The stock market’s 2023 recovery begs the question: are we in for a reversal next year? And if so, what does that mean for our closed-end funds (CEFs)?

It’s a natural concern, but it’s important to remember that bull markets don’t die of old age. Plus, we aren’t in a bull market—the S&P 500 still hasn’t fully recovered from its drop over the last two years, let alone priced in the economic growth over that time.

Whether stocks will or won’t price in that growth in 2024 depends on three things we’re likely to hear a lot about next year. The first will be something that’s seemingly been everywhere for the last two years.

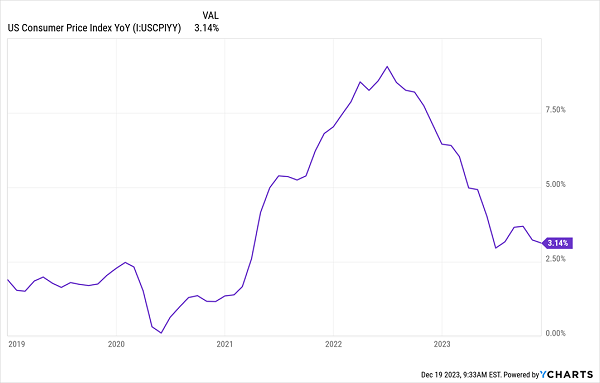

Inflation

This isn’t really the most important metric right now because inflation is now pretty much contained.

Inflation Bounces Around the Important 3% Level

While we aren’t below 3% sustainably, we keep pressing against it, which has led many to assume we will fall past the 3% floor in 2024.

I don’t disagree, but there’s a risk that we break through the 3% barrier too quickly. If that comes to pass, it could mean inflation becomes deflation, and a recession along with it. Similarly, if inflation doesn’t break below 3% or starts to go upwards, it’ll upend current assumptions about the second, and tightly related, issue that will be front and center in 2024.

Interest Rates

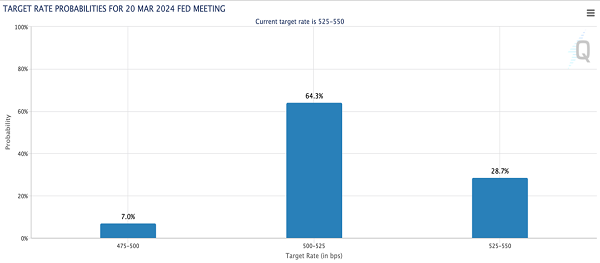

The Federal Reserve is likely done raising rates, and the futures market is expecting rates to be cut slightly in March.

Mild Expectations = Sleepy Markets

Source: CME Group

If the interest rate picture changes way too much in either direction, we’re likely to see more volatility. Higher rates are worrisome for the obvious reason we’ve dealt with these past two years: the cost of everything going up. But if rate cuts get aggressive in 2024, it would mean we’d be facing a recession, putting downward pressure on stocks, bonds and other assets.

Fortunately, we don’t need to go to the bond markets to get a hint of which direction things are likely to go on the rate front.

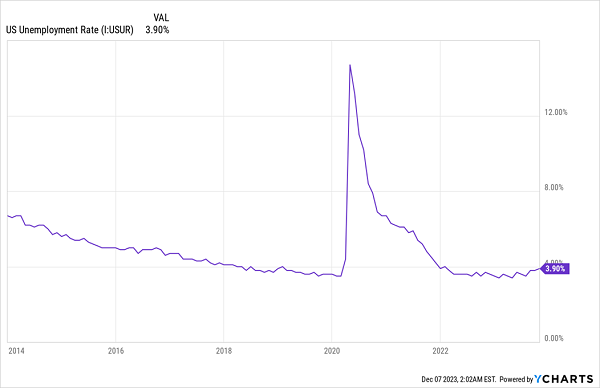

Employment

The real clue to how markets will perform in 2024 is going to lie with the job market, which will dictate whether the Fed is done with rate hikes and, if so, how aggressive it gets with rate cuts.

Remember the Fed balances interest rates and unemployment rates—that’s its defining function. If unemployment rises too much, it’ll have to fight that with aggressive rate cuts, meaning we can predict the Fed’s moves by seeing if employment is falling.

The Employment Question

At less than 4% unemployment, America’s labor market is doing well, producing higher real incomes for Americans, which let them spend more comfortably.

Thus, for now, while unemployment is bouncing around 4%, there’s good reason to think the markets expect the Fed to stay the course, inflation to stay around where it is, and stocks to see a healthy environment going into 2024.

In other words, as long as we don’t see too many overly fearful stories from the financial media, 2023’s strong recovery should turn into 2024’s bull market.

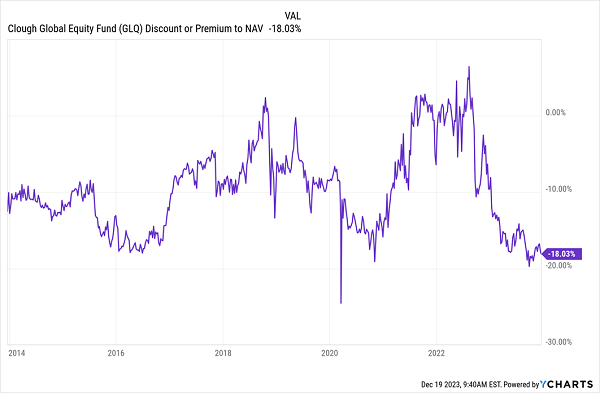

Discounts Bigger Than Ever: GLQ?

As investors look at these data points, they’ll likely be looking for any opportunity to buy assets that are still undervalued following the 2022 selloff.

Such a situation is a blessing for closed-end funds, whose 9.5% average discount to net asset value (NAV, or the value of a CEF’s underlying portfolio) is far larger than the 7% average discount they’ve had historically. That 2.5-percentage-point difference is huge because it’s spread out across nearly 500 funds, and some individual CEFs show how truly wide this “discount chasm” is.

Just as an example, consider the Clough Global Equity Fund (GLQ), which diversifies by buying the best firms in America and abroad—stocks like Microsoft (MSFT), Apple (AAPL), General Dynamics (GD) and Airbus SE dominate the portfolio. GLQ’s current 18% discount is much bigger than the 9.5% average discount it’s had over the last decade, not to mention the premium it had just two years ago.

GLQ’s Predictable Pricing

GLQ is a great swing trade to buy when its discount is way too big (like now) and sell when it approaches a premium. This strategy worked during the selloffs in early 2016 and early 2020, and now it’s available again, just in time for early 2024.

But GLQ’s likely discount-driven price jump over the next few months isn’t the only reason it’s nice to own—it also yields an eye-watering 12.5% today, and that payout comes our way monthly, to boot.

Grab These 5 Monthly Paying “Bargain-Bin Dividends”—Yielding 9.2%—NOW

GLQ is a great swing trade, sure, but for long-term holding, I recommend looking instead to the 5 monthly paying CEFs I’m urging investors to buy now.

In addition to dropping dividend cash into your account every 30 (or 31) days, these 5 reliable income plays yield an outsized 9.2% today.

Drop $100K into them now and you’ll pick up a cool $767 a month. $500K gets you $3,833 monthly.

And on it goes.

Here’s what really sets these 5 monthly payers apart: you don’t have to sacrifice gain potential to tap into their high payouts: all 5 are cheap—so much so that I’m calling for 20%+ price upside over the next 12 months!

Don’t miss your chance to buy these 5 high-yielding monthly payers while they’re still cheap. Click here and I’ll tell you more about them and give you the opportunity to download a FREE Special Report revealing their names and tickers.

Recent Comments