We’ve all loved watching our dividend payers soar since the August 5 crash. (To be honest, we might have liked a bit more time to shop the bargains!).

But that’s investing. And I do have two pieces of good news on that front:

- There are still some cheap—and growing—dividends on the table (we’ll name one below, as well as a “dividend dog” to dump right away if you own it).

- This latest market bounce is broad based, as opposed to most of the last couple years, when tech was running the show:

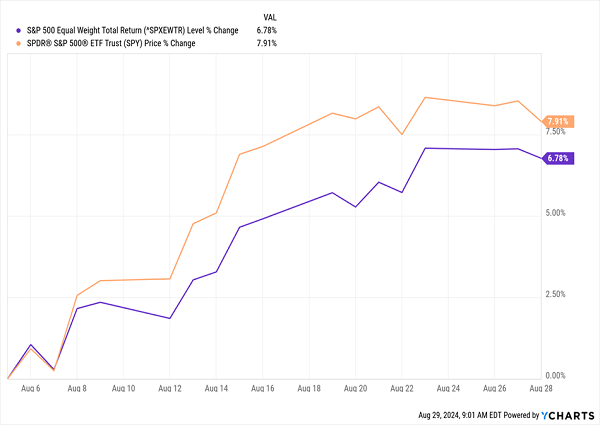

Good “Breadth” Bodes Well for More Gains

Here we can see the jump in the S&P 500 as a whole (in orange) versus its return on an equal-weight basis (in purple). Sure, there’s a bit of a gap, but safe to say this has been an across-the-board rise.

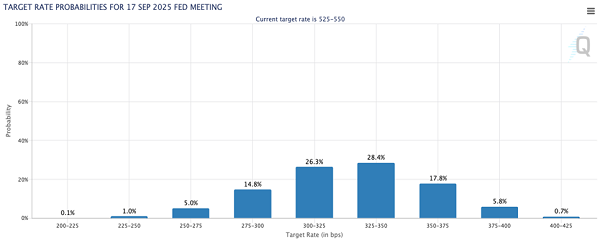

We can thank Jay Powell: At the Fed’s recent Jackson Hole retreat, he basically declared a September rate cut. Futures traders see as many as eight quarter-point cuts by this time next year:

Source: CME Group

That will give stocks a tailwind, but we won’t be able to simply buy anything and enjoy the next leg up. There’s still a lot of fear out there (and we have a contentious—to say the least—presidential election to get through, of course).

Quality will come first, second and third on most people’s lists as they shift from Treasuries and other guaranteed assets into stocks. So now is the time for us to sell weak holdings and shift into the remaining bargain-priced dividend stars out there.

Which brings me to the two tickers below. Both are tied to retail, but they couldn’t be more different: One is a department-store operator whose 10% payout is a warning sign. The other is a smart play on lower rates—with a dividend that’s more than doubled in the last five years.

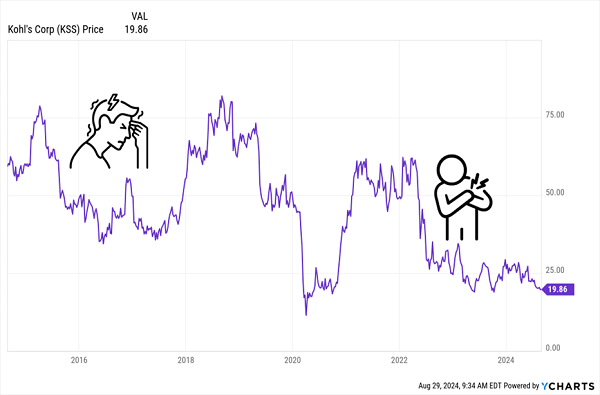

Sell This Struggling Retailer “on the Rip” …

If you hold department-store retailer Kohl’s, you have my sympathy. It’s the poster child for cardiac share-price action!

Kohl’s: Airsick Bag, Anyone?

If you’re hoping for yet another rebound, or are considering buying Kohl’s for its 10.1% dividend, do yourself a favor and step away. Because that 10.1% yield is a warning sign.

While the company did just report higher earnings (and a higher earnings forecast) in its latest quarter, cost cuts were the story here: Sales dipped 4.2% from a year ago and 5.1% on a same-store basis.

Reducing costs, of course, can only sustain profits for so long. Eventually sales have to rise, and many consumers are holding off, squeezed by higher costs.

To be sure, lower rates will help Kohl’s, but the company isn’t as well-placed as many of its competitors to capitalize. That’s especially true online, where Kohl’s ranks 21st among North American e-retailers, according to online-retail research firm Digital Commerce 360.

The company’s high payout ratio (it paid 80% of its earnings as dividends over the last 12 months) is also a worry, especially in the fickle retail sector.

