We’ve just hit the best time of the year to roll out one of our most potent dividend “hacks.” Timed just right, it’ll deliver us stout payouts yielding upwards of 5%—and growing triple-digits, too.

Best of all, we can “work” this proven dividend-growth system in just two quick steps, which we’ll dive into now. Then I’ll name three stocks you can buy today to give yourself a shot at “front running” double-digit payout hikes—and swift capital gains, too!

Step 1: Buy Just as a Dividend Hike Is Announced

We’ll start by “timing” our buys just as dividend hikes are announced. That’s a veteran move because a company’s shares almost always rise with its payouts, and there’s often a lag between the announcement of the hike and a rise in the stock.

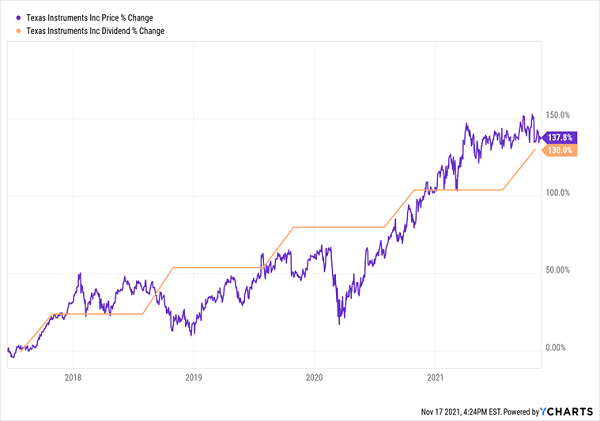

You can see this set-your-watch-to-it pattern in shares of Texas Instruments (TXN), a holding of my Hidden Yields service that’s delivered 138% price gains (and 168% total returns) since we bought it in June 2017.

You can see the pattern in action in the chart below, with a slight lag between when the dividend jumps and the stock price follows suit. That’s our window to buy, just as first-level investors are catching on and bidding up the stock:

TXN’s Dividend Telegraphs Its Next Price Move

This is Step 1 of our dividend-and-price-gain tango—buy shares of reliable dividend growers just before they announce hikes. And because management loves to reward investors near year-end, we have a raft of them to choose from—we’ll look at three specific year-end dividend raisers below.

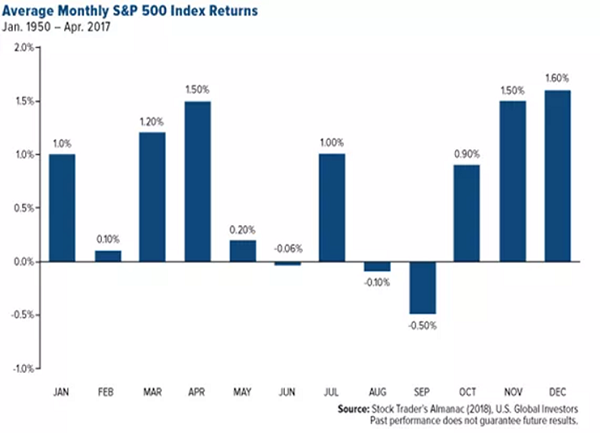

We’re also perfectly set to profit here because we’re entering three of the best months on the stock market.

According to 1950 to 2017 numbers from the Stock Trader’s Almanac, November and December are the two best months for stock performance, with average gains of 1.5% and 1.6%, respectively. January is historically a strong month, too, with a 1% gain, tying it for fourth spot.

Step 2: Add a Low Payout Ratio for the Strongest Dividend (and Price) Gains

So we’ve got a predictable dividend-hike pattern and seasonality working in our favor. Next we want to look for a reasonable payout ratio, which is the percentage of free cash flow (FCF)—the best snapshot of the cash a company is generating that there is—that’s absorbed by dividends. When it comes to dividend safety, I demand a ratio below 50%—and for maximum dividend growth, the lower, the better.

Now let’s dive into three names that tick our boxes, with a strong likelihood of announcing big dividend hikes in December, plus the financial strength to double (or more!) their payouts in short order.

Abbott Dividends—and Shares—Set for a Second Big Pop

Medical device maker Abbott Laboratories (ABT) sent a message last December when it delivered the biggest payout hike in its history—a 25% boost that instantly bounced its stock to all-time highs last year:

December 10 Payout Raise Could Top Last Year’s 25% Hike

Over the past five years, Abbott has inflated its dividend by 70%, driving the yield on a buy made then to 4.4% today, far higher than the 1.4% the stock yields now.

This year, you’ll want to circle December 10 on your calendar, as it’s the second Friday of the month—right when Abbott announced its double-digit hike last year. Because a second big boost is likely on the way.

I say that because the company posted solid third-quarter results, with total sales soaring 23.4% on double-digit gains across its divisions. The diagnostics business stole the show, thanks to healthy sales of its BinaxNow and Panbio at-home COVID-19 tests and its ID NOW COVID testing system for clinics and doctors’ offices.

