—and the dividend-up, share-price-up pattern is clear.

TXN’s Dividend Boots Up Its Stock

As you can see above, every time TXN dips, it inevitably bounces back to “catch” its dividend.

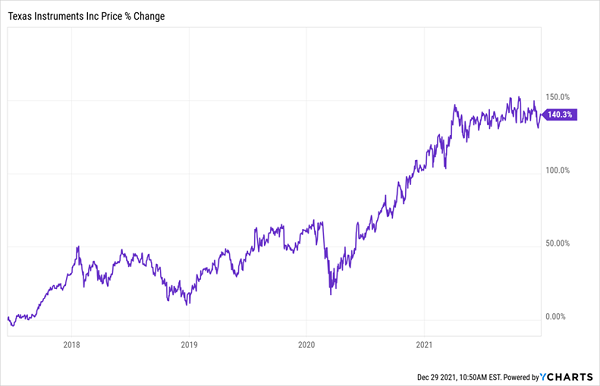

This is the dynamic I saw setting up with the stock in June 2017, and it prompted me to issue a buy call on the stock in the September 2020 issue of Hidden Yields. TXN has rewarded us handsomely, riding its rising dividend to a 140% price gain (or a 170% total return) since!

… And Then Bounce Back

Now that we’ve covered our dividend-driven buy indicator, let’s turn this strategy on its head and use it to tell us when it’s time to sell and take profits.

Yellow: When the Dividend Falls Behind the Share Price, We Stay Alert

For this step, let’s look at insurer Assurant (AIZ), which we sold in Hidden Yields in December 2019, for a 90% total return in just over four years.

During our holding period, Assurant shares continued to mostly track the company’s dividend, while jumping ahead from time to time. We were happy with this trajectory—though I did keep a close eye on it—so we let the stock run.

But the share price really took off in the last six months of 2019, as you can see below—and it quickly became clear that Assurant didn’t have the payout growth to support that leap:

AIZ Buries Its Dividend … and We Check Out

This is NOT the kind of setup you want to be caught holding when the market turns, so we took our 90% total return off the table. And as expected, Assurant has only posted a modest 18% price gain since, while the market bounced 49%:

Our “Dividend Indicator” Proves Its Value

Now let’s move on to our final sell indicator.

Red: When Momentum Stalls, and Yields Shrink, We Sell

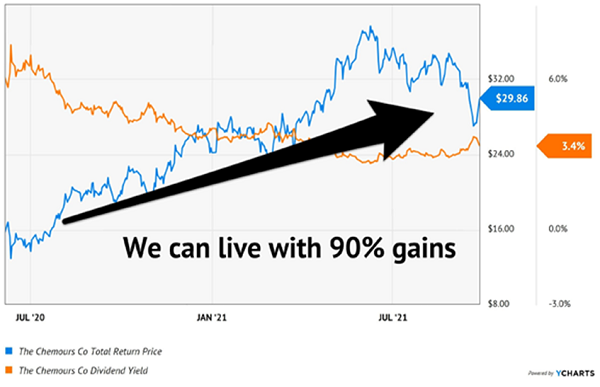

When we bought chemical maker Chemours (CC) in my Contrarian Income Report high-yield investing service in June 2020, it had a lot of appeal, including its 7.4% dividend and a 10% short squeeze “overhang.” In other words, 10% of its outstanding shares were being sold short, and these early sellers had to pay this fat dividend out of their own pockets.

The short sellers were wagering on an overhang of potential litigation against CC. But we recognized these fears as overblown when company Chief Operating Officer Mark Newman bought another 2,500 shares in May of 2020, just before we made our buy.

As it became clear that the CC shorts were wrong, they began to lose their shorts. Each share they “bought back” (short sellers have to “buy back” the shares they borrowed and deliver them to the lender) helped nudge CC higher. Plus, we collected the fat quarterly dividend alongside Mark as we enjoyed 90% total returns since June 2020.

Price Pop Lowers CC’s Yield

But by October 2021 we were at a crossroads, with momentum stalled for about four months and the yield for buyers cut to around 3.4%, due to the stock’s fast gains. That’s much less of an attractive lure to new buyers than the original 7.4%, which drove a lot of the stock’s momentum when we first bought.

Add in the Fed’s pullback on stimulus (and move toward higher rates), which could weaken demand for Chemours’ industrial chemicals, and it made sense to take our 90% gain off the table in October 2021.

Revealed: My Top 7 Dividend Growers to Buy in 2022 (and Hold Forever)

Even though I expect 2022 to be a stock-picker’s year, where timely moves into, and out of, specific stocks will be absolutely critical, there are still plenty of stocks out there that are ripe for buying now—and holding essentially forever.

I’m talking about companies whose businesses are so sturdy that they tick along, generating steady profits and high—and growing!—dividends in bull markets, bear markets, inflation, deflation … you name it.

My research team and I have combed the markets for these hidden gems and we’ve compiled our top 7 picks in a new special report I’ll give you when you click right here. These stout dividend growers are pegged for 15%+ returns year in and year out—forever.

That’s enough to double your nest egg every five years, AND these companies’ strong payouts will triple what you’d get from the typical S&P 500 stock.

Now is the time to buy these 7 cash machines, before they start on their next double-digit run. Go here and I’ll give you everything I have on them—names, tickers, dividend-growth histories, my complete analysis of their operations and more.

Recent Comments