Still spinning from Tax Day?

You’re not alone: plenty of folks who bagged wins last year are feeling shell-shocked, now that Uncle Sam has walked off with his cut.

Let’s face it: it’s too late to recoup any of that cash. But you can still take steps to weaken Uncle Sam’s grip on from your income stream, before you find yourself in the same boat next year.

And there’s an easy way to do it—it actually comes, in a strange way, from the government itself!

“Keep 100% of Your Gains Forever”

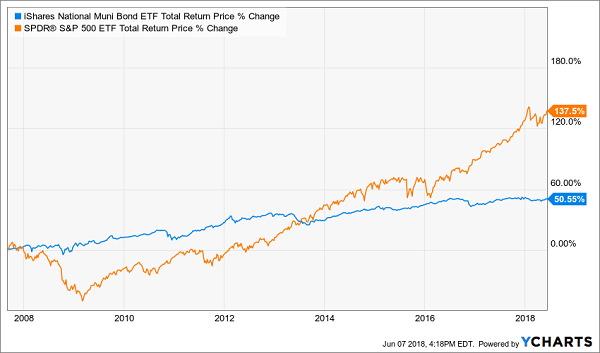

I’m talking about municipal bonds, or bonds issued by states, cities and counties to finance roads, bridges and just about any other project you can imagine.… Read more

Recent Comments