Dozens of companies are poised to raise their dividends over the next few months once the quarterly earnings season gets underway. Most of those are going to be token upgrades—just enough to pacify shareholders.

We’ll let Wall Street keep the tokens. We are “elephant hunting” big dividend raises.

I’m talking about companies with both the potential and the track record to hike their cash distributions by a minimum of 39%—though a lot more could be in store.

Why are hikes like these retirement makers? Simple—the “dividend magnet” effect.

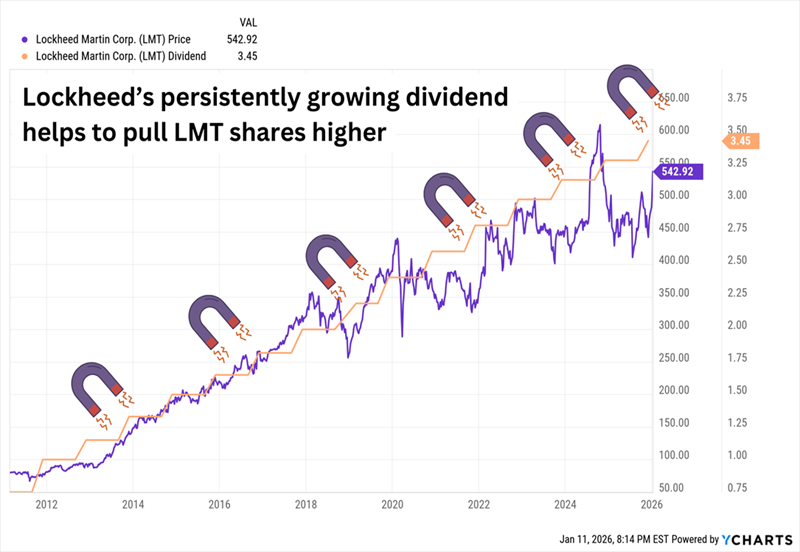

Lockheed Martin (LMT) is an example of this magnet in action. Look at how, for many years, LMT has traded almost in lockstep with its dividend—rarely getting too far behind or out in front of it.

The Magnet Is Strong in Companies With Persistent, Healthy Dividend Hikes

Meanwhile, Lockheed isn’t setting the world on fire with a 2.5% current headline yield—but anyone who has owned the stock for 15 years is sitting on a wild yield on cost of more than 18%!

Looking for the next Lockheed? Let’s discuss five companies that are due to deliver dividend hikes over the next couple of months. These firms generously rewarded shareholders with massive raises, including hikes of between 39%-100% as recently as last year!

Primerica (PRI)

Dividend Yield: 1.6%

2025 Increase: 39% (across multiple raises)

Projected Q1 Dividend Announcement: Early February

The first dividend-growth dynamo on this list is Primerica (PRI), which has more than doubled its payout in just the past four years.

Primerica deals in insurance, investments and other financial products. Specifically, Primerica offers term life insurance, mutual funds, annuities, business retirement plans, education savings plans, mortgages, identity theft protection plans, legal protection plans and other products targeting middle-income consumers in the U.S. and Canada.

Business has been steady. Primerica has delivered revenue growth every year for more than a decade. Bottom-line improvement hasn’t been as consistent, but the arrow has mostly been pointed upwards. The company’s full-year 2025 earnings per share (EPS) are expected to increase by low double digits, which is much quicker than usual. However, higher costs of living are pressuring Primerica’s customers, which is translating into more modest expectations for next year.

The question is whether Primerica’s next dividend hike—which likely would come in early February—will reflect the year it’s had or the year to come. The company’s 2025 hike was nearly 40% better than its 2024 starting dividend, and 15% better than its distribution by midyear (PRI raised twice in 2024).

Primerica’s Dividend Growth Has Been Particularly Aggressive Over the Past Few Years

Also worth noting: Primerica is throwing a lot of money at stock buybacks, and that should continue. In late 2025, the company announced a fresh $475 million buyback program for 2026.

