“Mom, please make sure you secure your mask first before assisting the kiddos.”

We receive this reminder every flight from at least one flight attendant. Mom receives the reminder while your income strategist sits across the aisle (a mile away as far as his parenting partner is concerned) in an uneventful seat dubbed Daddy Island.

This, of course, runs counter to Mom’s (and even Dad’s) instinct. If your kid is in trouble, your first, second and third reaction is to help your child first. The airline’s point is that we can best help our children by first securing our own oxygen.

We discuss dividends here every Wednesday. For the second week in a row, our portfolio problems are infinitesimal compared with the suffering that is happening in Eastern Europe.

This said, we can help others if we first help ourselves. And it is possible for us to keep our dividends flowing in an ethical manner.

There are many gray areas in this world. But, in my opinion, funding Russia’s government in the days after its disgraceful attack on Ukraine is not one of them.

In my Contrarian Income Report service, we sold a bond fund that held Russian sovereign debt last Friday. We booked a loss on Western Asset Emerging Markets Debt Fund (EMD), which is never fun. But it was the right thing to do from an ethical and future return standpoint.

We can buy other bond funds that pay big dividends. Or consider energy dividend stocks that seemingly rise every day as crude oil supplies are pressured.

The move in oil, and our sale of EMD, has prompted thoughtful questions from readers asking if we should also consider selling our energy dividends. Whether they are contributing to unsavory regimes or to climate change, should we boot them too?

This is a trickier question. To answer, consider that in fulfilling my role as your income strategist, I wear three different “hats.” It can be a balancing act, especially if the hats conflict.

For example, I often poke fun at the Federal Reserve. My joking is not because the folks at the Fed are incompetent. On the contrary, these are brilliant economists. But they are constantly pulled in different directions due to the Fed’s “triple mandate”:

- Maximum employment.

- Stable prices.

- Moderate long-term interest rates.

Goal number one—jobs for all—conflicts with numbers two and three, which concern price stability. The result of this split-attention lately has been short-sighted decision making (let’s print a lot of money to encourage employment). This created the hottest inflation we’ve seen in 40 years.

My triple dividend mandate contains goals that are better aligned with each other. It is possible for me to write and recommend stocks with a broader mission to:

- Educate you about income investing, so that you can make your own smart decisions.

- Identify high, safe dividends for your consideration (or, in the case of Hidden Yields, fast-growing dividends).

- Find stock prices that will be stable or, better yet, trend higher (with HY, looking for faster price growth).

When my duties conflict, I prioritize them in this order. I’d rather teach you to do something than tell you. Then we look for safe dividends. And finally, a price kicker when available.

Successful income investing is simple, but it isn’t necessarily easy. We individual investors compete with savvy Wall Street firms and pension funds. Being contrarian and buying dividend payers when they are “out of favor” is our secret sauce.

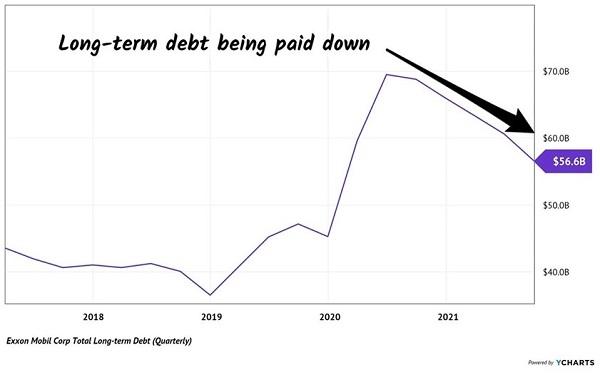

So, what do we do when Exxon Mobil (XOM) is trading impossibly low in April 2021? It feels like 11 years ago, but really it was just 11 months ago that XOM yielded 6.1% with 61% price upside.

My research told me crude oil prices were heading higher and that XOM would directly benefit. The stock was dirt cheap, and management was paying down debt—a sign that the firm had turned the corner. As your dividend guy, I had to share this with you:

How We Knew XOM’s Dividend Was Secure

XOM hit my multi-year price target in less than a calendar year. I didn’t think we’d see 60% gains this quickly, but here we are.

Will green alternatives make XOM’s business model obsolete someday? Of course. But not today.

Could we have bought the Invesco Solar ETF (TAN) instead? Sure! — if we wanted to lose 25% over the same timeframe. Plus, we wouldn’t have received any dividends.

TAN is a feel-good purchase. But the unfortunate reality of life is that cheery buys rarely make money. XOM was the profitable play to make.

To XOM’s credit, they did say last week that they will be winding down their Russian operations (with no new investment to come). XOM did not mince words in its statement, either:

ExxonMobil supports the people of Ukraine as they seek to defend their freedom and determine their own future as a nation. We deplore Russia’s military action that violates the territorial integrity of Ukraine and endangers its people.

XOM scores a point for good geopolitical behavior. This stock is a Hold here, however, as shares trade above my $85 price target. Our yield-on-cost remains 6%+ and we’ll let this winner keep running because, let’s face it, the West needs its oil this year.

Coca Cola (KO), on the other hand, is rightfully under pressure for completely ignoring the invasion. #BoycottCocaCola continues to trend online as the sugar-water maker continues to sell its product in Russia.

KO is not a stock we were interested in, because its dividend was growing too slow—“molasses moving uphill,” I wrote. That and its out-of-date management team made the investing decision easy. We had no interest in KO then, and even less now.

As I mentioned to some of you, I’m working on compiling a list of charities that benefit people in the Ukraine now. Our extra dividend dollars (and XOM profits) can go a long way. I plan to share this list with you soon and also donate myself.

(I’d probably have this promised list ready by now were it not for these manic markets. Alas, my priorities are to protect your retirement portfolio, identify a short-term low when we have one, and keep us away from that insensitive has-been KO—in that order.)

Update: As we were going to print, KO announced it was suspending its business in Russia. Perhaps an advanced copy of this article was leaked and read in Atlanta. We applaud the move, but still won’t buy the stock (its yield remains too low for such a slow dividend grower).

Finally, let’s circle back to those “better bond funds” that I mentioned earlier. They all pay monthly dividends that add up to 7% yields per year, or better. Which means their payouts will fully fund a retirement for around $500K.

Recent Comments