Almost One-Third of NYC Restaurants Missed June Rent, Survey Finds

Scan the business headlines (and let’s be honest, who actually reads anymore?) and we’ll see ominous headlines like this. Makes us wonder who would want to be a landlord in this economy?

It’s not just NYC. Here in California, most restaurants are, once again, not allowed to offer indoor dining. Epidemiology arguments aside, our beat here is money, and how many restaurants are supposed to make money right now I do not know.

If they’re not making money, who knows if they’re paying the rent. Taking that a step further, we might also question who wants to own any real estate investment trusts (REITs)? During “normal” times, these are sweet income vehicles. We talk about them often in this space because REIT stocks are our kinds of stocks. They collect cash and dish 90% of their profits to us in the form of dividends.

(REITs are required to pay out most of their stated income to shareholders as payouts, to keep their tax-privileged status. It’s a requirement we are happy to collect on.)

The trick is, today, that REITs must collect on their end before they can pay us. In other words, the rent has to get paid for our dividend to be safe.

This is why, as the initial lockdowns were handed down in March, REIT stocks were dumped en masse. Investors realized that April 1 rent payments were going to be a disaster.

However, after a few months of pandemic landlording in the books, you’ll be surprised to see who is actually paying their rents.

Before I share the stats, let me ask you: Would you buy an apartment REIT right now?

I didn’t think so. Which is why some of the best apartment REITs are looking cheap.

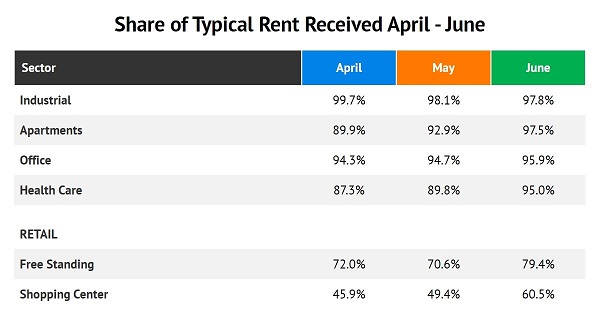

Check this out—it’s the rent collected by REIT sector for April, May and June. All of our newly completed “shutdown” and “re-opening” and “just kidding, we’re closing again” months. Would you believe that apartment landlords collected 97.5% of their typical rents in June?

(Source: Nareit)

Apartment tenants are paying more of their bills than healthcare firms. Who’d have guessed? (Not the “first-level” thinking crowd!)

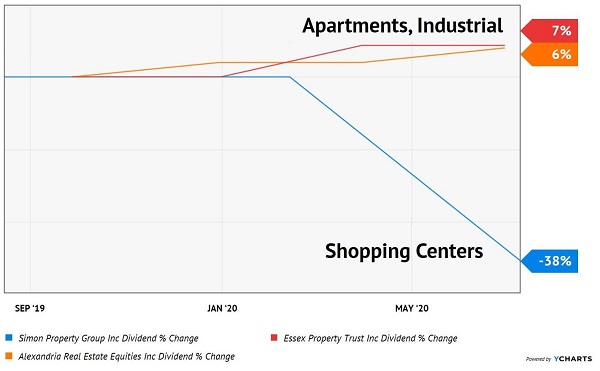

As rents received go, so go the accompanying REIT dividends. Cherry picking a blue chip from the apartment, industrial and shopping center contingent reveals that we’re looking at 7%, 6% and negative 38% dividend growth over the past 12 months:

3 REITs, 2 Diverging Dividend Paths

Essex Property Trust (ESS) is the apartment REIT above. It’s doubled its dividend (+101.2%) over the past decade. Essex rents to the high-earning tech brainpower that makes Google, Amazon and Facebook run. Its 240+ apartment complex footprint is focused on Northern California (42% of income), Southern California (41%) and Seattle (17%).

Essex yields 3.4% today, which is on the high end of its historical range. One concern I have with these apartment markets, though, is the smooth transition to working-from-home. What happens to rental prices when the tech sector officially admits that you can be just as efficient working from home (in another city, state or even country?)

There are already reports that San Francisco rents are falling fast (by their standards). I left SF myself in 2007, improved my quality of life and cut my cost of living to boot. Cheaper cities, states and suburbs should benefit if a distributed tech workforce is here to stay.

(How about suburban apartment REITs in counties with low case counts yet cheap share prices? Now we’re taking the elevator up another floor for some third-level thinking. I’ll keep you posted on this research.)

Meanwhile let’s talk industrial REITs. Our example here is Alexandria Real Estate Equities (ARE), another “undercover” tech play which owns offices and labs in “innovation clusters” (research-heavy areas).

Heading into the pandemic, Alexandria boasted a sky-high 96.8% occupancy rate. Its types of tenants—innovation-focused firms—often let their employees work from home. So, the idea of an office as a place someone can go to if they’d like is nothing new. (The only difference now is that employees will probably have to toss a mask on as they enter.) Alexandria’s tenants want the space available “just in case” someone wants to pop into the office.

As we keep an eye on ARE, let me also loop in our old friend and previous Contrarian Income Report holding, W.P. Carey (WPC). It’s back on my radar screen now that the stock’s yield is all the way up to 6.3%. Carey’s diversified book of industrial properties is continuing to cash flow for the firm. CIR veterans will fondly recall the 24% returns we made in our 12 short months holding WPC!

Our 24% Returns From WPC in Just 12 Months

While the industrial and apartment REIT bargain bins do contain some hidden gems, there is not enough hand sanitizer on the West Coast to tempt me into trying on any of the hopeless shopping center REITs. Simon Property Group (SPG) is the best in its business, and look what happened—a 38% payout cut with more pain likely.

We’ve been panning retail REITs for years now because the online shopping trend has simply not their friend. Lockdowns and limited foot traffic in 2020 has accelerated the e-commerce movement further. Sorry Simon, we say avoid.

In fact, we should avoid any and all dividends that are not 100% “recession-resistant.” Let’s be honest—our economic winter is beginning, and we’re rolling into the worst recession since the 1930s. This backdrop is going to be a disaster for many dividend investors, but it’s one that we can survive (and even thrive in) if we focus on second-level and third-level stock analysis like we did above.

With that in mind, I actually have five recession-resistant dividends paying up to 13% today that are great buys right now. Interested in my full research? Get my durable dividend dish including company names, tickers, and target prices right here.

Recent Comments