Volatility is high, stocks are shaky and there’s a major land war in Europe. So we’ll take a pass on the highflyers, thanks.

Give us the monthly dividends instead.

Of course, easy enough for us to say. We “retire on dividends” folks have spent years building up a nest egg that would last us forever. Now, it’s time for us to turn this pile of cash into cash flow.

I’m talking about dividend payers that will keep on paying no matter what happens around the world. We’ll discuss some elite monthly dividend payers in a moment—the types that will dish us 9.8% per year, paid every 30 days.

(That’s $98,000 annually in dividends on a million portfolio, or $49,000 in yield salary on a $500K nest egg.)

We’ll get to this trio in a moment. First, let’s appreciate monthlies.

High Monthly Dividends = Peace of Mind

Most dividends pay once every three months. Problem is, our bills come in monthly. Mortgage? Monthly. Water? Monthly. Car? Monthly. Cable?

Every 30 days, we need to pay. No good when we’re getting paid every 90.

Enter monthly dividend stocks (and funds), which do exactly what the name suggests—they write out a dividend check each and every month, in line with your average Joe’s responsibilities and commitments.

… And that’s it. There’s typically nothing else different about these companies and funds other than how often they serve up cash.

Check out the table below. Up top is the dividend schedule for an extremely generous 9.8%-yielding dividend portfolio made up of “normal” stocks. Below that is the income from a trio of dividend stocks and funds yielding the same amount, just delivering it each and every month. Both deliver roughly $49,000 in annual income—not on a million-dollar nest egg, but on a mere $500,000 investment.

I know which one I would pick, and it’s not because of the extra 20 bucks.

But ultimately, what matters most is whether these high-yielding monthly dividend payers aren’t just dividend traps in disguise. After all, what good is a giant yield (monthly or otherwise?) if the checks won’t last?

So today, we’ll look at three monthly dividends averaging nearly 10% in yield to see whether any of them make the grade for a reliable retirement portfolio.

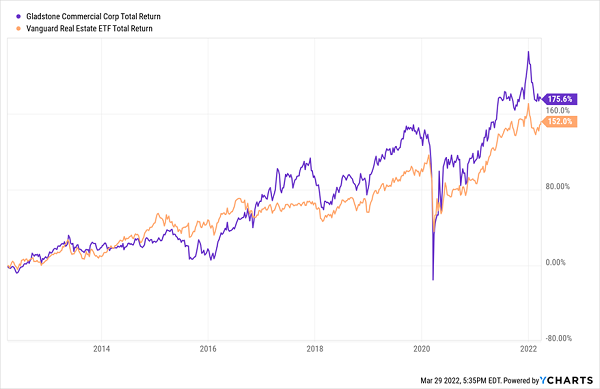

Gladstone Commercial (GOOD)

Dividend Yield: 7.0%

Gladstone Commercial (GOOD) is a member of the Gladstone Companies: a group of publicly traded investment vehicles that also includes:

- Gladstone Investment Corporation (GAIN)

- Gladstone Capital Corporation (GLAD)

- Gladstone Land Corporation (LAND)

Each of these funds invests in (and buys) lower middle market companies in the commercial and/or farmland real estate space.

And each one pays out a monthly dividend.

Gladstone Commercial is a real estate investment trust (REIT) that invests in single-tenant and anchored multi-tenant net-leased industrial and office properties. Its portfolio currently consists of 129 properties in 27 states, leased out to 108 different tenants spanning 19 industries. Telecommunications makes up 16% of the portfolio, followed by conglomerate/diversified services and automotive tenants at 13% apiece. Healthcare, manufacturing and building each earn single-digit exposure. The rest of the portfolio is spread across 13 other industries.

One of Gladstone’s biggest draws is how active a landlord it is. Rather than just sitting back and collecting rents, its management team will help tenants with everything from upgrading their parking lots to literally expanding buildings. And it even goes a step further: “We create value for our tenants by reducing operating expenses via tax appeals, national purchasing power, sustainability initiatives and energy audits.”

I’d be remiss not to point out that GOOD missed on its most recent quarterly revenues. Occupancy also slipped…but to a still-healthy 97.2%, and this is a company that almost never lets occupancy slip below 95.0%. All’s still well.

More encouraging is that shares have lost some of their froth of late. This long-time outperformer in the REIT space currently trades for 14 times estimated funds from operations (FFO, a critical REIT profitability metric). That’s not a screaming bargain, but it’s a better current deal than the overpriced REIT sector as a whole.

Gladstone Is a “GOOD” Egg in the Real Estate Space

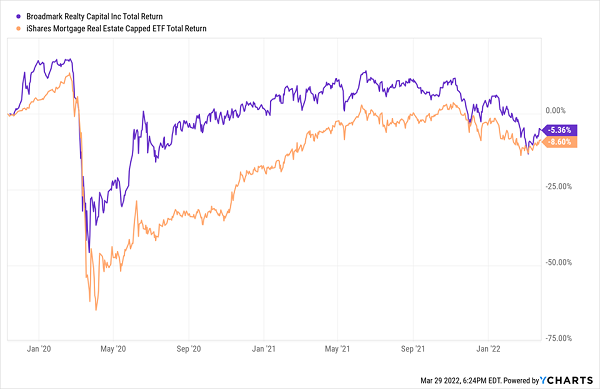

Broadmark Realty Capital (BRMK)

Dividend Yield: 9.8%

Broadmark Realty Capital (BRMK) is a mortgage REIT (mREIT) , which differs from your garden-variety REIT in that deals in paper rather than physical properties. Specifically, it borrows money at short-term rates to buy bundles of securitized mortgages that in turn drip down cash at (hopefully higher) longer-term rates. The difference between those rates (“net interest income,” or NII) is the mREIT’s profit.