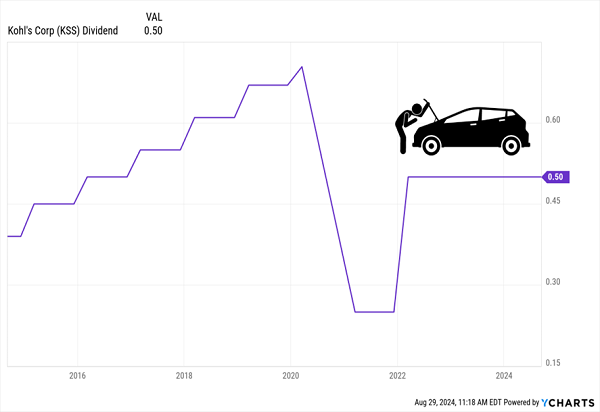

To be sure, management has made headway toward bringing the dividend back to where it was prior to its pandemic-era cut, with a raise announced in February 2022. But its high payout ratio and business challenges make further hikes unlikely—and raise the potential of another cut:

Kohl’s Dividend Stalls Out

Another warning sign: KSS shares fell on August 5 and haven’t really bounced back with the rest of the market. That sets the stage for another plunge the next time stocks take a header. It’s also a sign that investors are leaning into quality, as I mentioned earlier.

… And Buy This Payment Kingpin Instead

Speaking of quality, it’s hard to find a better business model than that of Visa (V). Swipe a card, “Big V” takes a percentage of the transaction. Simple!

That makes it a great play for us: Instead of trying to cherry-pick winners and avoid losers (I’m looking at you, Kohl’s) in the cutthroat retail game, we’ll simply buy the firm that owns the “payment pipelines,” thank you very much.

Recession worries are at the heart of our play here: They’re why Visa is only up about 5% this year, compared to the market’s 18% bounce.

But those fears are overblown: Consumer spending is holding up, unemployment is still low, and declining interest rates will put more money in consumers’ pockets. When a recession does inevitably hit, Visa’s well-placed to ride it out, as its network is used for essential and discretionary purchases alike.

The company also gets some insulation from the fact that it holds the largest slice of the payments market, with a greater-than 60% share as of 2022, according to Statista.

Meantime, Visa and main competitor, Mastercard (MA), aren’t banks—they just process payments. We can thank that particular difference for Visa’s “ironclad” balance sheet, with $20.6 billion in long-term debt, which is almost entirely cancelled out by its $16.6 billion in cash and short-term investments.

Visa is also leading the pack in the fast-growing e-payments space. Its new B2B Connect payment network, for example, is designed to facilitate cross-border transactions between businesses. It gives the buyer’s bank a way to pay the supplier’s bank directly, without the need for one (or more!) intermediary banks.

Cross-border transactions are a growing business for Visa, with volumes jumping 14% in its latest quarter from a year earlier. And with the direct connection, the service offers same-day payments. Cash is king in international transactions—the company that has the cash controls the deal. Visa’s speed of delivery helps reduce risk on both sides.

And don’t worry, Big V takes its usual cut of each payment. This is why it’s a cash cow: We’re talking 185% free cash flow (FCF) growth over the past decade alone.

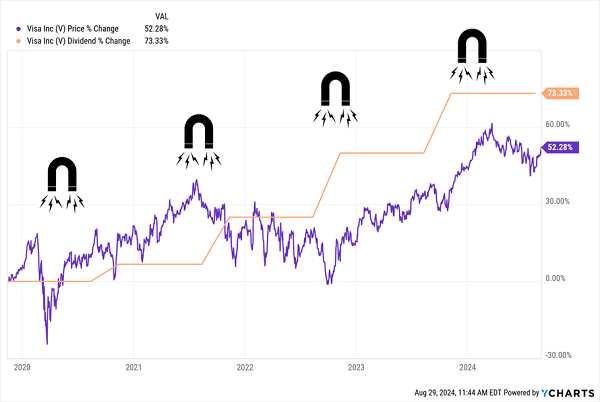

Visa’s “Dividend Magnet” also tells us it’s cheap today. Look at its share-price action below, which tightly clung to its dividend growth until the start of 2022, when it broke off. That points to further upside ahead.

A “Dividend Magnet” Getting Set to Power Up

Ignore the 0.8% current yield on this stock: As you can see, dividend growth—and its potential to ignite the share price—is where the party’s at. Visa is rarely as ignored as it is today. Let’s buy before its payout doubles again.

5 “Dividend Magnet” Buys to Turbocharge Your Payouts (and Net Worth)

Visa shows us the power of dividend investing done right: That is, zeroing in on dividend growth, not simply cherry-picking stocks with the highest yields.

Kohl’s is the classic example of the dangers of “chasing yield.” Its 10% yield is the result of a share price that’s crashed, wiping out any benefit you’d get from its dividend.

Visa, on the other hand, steadily drives its payout higher, building up the yield on your original investment—and taking the share price along for the ride! This is, by far, the safest way to build lasting wealth—and a “recession-proof” income stream, too.

I’ve got 5 more stocks with accelerating dividends I’d like to share with you now, with Dividend Magnets that are just as powerful as that of Visa.

The time to buy them is now. Click here to learn the secrets of the Dividend Magnet and download a free Special Report revealing these 5 stocks’ names and tickers.

Recent Comments