If you’re like pretty well everyone else, you’re closely watching Gilead Sciences (GILD), creator of remdesivir, a drug that, last week, showed progress in treating the coronavirus in a US government study.

But does that make Gilead a good stock to buy now, particularly if you’re focused on income? Let’s take a look.

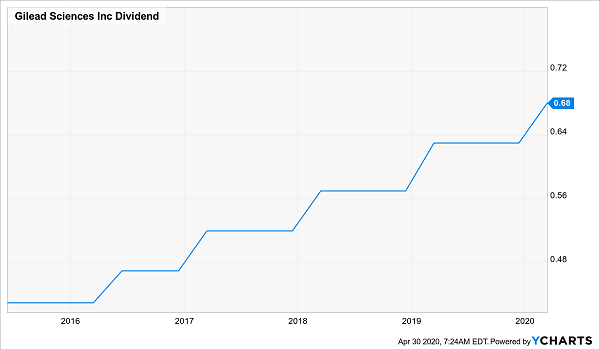

First up, unlike many other stocks these days, Gilead boasts a safe payout, with the dividend accounting for just 38% of free cash flow in the last 12 months. And the company has increased its dividend every year since initiating it in 2015:

A Reliable Dividend

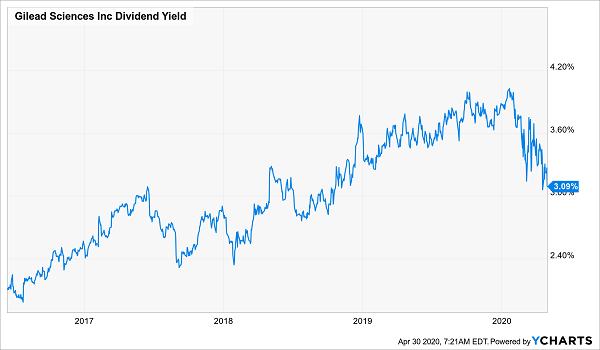

It’s on the current-yield front where the dividend story starts to fray. I’ll say right now that Gilead has never been in league with my favorite investments—closed-end funds (CEFs) paying 7% or more. But buying it in late March would have gotten you a respectable 4% yield, the highest in the company’s history.

Gilead’s Dividend Peak Arrives—and Departs

But buying today, just over a month later, gets you a much smaller 3.1% yield. That, of course, is because the current yield falls as share prices rise, and Gilead’s stock has been on a remdesivir-fueled tear:

Coronavirus Treatment Progress Looks Priced In

With Gilead shares up over 30% year to date and near their 52-week high, optimism for the drug is already priced into the stock. And bear in mind, too, that an earlier Chinese study showed no improvement among patients treated with remdesivir versus those given a placebo (though that trial was much smaller than last week’s study, and patients were given the drug up to 12 days after showing symptoms, possibly too late for it to be effective).

As I said, the science is still out on this one, but the stock’s run means that any more negative news on remdesivir could send it plunging.

“Farm Out” Your Pharma Investments to the Pros

I mention Gilead not because it’s the stock of the moment, but because it’s a good segue into my favorite way to invest in pharma, a sector that should have some representation in your portfolio, for reasons that go beyond our current crisis. With the aging population, these companies’ treatments are going to be in high demand in the future.

But, of course, we’re not medical experts here at Contrarian Outlook, which is why I prefer to “hire” a team of pros to do my pharma stock-picking for me.

That would be the team at Tekla Capital Management. The Boston-based firm’s CEO, Dr. Daniel R. Omstead, is a Columbia Ph.D. in chemical engineering and applied chemistry who works with a group of Ivy League–trained biopharma experts to dig into which companies are producing drugs that work, and which are not. (I’m not affiliated with Tekla, nor have I received any financial compensation from them; I write this as an admirer of their work alone.)

As a result of this expertise, Tekla has managed funds that have crushed the pharma benchmark iShares NASDAQ Biotechnology Index Fund (IBB) for years. And right now, two of Tekla’s funds are worth considering: the Tekla World Healthcare Fund (THW) and the Tekla Healthcare Opportunities Fund (THQ).

Both CEFs pay huge dividends (7.4% for THQ and over 10% for THW) while trading at discounts to their portfolios’ market value (6.5% for THQ and 7.7% for THW). Those discounts alone make them attractive, as Tekla’s funds often trade at premiums due to management’s strong past performance.

You could also consider these two funds a kind of second chance to buy Gilead—both hold the stock, and their discounts mean you can effectively buy Gilead at 6.5% or 7.7% off.

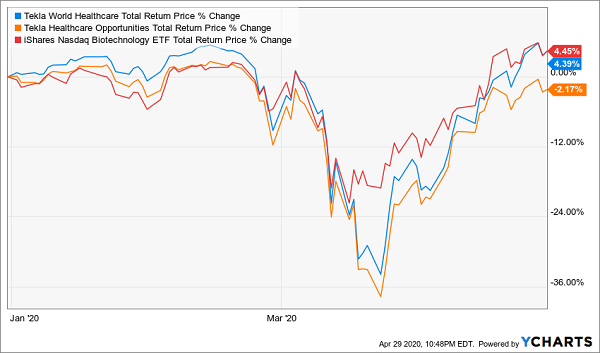

And here’s another signal that now may be the time to buy in: since their inception, both funds have been beating IBB, yet they’ve trailed the index fund year to date, though not by much.

Tekla Picks (Temporarily) Lag the Benchmark

The reason? Fear. CEF investors are very conservative by nature, so it’s unsurprising that many are shying away from THQ and THW during a panic—even if, ironically, these funds’ holdings are now more important to the economy than any other industry in the world.

And with high-powered scientific expertise helping these funds choose winners and dodge losers—as they’ve been doing for years—they’re worth a look. While you wait for them to regain their lead over IBB (and rise further), you’ll be collecting their attractive 7.4%+ dividends, paid monthly, no less.

The bottom line? Whether you’re relying on your portfolio for income or not, having medical pros steer your pharma holdings is a good way to profit from the sector’s growth as we move through the current crisis and into the coming recovery.

Your “Second Chance” to Buy This Rebound (With 8.4% Dividends!)

CEFs’ appeal isn’t just limited to pharma, of course. As I write this, there are some 500 CEFs in all, and they yield around 7%, on average!

They come from just about any corner of the market you can think of: there are CEFs that own bonds, S&P 500 stocks, tech stocks and even preferred shares and REITs.

Best of all, many of these proven income plays are cheap now. So if there’s a sector or investment you’ve wanted to get into but missed out on in this rally, these funds are a godsend—they give you a way to buy in at a discount, while giving you most of your return in safe dividend cash!

Consider my 4 favorite CEFs now. They pay a reliable 8.4% average dividend and form a standalone portfolio in their own right, giving you exposure to large cap US stocks, steady utilities and infrastructure names, bonds, the biggest tech plays (including Alphabet and Microsoft) and, yes, pharma stocks, too.

Except instead of settling for the lame 2% dividends most investors have to scrape by on, you’ll be collecting a life-changing 8.4% cash stream! And get this: these funds are so cheap now that I’m calling for 20%+ price upside in the next 12 months—bull market or bear.

I want to share the full story on this 4-fund “mini-portfolio” with you now. Click here and I’ll give you the complete tour, including names, tickers, dividend histories and everything else you need to know about these 4 high-yielding funds.

Recent Comments