$600K can be enough money to retire on. Even as early as age 50!

The trick is to convert the pile of cash into cash flow that can pay the bills. I’m talking about $50,400 per year or more in dividend income on that nest egg, thanks to 8.4% yields.

These are passive payouts that show up every quarter or, better yet, every month. Meanwhile, we keep that $600K nest egg intact. Or, better yet, grind that principal higher steadily and safely.

Got more in your retirement account? Cool—more monthly dividend income for you!

We’ll talk specific stocks, funds and yields in a moment. First things first, let’s wipe the false promises of mainstream finance from our minds.

Step 1: Forget “Buy and Hope” Investing

Most half-million-dollar stashes are piled into “America’s ticker” SPY. The SPDR S&P 500 ETF (SPY) is the most popular symbol in the land. For many 401(K)’s, this is all the “go to” ticker.

Sad for two reasons. First, SPY yields just 1.5%. That’s $9,000 per year on $600K… poverty level stuff.

Second, SPY could easily drop 10% here. That would be no bueno for our retirement portfolio. We’d be left with $540K—less capital to generate income off of.

Step 2: Ditch 60/40, Too

The 60/40 portfolio has been exposed as senseless. Retirees were sold a bill of goods when promised that a 60% slice of stocks and 40% of bonds would somehow be a “safe mix” that would not drop together. That can work—but not always, and that “sometimes” can really hurt!

Inflation—plus an aggressive Federal Reserve plus a (thus far) persistently steady economy—has drop-kicked both equities and fixed income. The result is that bonds have not been the haven guaranteed by the 60/40 high priests.

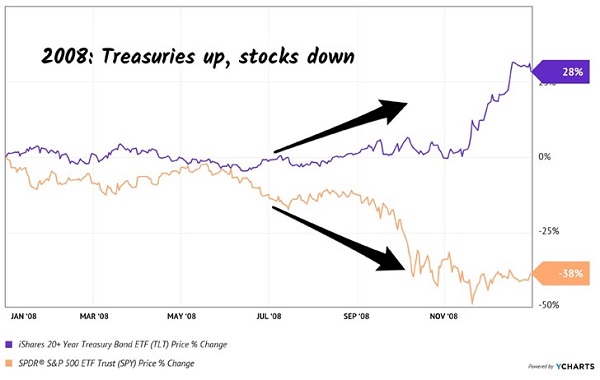

In a way, 2022 has been a worse dumpster fire than 2008. Granted almost everything crashed in the Financial Crisis, but US Treasuries rallied, and the iShares 20+ Year Treasury Bond ETF (TLT) delivered a 28% gain that year:

In 2008, Bonds Did Great

In 2022, however, TLT got tagged. Sure, it still paid its dividend. But even including payouts, the fund dropped 31%. Worse than the S&P 500. Ouch!

When stocks and bonds are dicey, where do we turn? To a better bet: a strategy to retire on dividends alone that leaves that beautiful pile of cash untouched.

Step 3: Create a “No Withdrawal” Portfolio

Tom Jacobs and I wrote the book on a dividend-powered retirement. In How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact, we outline our “no withdrawal” approach to retirement:

- Save a bunch of money. (“Check.”)

- Buy safe dividend stocks with big yields.

- Enjoy the income while keeping the original principal intact.

To make that million last, and our working and saving lives worthwhile, we really need 8% yields. And while we typically don’t see these stocks touted on Bloomberg or CNBC, they are around.

Of course, there are plenty of landmines in the high yield space. Some of these stocks are cheap for a reason. Which is why we need to be contrarian when looking for income.

We must identify why a yield is incorrectly allowed to be so high. (In other words, we need to figure out why the stock is priced so cheaply!)

The 19 dividend machines in my Contrarian Income Report portfolio average an 8.4% payout. This crew spins off $84,000 for every million dollars invested!

And you don’t have to be a millionaire to take advantage of this strategy. A $600K nest egg will create $50,400 in annual income. You get the idea.

The important thing is that these yields are safe, which creates stability for the stock (and fund) prices attached to them. We want our income, with our principal intact. It’s really the only way to retire comfortably, without having to stare at stock tickers all day, every day.

Now, many blue-chip yields are safe. They just need to hit the gym and bulk up a bit. Here’s how we take perfectly good yet modest dividends and make them into braggarts.

Step 4: Supersize Those Yields

Mastercard (MA) is a near-perfect dividend stock. Its payout is always climbing, up 128% over the last five years. (MA shareholders, you can thank every business that accepts Mastercard for your “pennies on every dollar” rake.)

