When a market storm hits, we dividend investors can protect our wealth and grab steady payouts when we buy stocks backed by strong recurring revenue.

It’s one of the oldest business models there is! Here’s how it works: customers pay for the services these companies provide every month, year or whatever, which gives them predictable—and ideally growing—profits.

What’s more, these payments are “sticky”: once buyers start making them, they’re quickly “out of sight, out of mind,” automatically pulling from their bank accounts (or dropping onto their credit cards) on the regular.

(I’ll show you two such firms in a moment, one of which is converting its recurring revenue into a recurring payout that soared 88% in just two years. Another is paying one group of lucky buyers an astonishing 22.2% yield!)

If this all sounds simple, it’s because it is. And you can find the best “recurring revenue” buys by looking out for three “must haves” (besides a top-quality product customers can’t live without, of course!):

- A growing dividend, which tends to pull a company’s share price higher. In times of crisis, a rising payout is a sign of a healthy business, which draws frightened investors in.

- Rising profits (and better yet free cash flow, a snapshot of cash generation that can’t be manipulated) to back that rising payout and, in turn, our upside.

- A safe payout ratio: I demand that “regular” stocks (i.e., those outside the real estate investment trust market) pay no more than 50% of free cash flow as dividends.

You can give yourself an extra upside kick when you buy recurring-revenue stocks just as they’re being forged, as we’ll see next.

Buy During This Rare “Window” for Big Upside

For companies, switching to subscriptions is a classic case of short-term pain for long-term gain: their revenue will drop as they “break out” a sale over 12 months instead of getting it in one transaction.

And if you buy during this transition, before the mainstream crowd realizes what’s going on, you can set yourself up for some very nice gains indeed.

For example, at some point over the last decade, you’ve probably read about the switch over to subscriptions at Adobe (ADBE).

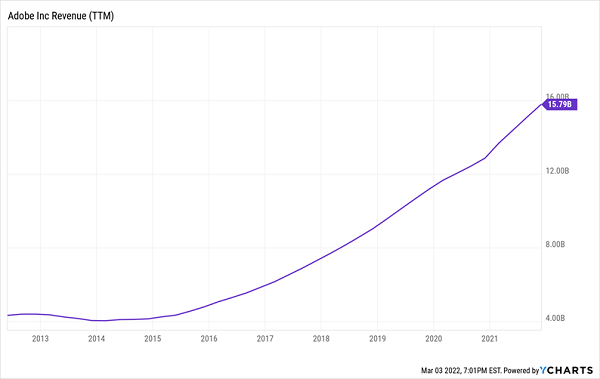

In 2011, when the company launched its Creative Cloud service (or its graphic design software by subscription), less than 20% of its revenue was recurring, according to research firm McKinsey, so most of its users were still buying one-off software packages. Fast-forward to its fiscal fourth quarter, which ended December 3, 2021, and recurring revenue was 93% of the total.

Adobe’s Smooth-as-Silk Recurring Revenue Stream

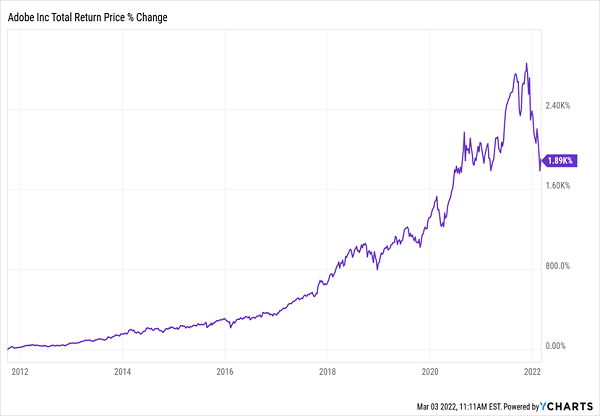

The stock tracked the shift, treading water at first, then soaring to a near-1,900%+ gain, even with the hit tech stocks have taken in the last few months.

Subscription Shift Ignites Adobe’s Stock (Once the Crowd Catches On)

I can’t recommend Adobe today, trading as it does at 46-times forward earnings (and paying no dividend!). So we’ll tip our hats to our lucky Adobe buyers and look to other “sticky” businesses instead, like the two we’ll talk about now.

Recurring-Revenue Pick #1: A “Boring” Stock Just Starting a Subscription Shift

Subscribers to my Hidden Yields service are seeing an Adobe-like shift from Carrier Global (CARR), a heating and cooling firm that’s teamed up with Amazon.com (AMZN) on its recently released Lynx Digital Platform.

For 106 years, Carrier has peddled its HVAC wares transactionally. Sell an air conditioner, collect the cash, rinse and repeat. With its partnership with Amazon Web Services (AWS), it’s pivoting toward the magic of subscriptions.

Here’s the gist of the partnership: consider the fact that we lose 475 tons of food each year to improper refrigeration, according to the International Institute of Refrigeration. (Yes, they have a trade society for everything.)

