Imagine what you could do with a 19% dividend.

To be clear, any dividend that high simply isn’t sustainable. So if you do see one, I don’t recommend buying.

Still, the thought’s nice. With a 19% yield, financial independence becomes easy. Want to live on $60,000 per year? Well, conventional wisdom says you’ll need at least $1.5 million to generate that kind of income, and some advisors will tell you to save $2 million, just to be safe.

But a 19% dividend? Suddenly it only takes $316,000 in savings to secure $60,000 in yearly income. That cuts down how long one needs to work and save by decades. Who wouldn’t want such a thing?

And while a 19% yield may be off the table (for reasons I’ll get into in a moment), all is not lost here: thanks to the 2022 pullback, there are plenty of safe dividends in closed-end funds (CEFs) in the 10% to 12% range, which is still plenty high to build a livable income stream on a reasonable nest egg. I have plenty of buys in that neighborhood that I’ve personally safety checked in the portfolio of my CEF Insider service.

But just for interest’s sake, let’s look at one 19% dividend (18.6%, to be precise) out there—the payout on a CEF called the Cornerstone Total Return Fund (CRF)—to illustrate why a payout that high is one to avoid.

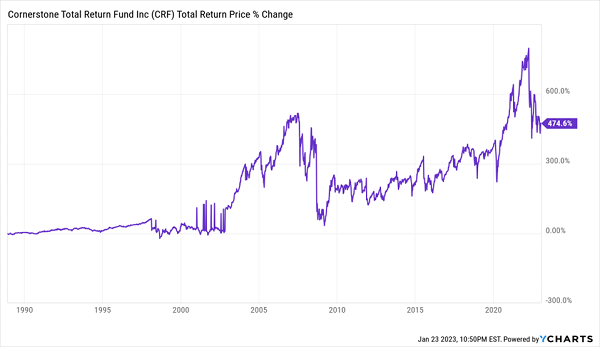

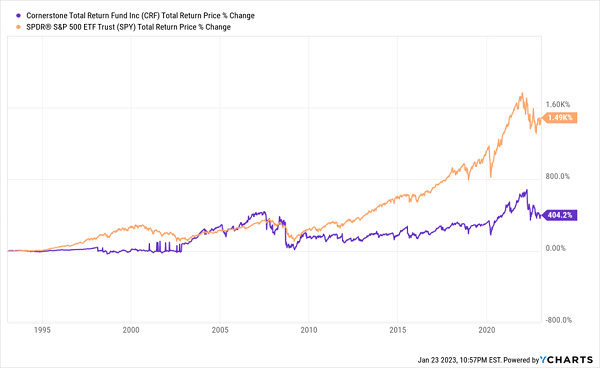

First off, it’s easy to understand why you might be tempted by CRF’s 18.6% yield, given its long history: the fund has been around since 1986.

CRF Boasts a Long History

What’s more, as you can see above, CRF has indeed earned investors a profit over the long term, and it’s hard to tell people they’ve made a bad investment when they’ve made money at it!

But we still shouldn’t bite on CRF, despite its history and the fact that it has a portfolio made up of household-name American companies: Apple (AAPL), Microsoft (MSFT), UnitedHealth Group (UNH) and Amazon.com (AMZN) are all top holdings. Here are three reasons why I feel this way:

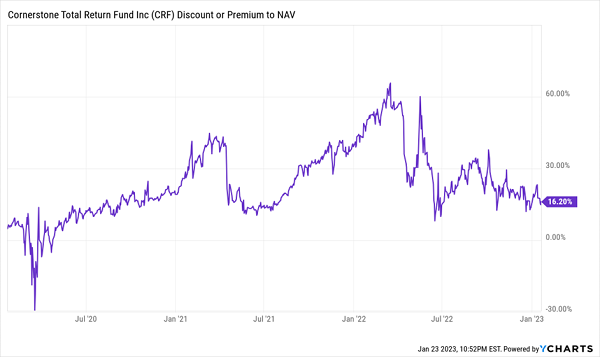

Reason #1: CRF Is Overpriced

The most obvious reason not to buy CRF now is that it trades for more than it’s worth.

CRF Investors Pay $1.16 for Every Dollar of CRF’s Assets

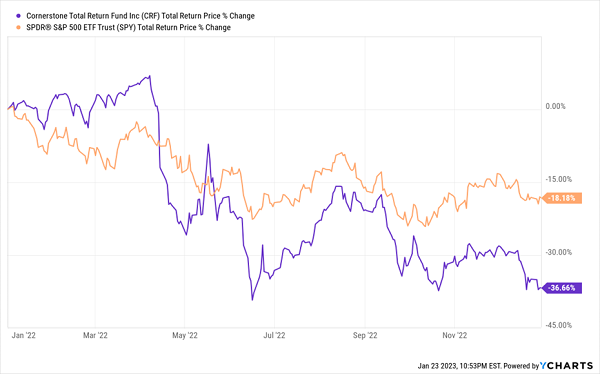

CRF traded at a market price above its net asset value (NAV, or the value of the assets it holds) throughout 2022, despite the selloff in the market, the fund’s portfolio and the fund’s market price. In fact, CRF’s losses were nearly double those of the broader stock market in 2022.