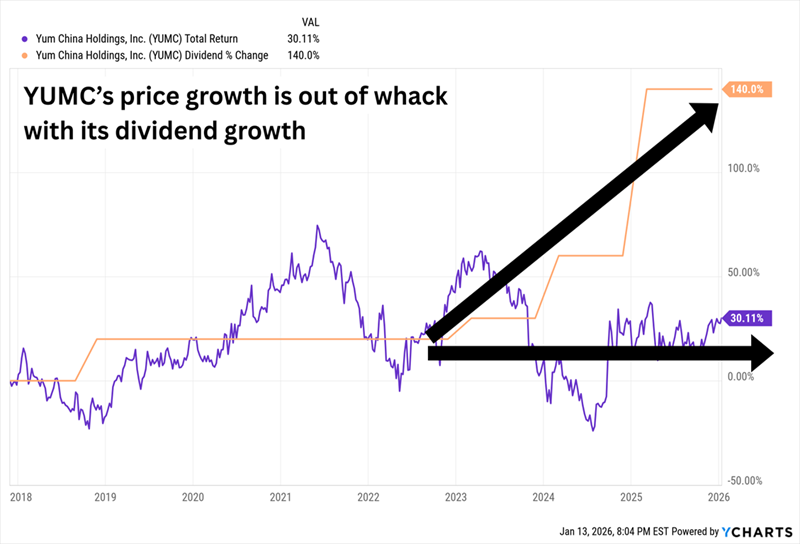

Yum China Holdings (YUMC)

Dividend Yield: 2.0%

2025 Increase: 50%

Projected Q1 Dividend Announcement: Early February

Shanghai-based Yum China Holdings (YUMC) is best known in the U.S. as the owner and operator of Yum Brands’ (YUM) keystone KFC, Pizza Hut and Taco Bell restaurants in China. However, it operates other chains in the world’s second-largest economy, including Lavazza coffee, Little Sheep hot pot, and Huang Ji Huang casual Chinese.

YUMC has driven fairly consistent top-line growth since its 2016 split from Yum Brands, and the restaurateur expects fairly aggressive expansion going forward. The company was on track to open 1,600 to 1,800 net new stores in 2025, and it’s modeling double-digit annual earnings per share growth through 2028. Profit growth hasn’t been nearly as consistent, however, and the stock has reflected that—shares are virtually flat since the beginning of 2020.

It would seem Yum China is throwing cash at the problem, pledging to return $3 billion to shareholders between 2025 to 2026. The company took seven years to raise its dividend from 10 cents per share (2017) to 16 cents per share 2024). But in 2025, it turbocharged the payday, announcing a 50% hike to 24 cents per share.

Nothing Else Has Worked—Maybe the Dividend Magnet Will

YUMC’s current dividend represents about 33% of 2026 profit estimates, so it certainly has room for another big bump. The question will be whether it wants to commit even more capital when it’s clearly still in the midst of aggressive expansion. We’ll keep watch for its next dividend announcement, which should come in early February.

Also, YUMC isn’t the only Chinese stock to monitor this quarter. JD.com (JD) and Tencent Music Entertainment Group (TME) both raised their payouts by more than 30% in March of last year.

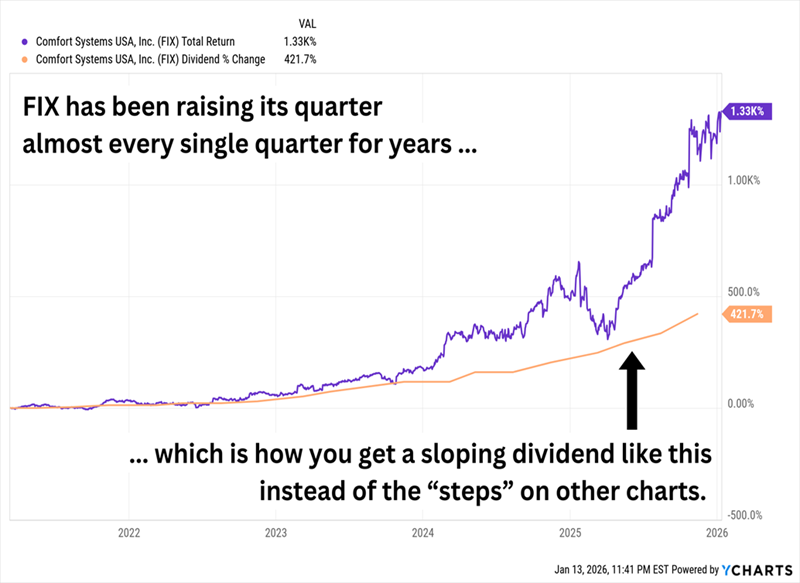

Comfort Systems (FIX)