Enter Lynx, with a mission to provide customers with visibility across the entire “cold chain” (great term), helping with tasks such as:

- Matching food producers with the ideal refrigerated trucks for transport,

- End-to-end route planning, and

- Preventing spoilage thanks to its visibility into, and ability to access, the entire supply chain.

The “platform” moniker is what should warm our hearts as investors because “platform” is just another way of saying “recurring revenue.” (I learned this when I was pitching venture capitalists for my own first start-up a decade ago. Always say you’re building a “platform” and you’ll command VC attention!)

88% Payout Hike Attracts Investors in Hot and Cold Markets

Meantime, the company continues to, er, deliver for us Hidden Yields members on the dividend front. It doesn’t get much attention from the income crowd because of its low 1.1% yield, but that masks its strong payout growth: Carrier hiked its dividend by 25% in December and 88% in the past two years alone.

Those dividend hikes help throw a floor under the share price in tough times, as the company’s rising payouts attract new investors. They also give it an extra kick when markets (inevitably) rise again.

Recurring-Revenue Pick #2: A REIT That’s Quietly Built a Safe 22.2% Dividend

REITs, which rent space ranging from warehouses to office buildings and malls, are the quintessential recurring-revenue stocks, due to the steady rent checks their clients pay. A good corner of the space to play right now is self-storage, which is profiting as people load up on consumer goods.

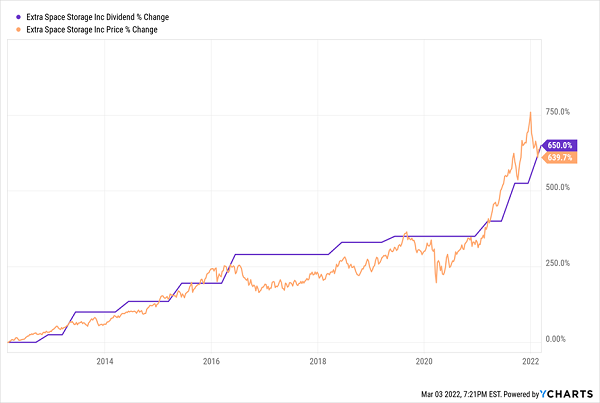

Self-storage REIT ExtraSpace Storage (EXR) is in the thick of that trend: it yields 2.7%, which is already 100% more than the average S&P 500 stock pays, but has boosted its payout a phenomenal 650% in the last decade. In other words, if you bought then, you’d be raking in an incredible 22.2% yield on your original buy.

We can see EXR’s rising payout pulling its shares higher—the pattern is unmistakable:

EXR’s Recurring Revenue Drives Explosive Payout (and Price) Growth

ExtraSpace can easily keep this roll going, with its high 97% occupancy rate and its dividend accounting for a reasonable 77% of the midpoint of forecast 2022 FFO (which is low for a REIT that really only has to hand out keys and keep the dust off the shelves!). Plus, management expects EXR’s FFO to surge 13% this year, going by the midpoint of its forecast range for the year.

7 Stocks That Love a Crash (and Are Set to Jump 15%+ Yearly in any Market)

Let’s be honest: investing hasn’t been much fun lately. It seems like just when we think the market’s hit bottom and it’s safe to buy again … it takes another leg down.

But you and I know the answer is not going to cash. Doing so cuts off your dividend stream—and exposes your savings to the ravages of inflation.

This Stock-Pickers’ Market Is Perfect for Us

Instead, we need to hold fast to our dividends and, contrarians that we are, we’re going to buy more. But now more than ever, we need the right dividend payers. Sitting in an index fund and hoping for gains has been a recipe for steep losses in 2022, and that’ll be the case for the rest of the year, at least.

But this stock-pickers’ market is perfect for contrarians like us! And I’ve got 7 “Hidden Yield” stocks I’ve handpicked to hand you returns of 15%+ a year in all market weather!

I call them “Hidden Yield” stocks because they pay us in ways that go beyond the current yield—the headline figure most people look at when they evaluate a dividend. They’re all cheap now, and spring-loaded for their next leg higher.

Hidden Yield Stocks Are “Dividend Rubber Duckies”

As we saw with Carrier, judging a stock by its yield alone is a mistake because the current yield conceals other factors, like payout growth and share buybacks, which goose dividends (and share prices with them)!

Enter the 7 stocks I have for you right here. They rain cash on shareholders through high, safe and growing payouts and share buybacks, all of which support their stock prices in a pullback and give them an added boost when markets rise!

I call them “dividend rubber duckies” because their rising payouts mean you can’t keep them down (and when they do drop, it’s a marvelous buying opportunity).

They’re the perfect companies to own now, and I can’t wait to show them to you. Click here and I’ll give you full details on my 7 “Hidden Yield” stock picks, including their names, tickers, a complete breakdown of their dividends, my in-depth analysis of their operations and more.

Recent Comments