With stocks again on the upswing after the August 5 pullback, the appetite for risk is back!

Rising markets are terrific, of course. But they do bring dangers. One is that they might tempt some people to abandon sound long-term investing and take a stab at more speculative approaches, like day trading.

Before we go too far into whether you can actually make a reliable return from day trading, I’d say that to be a successful day trader, you should be aiming to beat the market … and a lot of ink has been spilled about how active managers—and I’d include individual investors here—can’t do that on the regular.

Well, that’s nonsense. Plenty of portfolio managers and individual investors do beat the market regularly. Consider closed-end funds (CEFs), for example, which yield 7%+ on average, with plenty sporting histories of beating their benchmarks.

That’s especially true when you look at funds focusing on assets outside of stocks: REITs, corporate bonds, municipal bonds, preferred stocks and such.

There’s no reason why you can’t do it, too. A good place to start is the field you know best. Let’s say you’re an HVAC engineer and you’ve spent your life studying and repairing these systems. Could that expertise help you identify strong HVAC firms better than a Harvard-educated investment banker could?

Of course. Which is why investment banks hire firms to help them gain the expertise of people skilled in one field. You, as a day trader, might be able to cut out the middleman—the banks collecting all that expertise—and beat the market.

Even so, the math says day trading is unlikely to go your way.

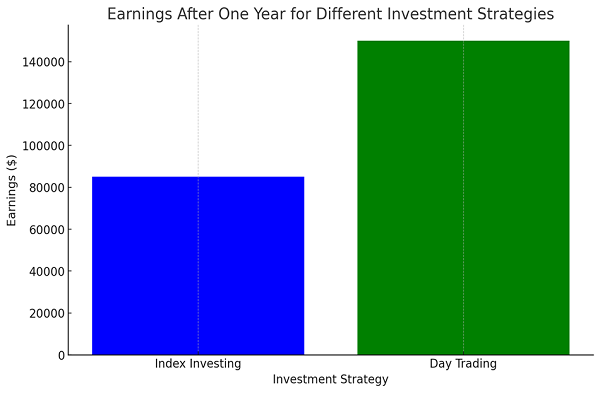

Let’s say you have a million-dollar account, and you invest in an index fund with an average annualized return of 8.5%—more or less the stock market’s long-term return, depending on the timeframe.

For our day-trading scenario, let’s be (very) generous and say a 15% average annualized return is on the table here.

Source: CEF Insider

Bearing these assumptions in mind, the difference in favor of day trading is $65,000—a lot of cash, I’ll admit.

However, let’s translate that into time. American stock markets are open six-and-a-half hours a day, five days a week, with few days off. That translates to 1,631.5 hours a year of work, meaning you’ve earned a bit less than $40 an hour.

If that’s more than you earn now and you’re 100% confident you won’t make a mistake you can’t recover from—great. But even under these circumstances, we need to be clear that we haven’t found financial independence here. We’ve just found a new small business as an asset manager, and it’s a full-time job.

Of course, any day trader will tell you that they don’t just work during market hours, so in reality that $40 per hour will be less. We can, of course, fix this by earning a bigger return: the day trader who is confident they will earn 150% annually, on average, would make $867 an hour for their labor on a million-dollar investment.

Impressive, I suppose, although there are people in finance who earn more doing things that are much less stressful. But clearly, no matter how good we are at it or how much money we can make, day trading is a job, and the risk is much greater when it’s with our own money.

Which is why we at my CEF Insider service continue to see buying quality CEFs, holding for the long term and collecting their high—and often monthly paid—dividends as a much better way to go.

The Passive-Income Alternative

With dividend yields averaging over 7%, CEFs are a great way to translate long-term capital gains from stocks and other assets into an income stream.

That 7% is actually an understatement: it’s dragged down by a lot of municipal-bond CEFs that yield less, but, since their income is tax-free for most Americans, tend to be the equivalent of around 8% for median US earners (and more for higher earners).

Equity CEFs, for their part, average an 8.1% yield over the long term, again indicating that CEFs have big income streams that, upon closer look, are actually even bigger.