But if we’re being accurate, Broadmark isn’t your typical mREIT.

BRMK is more of a money lender that specializes in a variety of loans. Its primary business is construction loans, though it also offers heavy rehab/redevelopment loans, land development loans, and bridge financing and construction completion loans. These loans are provided to builders, and most of the time, they’re looking for a quick turnaround, which allows Broadmark to set pretty high rates.

You’d think that, in the midst of a booming housing market, that BRMK would be off to the races. And it was, for a moment.

Post-COVID Housing Surge Lifted BRMK (For a Time)

In Q2 2020, for instance, BRMK told investors that “COVID-19 has stimulated demand for housing stock at historic levels which is driving residential construction and, in turn, loan growth.” Not bad.

Of late, however, the business has been weighed down by non-accruals (typically, loans in which principal and/or interest is at least 90 days past due). That’s likely to weigh on earnings in the short-term, and that—as well as the prospects for rising rates—have in turn hampered the stock, and could keep it anchored for several quarters to come.

But keep your eye on the young Broadmark, which came public just a few years ago, in 2019. Non-accruals eventually will be resolved, and if it can get through this rough patch with its monthly dividend still intact, it could be a much more attractive long-term prospect.

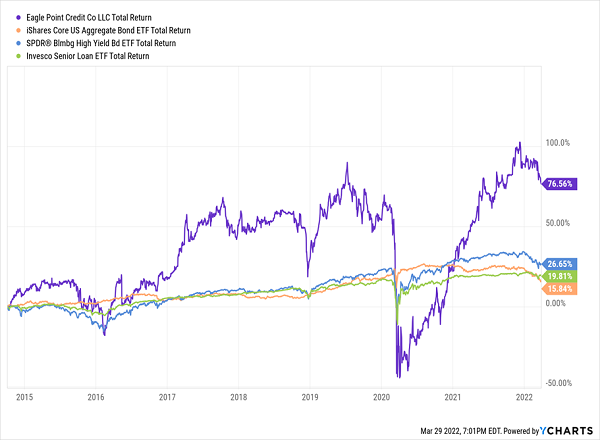

Eagle Point Credit Company (ECC)

Dividend Yield: 12.5%

Eagle Point Credit Company (ECC) pays monthly, but it’s a black box, to put it lightly.

ECC is a closed-end fund (CEF)—and while I’ll tell you that CEFs are superior to exchange-traded funds (ETFs) for any number of reasons, one way in which they fall short is transparency. CEFs aren’t nearly as forthcoming about their holdings, which means it’s more difficult to peek at what’s inside; you just have to trust the manager knows what they’re doing.

On top of that, ECC invests in a particularly murky asset—collateralized loan obligations (CLOs)—that, among other things, makes it difficult to compare to most other types of fixed-income solutions.

But Generally Speaking, The Rewards Can Be Richer

CLOs are effectively securitized pools of business loans—typically first-lien senior-secured bank loans, though they can include second-lien loans and even unsecured debt. Within the CLOs, there are different tranches of debt with varying risks, as well as an equity tranche. Eagle Point Credit primarily invests in the equity and junior debt tranches.

In short, it’s virtually impossible for the average investor to get a clear picture of the underlying portfolio, let alone analyze it.

That’s where the trust part comes in. And to management’s credit, they’ve been able to put up much stronger longer-term returns than just about any type of fixed income product out there, in part thanks to a massive yield well above 12%.

But it’s no picnic—ECC is rife with volatility, which you can at least partially chalk up to extreme leverage above 30%. It’s expensive, too—not only does the fund charge a whopping 9.7% in annual fees (management, interest and other expenses), but ECC currently trades at 5% above NAV, meaning you’re paying $1.05 on the dollar for this portfolio.

Your 2022 Guide to Retirement Riches: 7%-Yielding Blue Chips That Pay EVERY MONTH

This group of monthly payers has a couple of interesting prospects. But if you’re trying to renovate your retirement portfolio into a worry-free source of high, sustainable income, you can’t deal in “potential”—you need proven, blue-chip monthly payers whose yields have already survived the test of time.

You need to know, rain or shine, that a sizable dividend check is hitting your mailbox each and every month. No exceptions.

You need the “A” squad: diversified, reliable payers of mouthwatering yet dependable income that don’t knuckle under every time the economy throws a fit.

And you can find these rare monthly dividend blue chips in my “7% Monthly Payer Portfolio.”

Many of the picks in my “7% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate not just massive yields, but shockingly aggressive price performance. The upshot is that we can do the unthinkable from an income strategy:

We can double our money much more quickly than traditional blue-chips-and-mutual-funds portfolios.

And the dividends?

They’re not just good. They’re not just great. This is life-changing income.

Do the math: Even if you have just a $500,000 nest egg—that’s less than half of what most financial gurus suggest you need to retire—into this powerful portfolio now, you can kick-start a $35,000 annual income stream.

That’s nearly $3,000 a month in regular income checks!

Even better? The market’s recent antics have provided us with a rare gift, pulling all of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to get everything you need—names, tickers, complete dividend histories and more on these monthly dividend payers—right now!

Recent Comments