Dividend Yield: 0.2%

2025 Increase: 60% (across multiple raises)

Projected Q1 Dividend Announcement: Late February

Anyone who has ever worked or visited a commercial building (so, most of us) has likely benefited from Comfort Systems USA (FIX), which keeps buildings usable and comfortable. The company installs, renovates, maintains, repairs and replaces heating, ventilation, air conditioning, plumbing, electrical, monitoring, fire protection and other systems.

The company provides its services for buildings that serve a wide variety of sectors. Its two largest customer types are manufacturing and technology—and the latter is considered to be a significant driver of growth. One area of opportunity is artificial intelligence (AI); as technology companies continue to build the data centers necessary to power AI, they’ll need the types of HVAC and electrical solutions Comfort Systems provides and installs.

I pointed this out in mid-2024, and I’m not surprised to see FIX on this list again.

Comfort Systems’ dividend has simply exploded in recent years, up some 471% since 2020. The yield is modest but consider this: The stock yielded less than 1% at the start of 2021. But in just five years, anyone who bought them is sitting on more than 4x that, at a yield north of 4%! That’s because the company’s fortunes are rising fast.

And Management Clearly Sees the Need to Share the Wealth Appropriately

The good times continue to roll. In its most recent quarter, organic revenues were up 33%, EPS doubled, and operating cash flow jumped 83%. That makes another dividend hike appear highly probable—and the likely timing based on past precedent would be sometime in late February.

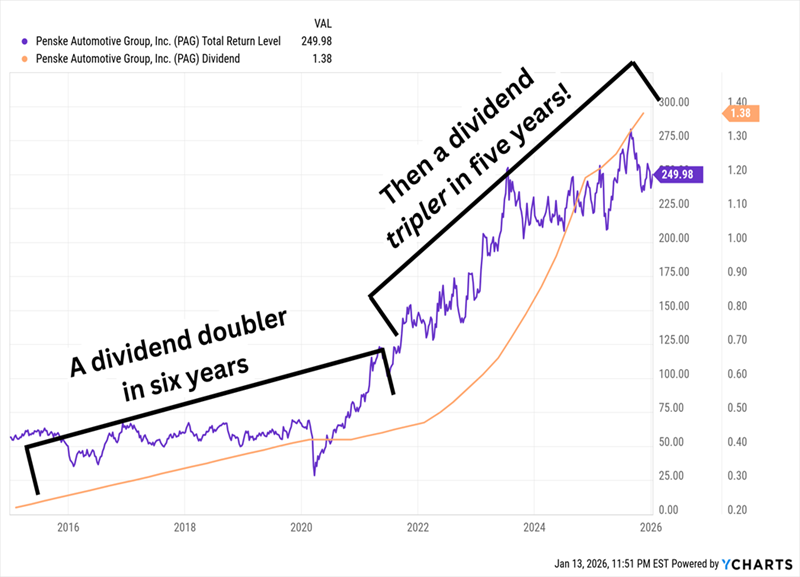

Penske Automotive Group (PAG)

Dividend Yield: 3.4%

2025 Increase: 40.2% (across multiple raises)

Projected Q1 Dividend Announcement: Late January/Early February

Speaking of quarterly raisers, Penske Automotive Group (PAG) also gets the itch every three months or so.

Penske is an international automobile retailer that operates dealerships not just in the U.S., but also the U.K., Germany, Italy, Canada, and Japan. And these dealerships cover just about every international auto brand under the sun.

But it’s not just passenger vehicles—Penske also has a commercial-truck retail business across North America, and it distributes and retails commercial vehicles, power systems, engines, and more across Australia and New Zealand. In addition to all that, it owns just shy of 29% of Penske Transportation Solutions, a North American transportation services, logistics, and supply-chain management services provider.

I’ve highlighted Penske in a previous look at dividend growers, but PAG is so prolific it bears shining a spotlight on it again. Penske has an almost uninterrupted run of quarterly dividend hikes going back more than a decade—it did suspend its payout for two quarters in 2020, which we don’t want to ignore—but it resumed distributions that same year, then just went right back to raising and raising and raising.

