Election chaos—especially after Friday’s bombshell—could be a knockout blow for this market bounce. I’m worried. And going by our Contrarian Outlook mailbag, plenty of readers are, too.

A typical question goes like this: “Brett, what should I buy/hold/sell if X/Y/Z happens after November 3?”

Now we have to add the president’s positive coronavirus test into the mix!

Rest easy—I’ve got you covered. Today we’re going to talk about two stocks you could hold through 2021, 2022, 2023, and beyond. These companies’ current dividends are much higher than the S&P 500 average. But the real story is their dividend growth, which will triple up your income stream in short order.

And Friday’s news only emphasized how important stocks like these are today, because this duo is set for any political or economic future, for one reason: they’re what I call “tollbooth stocks.”

Steady “Tolls” Are the Cure for a Scared Market

Tollbooth stocks are the kinds of companies we safety-conscious dividend investors love: they hold the infrastructure—think pipelines, warehouses and data networks—big players like, say, Amazon.com (AMZN) must have to operate.

These quiet “toll collectors” hand over most of the cash they collect to us in the form of rising dividends. Buying these stocks is also much safer than playing “whack a mole” and trying to pick individual winners in hyper-competitive industries.

To show you what I mean, let’s dive into our first “tollbooth” stock, which is riding the pandemic-driven surge in mobile-data demand. It’s also cashing in on the shift to ultra-fast 5G networks, which will march onward no matter who’s president:

Tollbooth Dividend Play No. 1: A 242% Dividend Grower With a 5G Kicker

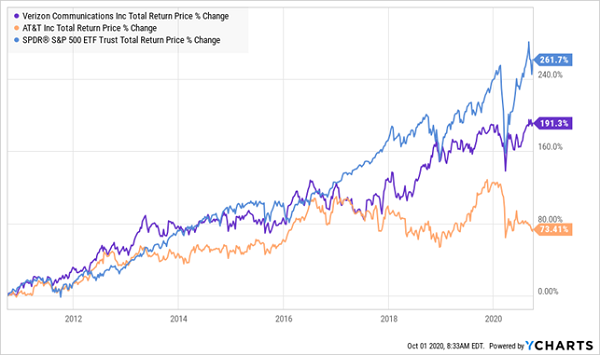

When most people look for a telecom stock to buy, they go straight to Verizon (VZ) and AT&T (T). The appeal is obvious: both pay dividends far in excess of the market average (a 4.2% yield for Verizon and a whopping 7.3% payout for AT&T).

Now, in exchange for payouts like that, you might expect some underperformance. (Though to be honest, I wouldn’t settle for any!) But this is ridiculous:

A High Price for High Yields

If you’d simply bought an index fund a decade ago, you’d have 37% more in gains and dividends sitting now than if you’d bought Verizon. AT&T’s colossal dividend didn’t help its shareholders, either: index-fund buyers clobbered them by 252%!

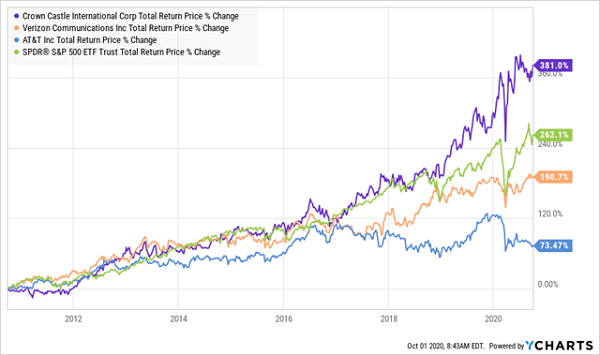

When you add our first tollbooth play, Crown Castle International (CCI)—in purple below—to the picture, the smarter move becomes clear:

Crown Castle Versus Everyone

Crown Castle is a real estate investment trust (REIT) with 40,000 cell towers and 70,000 small-cell nodes. The latter are “mini-towers” that boost capacity and service quality in a particular area and are vital to the deployment of next-gen 5G networks. All the major telcos pay “rent” to CCI, including AT&T and Verizon.

Plenty of investors are put off by CCI’s comparatively low 2.9% yield. But that masks the real dividend picture: CCI’s payout has surged 242% in just the past six years, putting AT&T and Verizon to shame.

Put it this way: if you’d bought CCI in 2014, you’d be yielding 6.5% now. And that payout is primed to rise again: CCI regularly announces dividend hikes in mid-October, and last year’s boost came in at a healthy 7%.

Expect another hike this year: the payout accounts for 83% of adjusted funds from operations (FFO), which is reasonable for a REIT, and 78% of the FFO management expects to generate in its full 2020 fiscal year.

Tollbooth Dividend Play No. 2: A “Megatrend” Stock That’s Doubled Its Payout

No matter what happens with the election, we can be sure of one thing: healthcare spending will keep rising, even after the pandemic.

