A dividend hike is the ultimate sign of dividend safety. It’s also the surest, safest way to “get rich soon-ish” in stocks.

Find me stocks that are raising their dividends quickly and regularly, and I’ll show you some stocks that are doubling every few years.

What drives the dividend? Well, the likelihood that a company is going to raise its dividend (or cut it) is directly related to its payout ratio, or the percentage of its profits that it is dishing out to shareholders as dividends.

As a rule of thumb, a payout ratio below 50% is a sign of dividend safety. Some capital efficient firms can pay more and real estate investment trusts (REITs) can pay up to 90% of their cash flows as dividends.

It depends on the company (and if you don’t feel like following the payouts and cash flows of a portfolio of stocks and funds yourself, I’ll gladly do it for you as part of your Hidden Yields subscription!).

We’ll get greedy in a moment. First, here’s what we avoid—dividend cuts.

Payouts that get punked are no fun. Not only are they a pay cut for us, but (worse) they destroy capital. Take the case of CenturyLink (CTL), which has been writing its investors dividend checks that it couldn’t cash since I called out this “paper telecom tiger” in May 2016 (and many times since!)

At the time, CTL was paying out 135% of its earnings as dividends. The company wasn’t growing profits, either, so the payout eventually had to go. Mr. Market eventually sniffed this out and CTL’s management team finally made the inevitable cut a few years back:

Stocks Rise and Fall with Their Dividends

Unfortunately for CTL’s “income” investors, their stock’s price dropped 59% while they received a 54% pay cut!

That’s no good. Show me the (rising) money, Jerry!

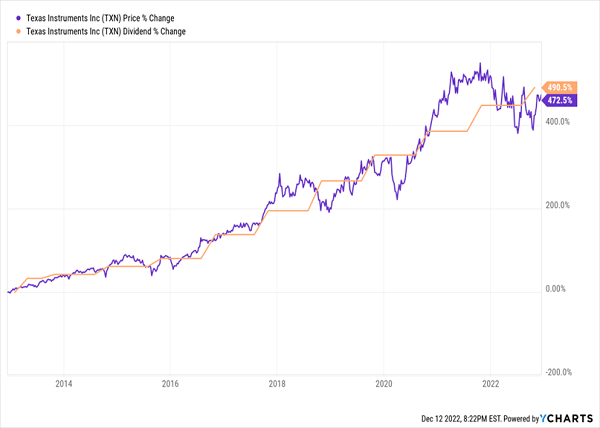

Texas Instruments (TXN) is the opposite case. For the past decade it has mostly boasted a payout ratio below the 50% mark. Which is good—it means the company had “cash fuel” for future dividend hikes.

And hike TXN did! Here’s how we calculate a 491% dividend increase—with a perennially-low payout ratio. (Notice how the stock price follows that payout higher like a devoted puppy dog. Thank you, “dividend magnet.”)

This Virtuous Cycle Drives Market-Beating Total Returns

So, where do we find the next TXN and double our money every few years?

By finding fast dividend growers with low payout ratios today. The faster the increases, the better. And the lower the dividend-to-profit ratio, the better.