PAG Delivers 430% Dividend Growth Over the Past Decade

This has made Penske’s quarterly dividend announcements must-see events for dividend growth investors, and the next one is likely to come in late January or early February.

However, PAG’s next few quarters are worth watching to see what its dividend announcements say about management’s confidence. Net income has actually been on the downswing over the past couple years; Wall Street sees another slip for full-year 2025, and flat profits in 2026.

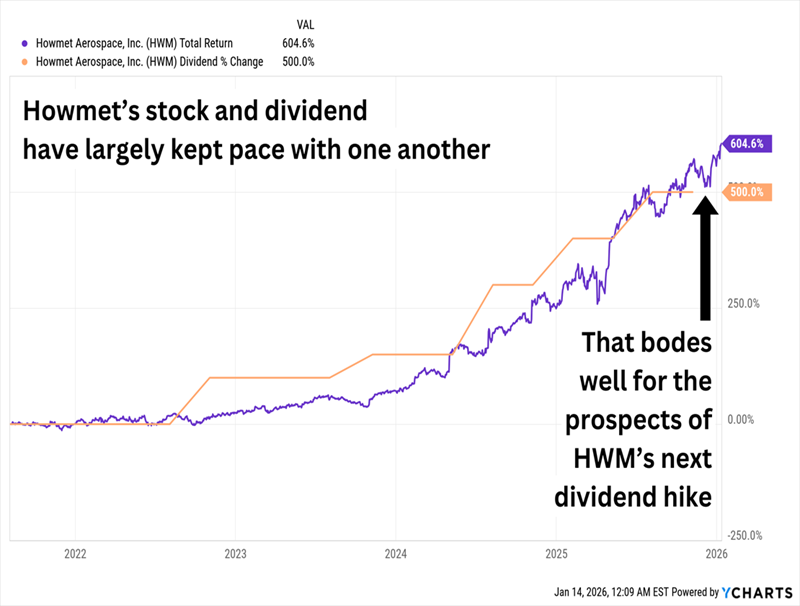

Howmet Aerospace (HWM)

Dividend Yield: 0.2%

2025 Increase: 100% (across multiple raises)

Projected Q1 Dividend Announcement: Late January

Howmet Aerospace (HWM), the result of a split in Arconic back in April 2020, makes advanced engineered products for the aerospace and transportation industries worldwide. Its products include jet engine components, aerospace fasteners, airframe structures, and forged aluminum wheels for commercial trucks. Essentially, Howmet makes things faster, cleaner, stronger, and/or more fuel-efficient.

Like with Comfort Systems, Howmet’s current yield is microscopic, but it’s not for lack of effort. The company’s dividend has grown by 6x in just five years. The 10 cents it paid to start 2025 was double what it paid to start 2024, and it tacked on another 2 cents midyear.

HWM’s Dividend Is Going to the Moon

Howmet’s latest potential growth driver? In late December, it announced a $1.8 billion acquisition of Consolidated Aerospace Manufacturing—a maker of precision fasteners, fluid fittings, and other engineered products for aerospace and defense—from Stanley Black & Decker (SWK). Its revenue projections imply 20% revenue growth for the division in 2026.

The company is expected to grow its bottom line by 37% for full-year 2025, then slow to a still-robust 20% EPS expansion in 2026. It’s difficult to tell how much of that will flow through in the form of higher dividends, but the track record is encouraging. We should find out one way or the other in late January.

5 More Dividends That Could Double Every 5 Years

Monitoring and identifying the best dividend raisers is the key to our wealth-building strategy.

We buy boring, underappreciated stocks that raise their dividends, then wait for those dividends to inevitably pull shares higher over time. In fact, this simple relationship between dividends and price gains holds the key to 15%+ returns per year from conservative investments.

I call it the “Recession-Resistant Retirement Plan.”

It’s not flashy. It doesn’t give CNBC’s talking heads anything to chat about. But it works.

Right now, I’m laser focused that are poised to soar while dishing out solid, rising income.

These stocks have the potential to deliver 15%+ annualized returns over the long run—that’s enough to double your investment every 5 years.

Now’s the time to strike.

Recent Comments