Even without COVID tests, sales still rose a healthy 11.7%. Free cash flow has also been soaring, another factor pacing the stock higher (and resulting in Abbott’s extremely low FCF payout ratio of 33%):

FCF Powers the Share Price—and Our Dividends

Finally, don’t be put off by Abbott’s seemingly high P/E ratio of 31.9—it’s actually a bargain in disguise! Last year at this time, the stock traded at a “nosebleed” 60-times trailing-12-month earnings and still delivered that big payout-driven pop we just saw. This year, with an even better valuation, I’m expecting more.

A Canadian Bank With a Pent-Up Payout Hike

Canada’s banks are an untapped resource for many US investors, and I’ve always wondered why. For one, they tend to yield more than their American cousins—take Toronto Dominion Bank (TD), which yields 3.5% as I write this, compared to 2.4% for JPMorgan Chase & Co. (JPM) and a mere 1.6% for Wells Fargo (WFC).

TD is Canada’s most “Americanized” bank, with roughly the same number of branches south of the border as in its own country (around 1,100 in the US, compared to 1,085 in Canada).

TD’s Canadian and US businesses are also profiting both from higher trading volumes and strong loan originations. TD is also nicely positioned to profit on the gap between rising yields on the 10-year Treasury note (and in Canada the 5-year government bond), which dictates interest rates on loans it makes to customers, and near-zero overnight rates set by the Federal Reserve (and Bank of Canada), at which banks lend to each other.

The real catalyst is that TD and other Canadian banks have just been cleared by the Canadian government to resume dividend hikes as the worst of the COVID-19 crisis recedes. Given the bank’s long dividend history (it’s been paying dividends since 1857) and strong business performance, we can expect a hike to be announced any day—and it’ll likely eclipse the 7% increase (in Canadian dollars) the bank last announced, pre-COVID.

Let’s Gear Up for Our Progressive Special Payout

Our Hidden Yields members will know Progressive (PGR) well. The auto insurer uses a sneaky-smart strategy to discern, via an algorithm, if a new customer is worth insuring. If they’re too risky, it tosses out a high quote, giving the company two ways to win: the customer either takes the quote or moves on to (and becomes a problem for!) one of its competitors.

The company applies the same strategy to its payout, yielding $0.10 per quarter, but paying the bulk of its dividend as a special payout that rolls out in early December (or thereabouts). Factor in last year’s special payout and you get a hefty 5.4% trailing-12-month dividend yield. And with an FCF payout ratio of just 37%, Progressive has plenty of room to roll out another healthy “special” this year.

Finally, like TD, Progressive benefits from rising interest rates because it invests its “float” (or the premiums it collects) in safe interest-bearing securities, as claims will need to be paid out at some point.

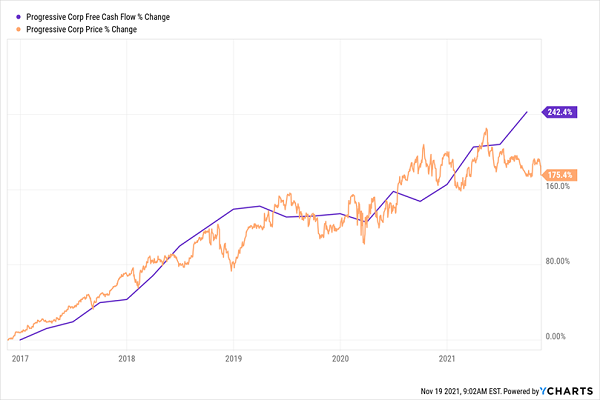

Progressive’s FCF Powers Its Payout

Finally, as you can see above, its cash flow has been growing strongly: FCF per share is up 242% over the past five years, and like dividend growth, is another strong driver of future share price increases.

These 23 Stocks Are Primed for Big Dividend Hikes (Starting Soon)

I’ll give you my latest buy/sell/hold advice on Progressive and the other 22 dividend growers in my Hidden Yields portfolio when you take advantage of my special invitation to road test the service with no risk and no obligation!

Plenty of these stocks are on the verge of announcing their next big payout hike, and I don’t want you to miss any of the action.

That’s not all: I also want to give you my latest free investor report outlining the 7 dividend growers I’ve hand-picked to deliver you a steady 15%+ in gains and dividends a year, no matter what the market does.

These 7 dividend growers are especially critical to hold today, as their rising dividends keep your income stream ahead of inflation while powering their share prices higher, too!

Full details on all 7 are waiting for you now in your free investor report. Click here to get your copy, which includes their names, tickers, best-buy prices, current yields and complete dividend histories. And you’ll get a chance to try Hidden Yields with no risk and no obligation, too!

Recent Comments