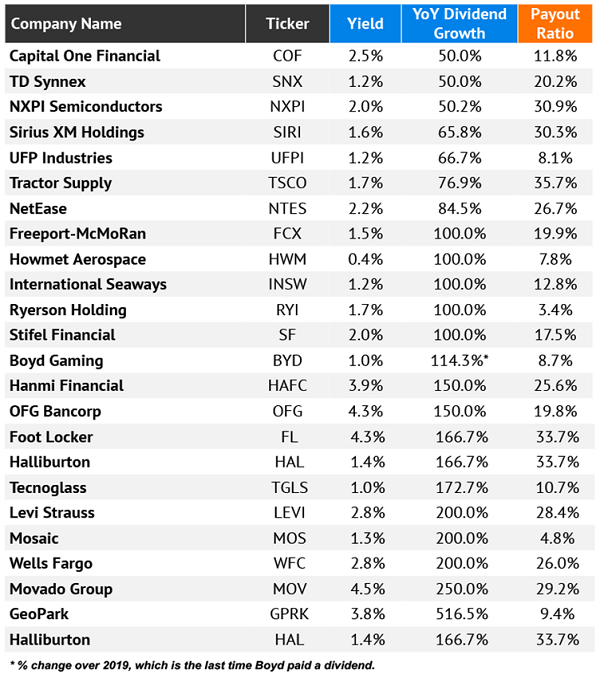

And wouldn’t you know, we have 23 nice-looking dividend growers to consider as we head into 23! All of them have raised their payouts at least 50% over the past year (that’s no typo).

All have payout ratios below 40%. Even better than TXN did during its epic run! Here’s the list:

Note: % dividend change calculated between start of 2021 and December 2022

Source: S&P Global Market Intelligence

We have a large number of financial companies on this list. Mega-banks such as Capital One Financial (COF) and Wells Fargo (WFC) would seem unlikely candidates for massive payout moves given their every-year need to pass the Fed’s financial stress tests. But Wells has moved its dividend higher multiple times since the start of 2021, from 10 cents per share to 30 cents—a tripling!—albeit from a very low starting point following its 2020 cut. Capital One is a similar story, also briefly cutting its payout to 10 cents in 2020, then ramping up again from there.

And the list is not without irony! We even highlight brick-and-mortar retailers in the year 2022. Several are ramping up their payouts, though their stories aren’t the same. Foot Locker (FL) has delivered 167% dividend growth, from 15 cents quarterly to 40 cents, since 2020—when it cut its dividend from 40 cents.

We must respect the consistency of Tractor Supply (TSCO). TSCO has scrawled out 14 years of higher profits in the past 15 (2017 being the lone exception), and the payout has done nothing but head higher since Tractor Supply began distributing dividends in 2010. Its latest bump? 77% to 92 cents per share, and it should announce its next hike sometime in January. CEO Hal Lawton says more millennials are embracing the “out here lifestyle”; that can only mean good things for the still-expanding rural-goods retailer.

And remember TXN? It’s still here.

Tech is an unsung hero of dividend growth. NXPI Semiconductors (NXPI) is perhaps the most noteworthy name here. In 2018, a buyout deal with Qualcomm (QCOM) was scuttled; shortly thereafter, the company announced its first dividend: a 25-cent payout that has since exploded by more than 230%. NXPI has heavy automotive exposure (more than a third of revenues), a sub-13 forward P/E and a very flexible payout ratio of just more than 30%.

7 Stocks That Could Double Their Prices … And Triple Their Dividends

All of the stocks above have the power to harness what I call the “Dividend Magnet”: The market forces that turn profitable companies into a virtuous and violent cycle of rapid dividend and share-price growth.

But they’re what I would call the “B squad.” All of them boast attractive traits and the potential to pop off in the years ahead—but all of them have enough concerns that I’m not quite ready to pounce.

That’s not the case for the “A squad”: 7 overlooked “Dividend Magnet” stocks that are poised to deliver two incredible financial feats:

- Double their stock prices in five years or less

- Triple their dividend payouts in the same time

My Dividend Magnet strategy is pretty simple—in fact, it’s made up of just three signals. And if a stock throws off all three of these telltale signs, it’s time to buy with both hands—and then hang on tight with both hands as the company’s dividend balloons and its share price screams higher.

And not only am I going to give you the seven Dividend Magnet picks above—I’m going to show you, step by step, exactly how the Dividend Magnet has uncovered break-neck returns of 61%, 112%, even 148%, so you can identify even more opportunities!

Personally, I think triple-digit gains are squarely on the table with these 7 hidden gems. But conservative sort that I am, I’m forecasting steady 15%+ annualized returns for the long haul. That’s enough to double our investment every five years and triple our income stream, too.

We’ll happily take that deal!

Want to learn more? CLICK HERE and I’ll reveal my Dividend Magnet strategy, as well as introduce you to these seven dividend-growth dynamos.

Recent Comments