According to April numbers from the Center for Medicare & Medicaid Services, the US will spend 5.4% more on healthcare every year, on average, to 2028, dwarfing both inflation and GDP.

Pharma stocks are poised to grab a slice of that cash, but picking winners here is no cinch: many treatments fail in the testing stage: according to a study published in Biostatistics in April 2019, for example, a staggering 96.6% of developmental oncology drugs never made it to market from January 1, 2000, to October 31, 2015.

And when a drug flunks, it takes all the R&D cash management has invested with it! This is why pharma companies have to dump huge sums into development. Merck & Co. (MRK), for example, spent $10 billion in its last 12 months of earnings, or more than 21% of its sales.

I’m no medical researcher, so I work around this problem in a couple ways. One is to farm out pharma picks to a closed-end fund (CEF) run by expert managers.

The Tekla Healthcare Opportunities Fund (THQ), which I told you about last week, is a good example. It’s run by a team of pharma and finance pros and pays a 7.8% dividend that comes your way monthly.

THQ also trades at a 10.8% discount to net asset value (NAV), so you’re getting its portfolio of blue-chip pharma names for 89 cents on the dollar.

But there’s another approach, and it comes back to our tollbooth analogy: skip stock-picking altogether and buy into a company that collects a rent check whether a treatment passes or fails. Lab owner Alexandria Real Estate Equities (ARE) is a great example.

Alexandria’s tenants include pharma giants like Pfizer (PFE), Eli Lilly and Co. (LLY) and Novartis (NVS) but also medical-device makers like Thermo-Fisher Scientific (TMO), Quest Diagnostics (DGX) and Abbott Laboratories (ABT).

Abbott, you’ve probably heard, just had its rapid test for COVID-19 approved. Abbott’s shares are pricey, at 33-times earnings. But investing in the COVID-19 fight through Alexandria, whose tenants are almost all involved in some way, lets you sidestep trying to pick future winners in this intense race.

Alexandria Tenants Involved in COVID-19 Treatment

Source: Alexandria Real Estate Q1 earnings presentation

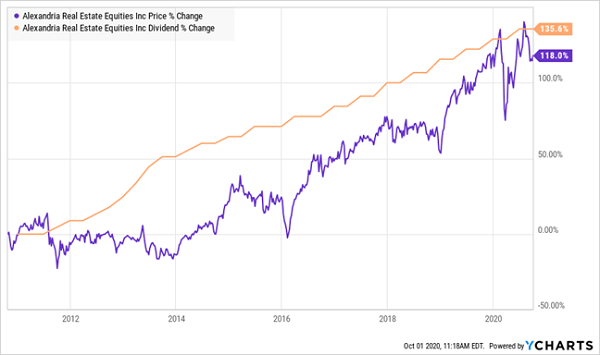

Rising demand (and rents) for labs should continue to spur Alexandria’s payout growth. As you can see below, the REIT regularly raises its dividend twice a year, and the dividend has doubled in the last decade. That’s driven an almost identical rise in the share price.

This Toll Collector Pays You 2 Ways

Like CCI, Alexandria boasts what (at first) looks like a ho-hum dividend yield of 2.5%. But also like CCI, its soaring dividend growth will boost the yield on a buy made today. If you’d bought 10 years ago, you’d be pocketing a 6.1% yield now.

Finally, the REIT pays out just 57% of its FFO as dividends, so safety isn’t a worry—and we can look forward to continued payout growth.

5 “Recession-Resistant” Stocks Paying 8%+ [Your Chance Is Vanishing Fast!]

I can’t stress enough how perfect stocks like Crown Castle and Alexandria are for times like these. “Tollbooth” plays let us stay in the market and collect a growing income stream, too.

That’s far better than what most folks are doing: sitting in cash, grinding their teeth wondering when to get back in. Let’s be honest, 99% of these investors will miss the bottom of this latest dip … and lose out on the biggest gains, too.

This is why permabears almost always lose money in stocks: they wait too long to get back in!

But holding long-term “tollbooth” plays, or CEFs like THQ (which gives you most of your return in cash, thanks to its huge 7.8% yield), are the answer to this problem.

And these aren’t even my best dividend buys for these trying times. Those would be the 5 stocks in my “Recession-Resistant Portfolio.”

These 5 stout buys yield 8%, on average, and they ALL trade at huge discounts. Those bargain valuations are critical—they help throw a floor under these 5 stocks’ prices and give you peace of mind while you collect your rich 8%+ cash dividends.

Best of all, you’ll get your first dividend in just a few weeks (many of these solid buys pay monthly!), while your friends sit in cash, watching helplessly as inflation slowly erodes their nest eggs.

Recent Comments