CRF Outperformed the S&P 500 (in a Bad Way) in 2022

Why would you pay a premium for a fund that underperforms? The only reason why most folks do is that they’re lured by that high yield. But the fund’s loss last year included its dividend, so there was no safety in that payout. The fact that CRF continues to trade at a premium only amplifies its risk.

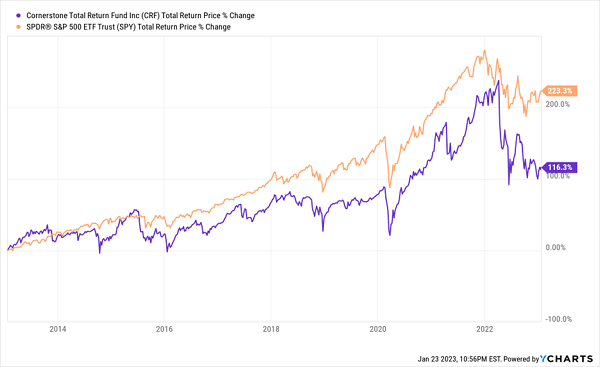

Reason #2: CRF Underperforms

As I alluded to above, CRF tends to do worse than the stock market. This chart demonstrates the problem.

CRF Lags the S&P 500 in the Short Term …

CRF tries to track the S&P 500’s performance and translate its returns into big dividends. But since its yield is more than double the S&P 500’s overall annualized historical performance, CRF can’t keep up, and the value of its portfolio erodes over time. When investors see this happening, they sell, which exacerbates the problem. Thus, CRF’s long-term returns are a fraction of the S&P 500’s, and the further back you go, the worse it gets.

… And the Long

Reason #3: Its “Big Yield” Doesn’t Last

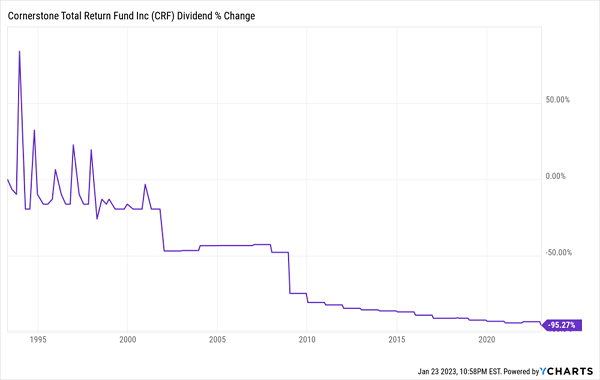

Finally, let’s tackle that dividend. Since CRF’s big yield is its main draw, we want the fund to maintain its payout so we don’t take a pay cut. In reality, that’s not how things have played out.

CRF Lets Down Income Investors, Time and Again

CRF has cut payouts by over 95% since inception, with annual dividend cuts being standard operating procedure at the fund. And things are getting worse.

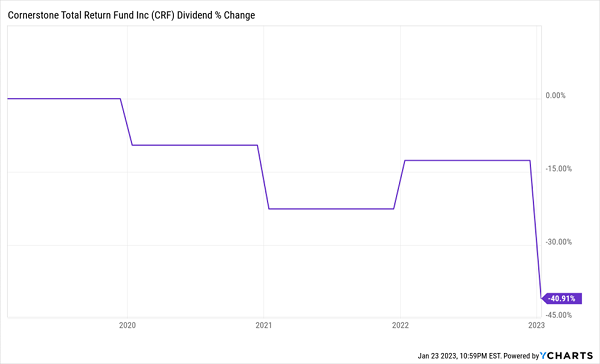

CRF Payout Cuts Get Steeper

During the pandemic, CRF cut its dividend mostly in line with the trend established over the last decade. But suddenly in late 2022, CRF made one of the most drastic cuts in its history.

If you bought CRF three years ago, you probably felt great about your 19.7% dividend yield. But these payout cuts mean you’re now yielding just 15.8% on your original buy. That’s still a high number, but it also represents a big reduction. A million bucks in CRF just went from yielding $197,000 a year to $158,000. That’s a full $3,250 per month less—in just three years!

Plus, your million-dollar investment in CRF would now be worth just $851,000.

The takeaway: if a CEF’s high yield sounds too good to be true, it’s worth doing more digging. And CRF, beyond its high yield, gives us a good list of flaws to look for, including historical underperformance, an unsupported premium and a history of dividend cuts. If you see any or all of those warning signs, you’re best to move on.

5 Monthly Dividend CEFs That Crush CRF—and “Regular” Stocks, Too

Instead of CRF, I urge you to take a look at the 5 monthly paying CEFs I’m pounding the table on now.

In addition to monthly payments, these 5 funds yield a steady 8.9% today—enough for many folks to generate a livable income stream on just $500K saved.

Sure, it’s no 19% payout. But the fact that these funds are likely to soar (I’m expecting 20%+ returns this year, thanks to their deep discounts), rather than plunge like CRF, more than makes up for it.

I can’t wait to tell you about these 5 proven moneymakers. Click here and I’ll show you how to download a free Special Report with all of my research on these 5 ultra-reliable—and monthly paying—CEFs.

Recent Comments