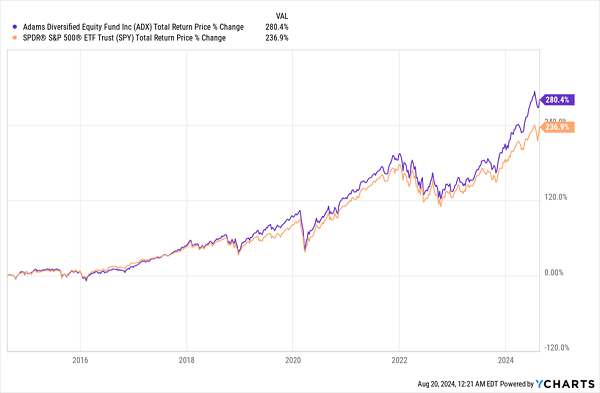

This is important because it means we can get the 8.5% annualized profits of the stock market almost entirely in the form of dividends, in the case of many funds. And some do better. Take, for example, the Adams Diversified Equity Fund (ADX), a CEF Insider holding that holds blue chips like Microsoft (MSFT), Apple (AAPL), JPMorgan Chase & Co. (JPM) and Visa (V) among its top-10 holdings.

The fund has earned a 280.4% total return over the last decade while exceeding the stock market’s return.

ADX Beats the Market

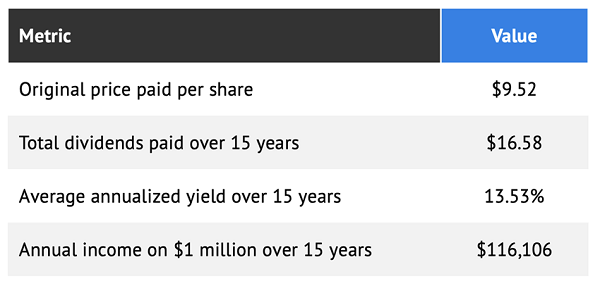

ADX has paid out $16.58 per share in dividends over 15 years, but it’s actually much older than that (there’s a longer history of big payouts here—more on that in a minute). Investors who bought then and have collected payouts since have earned a 13.53% dividend yield on their initial investment.

True, that’s $116,000, still less than our hypothetical day trader who could earn $150,000 on a million invested in our generous previous example. But it’s both more than the market’s average and it’s come in the form of dividend payments that investors had to spend exactly zero hours per year to earn.

Note, too, that ADX recently changed its dividend policy: Before the change, ADX paid most of its dividend in the form of a one-time, year-end special payout. Now ADX will pay no less than 2% of its net asset value (NAV, or the value of its underlying portfolio) per quarter, for an average 8% yield on NAV.

That shift expands the fund’s appeal beyond its core group of shareholders, in light of income investors’ preference for a more regular, consistent payout.

Finally, what we like the most is the lower risk involved here. One bad mistake with day trading can make a trader’s life savings evaporate; ADX has been a profitable company since 1854 and a profitable CEF since 1929. While hundreds of day traders are ruined every year, ADX has held fast through ups and downs over more than a century.

A Reliable 5-CEF Portfolio That Crushes Stocks, Yields 8.7%

ADX shows why we prefer CEFs to any other asset class or strategy (especially day trading!): They give us most of our return in dividend cash, thanks to their high yields.

We can reinvest that if we like, or go ahead and use it to pay our monthly bills.

Still, if you’re new to CEFs and are still a bit hesitant, I get it. It’s always hard to take the plunge on something new. Which is why I want to make it as easy as possible for you to try out CEFs yourself.

To that end, I’ve put together a “mini-portfolio” of 5 CEFs that kick out a reliable 8.7% payout. Here’s what your income stream could be if you bought now:

- $200,000 invested generates $17,400 a year ($1,450 a month)

- $500,000 invested generates $43,500 a year ($3,625 a month)

- $1 million invested delivers $87,000 a year ($7,250 a month)

And on it goes!

I can’t wait to share the details on this 5-fund portfolio with you. Click here and I’ll tell you more, including why CEFs are far off most investors’ radar, and give you the opportunity to download a FREE Special Report revealing the names and tickers of these 5 wonderful CEFs.

Recent Comments