Swipe, swipe, swipe. Remember cash? Me neither. Another 2020 casualty, with Mastercard making a few dimes or dollars on every plastic transaction.

The cashless tsunami has been in motion for years, but international growth prospects remain huge! Just a few years ago, 80%+ of transactions in Spain, Italy and even tech-savvy Japan were in cash. We expect more dividend hikes as cash morphs to plastic.

The only chink in MA’s armor? Everyone knows it is a dynamic dividend stock. So, it only yields 0.6%. Investors keep bidding it higher, knowing that the next dividend raise is just around the corner. The yield stays tiny.

So, the compounding of those hikes makes MA a great stock for our kids and grandkids. You and I, however, don’t have the time to wait for 0.6% to grow. And $3,600 on our $600K nest egg simply won’t get it done.

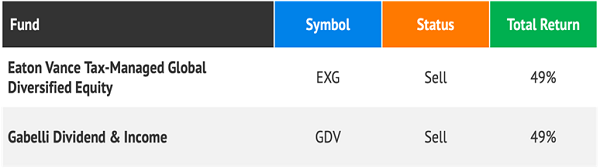

Let’s instead consider top-notch closed-end fund (CEF) Gabelli Dividend & Income Trust (GDV), managed by legendary value investor Mario Gabelli. Mastercard is Gabelli’s second-largest holding. But we income investors would prefer GDV because it boasts a sweet 6.4% dividend, paid monthly.

Not only that, but thanks to the selloff of ’22, we have a rare opportunity to buy Mario’s portfolio for just 84 cents on the dollar. Yup, GDV trades at a 16% discount to its net asset value, or NAV. It’s a great way to boost MA’s payout and snag a discount, too.

Where does this discount come from? CEFs have fixed pools of shares, so they can (and do) trade higher and lower than their NAVs, or “fair” values (the value of their holdings minus any debt). As contrarians we can step in when they are temporarily out-of-favor, like after a pullback when liquidity is low, and buy them at generous discounts.

GDV holds more blue-chip dividend payers alongside MA, such as Microsoft (MSFT) and JPMorgan (JPM). These stocks are already cheaper than a year ago, and with GDV, we have an opportunity to purchase them at a 16% discount.

These high-quality stocks wouldn’t normally qualify for our “retire on $600K” portfolio because everyone in the world knows they are nice long-term investments. Even though these companies consistently raise their dividends, investor demand for the stocks keeps their prices high and current yields low. They never meet our current yield requirement.

GDV does. Its monthly dividend adds up to a 6.4% annual yield.

But Brett, 6.4% ain’t 8.4%. Good point, so let me give you one more idea. Eaton Vance Tax-Managed Global Diversified Equity (EXG) is another CEF with a similar blue-chip dividend portfolio. But EXG generates even more income than GDV by selling covered calls on the shares it owns. More cash flow means a bigger dividend—and EXG pays an elite 8.4%!

So, do we buy and hold EXG and GDV forever, collecting their monthly dividends merrily along the way? Not quite.

In bull markets, these funds are great. But in bear markets, they’ll chew you up.

Step 5: Protect That Principal!

My CIR readers will fondly recall the 15 months we held GDV and EXG, collecting monthly dividends plus price gains that added up to 49% total returns.

What was happening in that period from October 2020 until February 2022? The Federal Reserve was printing money like crazy. Yes, it did stoke inflation, but we enjoyed a more-than-offsetting boost in asset prices.

Starting in 2022, we had the opposite situation. The stock market was topping, and we didn’t want to fight the Fed. We sold high.

So Long, Fed Fueled Plays

Might we buy these funds back someday? Of course. When the time is right.

For whatever reason, “market timing” is a taboo phrase among long-term investors. That’s a shame because it is quite important. By aligning our dividends with the market backdrop, we can protect our principal from bear markets like we saw this year.

Step 6: Start Here to Retire on $600K

“Tried and true” money advice—like the 60/40 portfolio and the 4% withdrawal rule—have been properly exposed as broken. Good riddance!

I’d love to tell you more about my solution, the 8% “No Withdrawal” Retirement Portfolio. Including my favorite stocks and funds to buy right now.

While we wait on bull market dividend darlings like EXG and GDV, we have flashing BUY signals in select corners of the bond market. Click here and I’ll share the details, include tickers and buy prices.

Recent Comments