It was a simpler time years ago in America when my grandfather shared some nutritional advice with me:

“So, you’ve got the tomato sauce. Tomatoes. They’re good for ya,” as he put out his thumb to indicate the count was now one.

“And the cheese,” he continued. “Dairy. That’s good, too.”

Two fingers on grandpa’s right hand reflected the updated count.

“Plus the bread. That’s another group.”

Three points for pizza being good for you. My 12-year-old self was thrilled! I informed my parents about the good news on our car ride home from grandma and grandpa’s.

“You are not having pizza for every meal,” they quickly dismissed my nutritional news. “He doesn’t know what he’s talking about…”

Grandpa actually did know what he was talking about. He was simply reading off a past playbook from the USDA’s history. In 1943, when he was in Asia serving this country in World War II, the USDA introduced the “Basic 7” food groups to help Americans balance their nutrition during wartime rationing:

In 1956, the USDA consolidated the list to the “4 food groups” that many of us grew up with:

- Milk,

- Meat,

- Fruit and vegetables, and

- Bread and cereals.

Ironically, the initial edition with seven groups carried more nutritional diversity and is closer to the guidelines accepted today. The “dumbed down” version was introduced in 1956 and taught to your income strategist decades later. It more closely supports pizza as a daily staple.

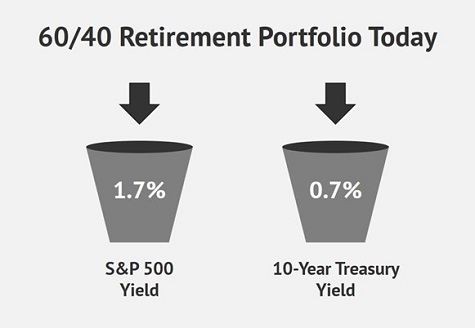

The “60/40 retirement portfolio” is the financial world’s parody on having pizza for every meal. The theory goes that you should:

- Put 60% of your nest egg in stocks,

- The other 40% in bonds, and

- Toggle the level up or down depending on your age.

This is where the tale really deviates from common sense. The “advice” says that we subtract our age from 110 (or 100—there are different variations) to determine how much to allocate to equities, with the rest going to fixed income. So a 30-year-old, with decades left to work, would calculate 110 minus 30 equals 80, which means he or she would put 80% in stocks and 20% in bonds.

Why would a 30-something not be 100% in stocks?

Let’s fast-forward to a 60-year-old who is hoping to retire. Is a 50/50 split between stocks and bonds really appropriate, or too risky? It depends where that stock allocation is going. (And heck, same with the bonds. Are we talking junk issuances, or US Treasuries?)

A vanilla version of 60/40 has another problem, today. It’s like comparing a fresh slice from grandpa’s favorite Italian pizzeria with a frozen alternative that we “nuke” in the microwave for two minutes and then choke down.

It doesn’t really matter how we mix these basic buckets. The net yield is not good:

A 60/40 mix gives us a 1.3% blended yield. This equates to a whopping $13,000 in annual dividend income on a million-dollar portfolio. Yuck.

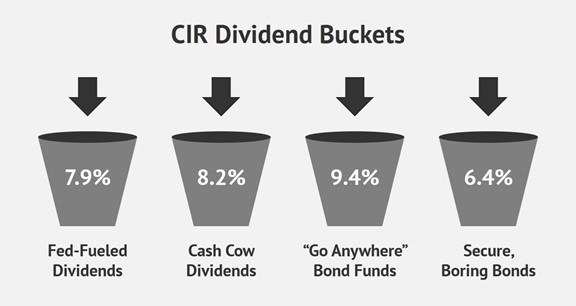

Fortunately, we original thinkers are not confined to this hopeless financial advice! On Friday, I introduced four dividend buckets to my Contrarian Income Report subscribers that we can actually use to retire on.

I leave the exact “bucket allocation” up to each individual because you are the architect of your own portfolio. These are dividend tools for you to use: upgrades from “Stone Age” investing advice to produce actual, meaningful income:

The Fed-Fueled Dividend bucket contains stock funds and individual stocks that are likely to benefit from the Federal Reserve’s continued money-printing. It pays 7.9%, and it has serious near-term upside thanks to the upcoming election (because the Fed wants to accommodate both political parties.)

Next we have a Cash Cow Dividend bucket that features multi-year stock holdings. These are shares that are currently out-of-favor but likely to rally over time as the world returns to our pre-2020 normal. While we wait, we collect an 8.2% yield.

On the bond side of the equation, our “Go Anywhere” Bond Fund bucket features excellent fixed income managers that have the OK to bank yields overseas. These are also multi-year positions which are likely to benefit from a weak dollar. Today they pay a fat 9.4%.

Finally, our most pedestrian bucket is Secure, Boring Bonds such as municipals and preferred shares. It pays “just” 6.4% and may make the most sense for investors closest to, or already in, retirements. These are positions you can buy and sock away forever.

Looking for big dividends likely to rally between now and Inauguration Day? Check out the #1 income investment I’m urging everyone to buy right now.

Recent Comments