Generally, recessions are bullish for bonds. Which makes this 4% bond yield a “best recession bet.”

Why are we talking bonds when, over the past 18 months, they have all been crushed? Well, that’s the reason. The cure for poor bond performance is the high yields that are now staring us in the face. We look forward, not backward.

If you took our cue and used cash under your mattress as a bond proxy lately, then you are sitting pretty. Because now, we finally have attractive fixed-income yields!

Granted, safety is the key here. Remember, we are picking an economic slowdown as our catalyst. We want to profit in all conditions, but today we are not looking for exposure to credit that may blow up.

We’ll take secure income at levels that we haven’t seen in years. And, as always, we won’t argue with the price upside that accompanies these bargain levels.

Why are recessions good entry points for safe bonds? When the economy slows, rates fall. Bond prices move opposite to rates, so declining rates bring tidy profits.

This hasn’t happened yet. But history tells us it should happen soon.

Let’s look back to 2008. Stocks, commodities and really everything crashed. One of the lone exceptions? US Treasuries, which powered popular iShares 20+ Year Treasury Bond ETF (TLT) to a 28% gain:

2008: TLT was Terrific

The difference in 2008? The economy was already imploding. The financial mayhem was bullish for TLT. The world flocked to Treasuries as the sole secure savings vehicle in the tumult.

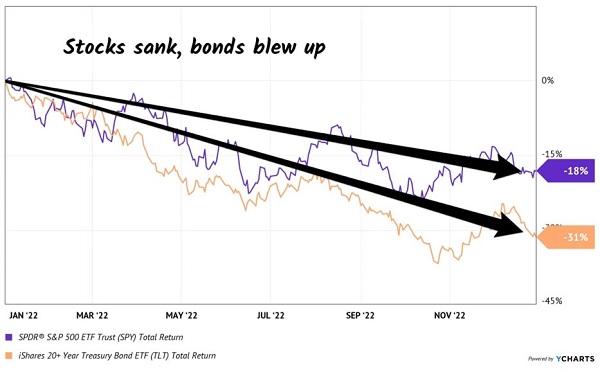

Last year, 2022, was its own special type of dumpster fire. It has been particularly frustrating for retirees because stocks and bonds have collapsed together. Inflation—plus an aggressive Federal Reserve plus a (thus far) persistently steady economy—has drop-kicked both equities and fixed income.

The result is that TLT was no haven. Sure, it still paid its dividend. But even including payouts, the fund plunged 31%—worse than the S&P 500. Ouch!

In 2022, TLT was Terrible

This is not what income investors were looking for from safe Treasuries. But again, let’s remember that in Bondland, bad news eventually becomes good news. Lower prices mean higher yields, which attract yield-hungry buyers.

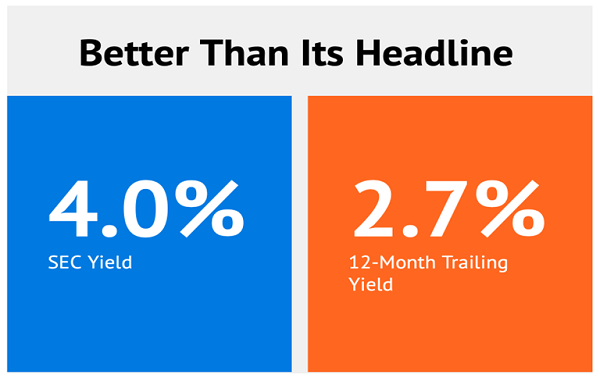

TLT’s trailing dividend is now 2.7%, its highest since 2019. While nothing to write home about, the fund’s SEC Yield—its dividend “run rate” over the past 30 days, minus expenses—is 4%, about 50% more! Now we’re getting somewhere.

Put a million dollars into TLT, and you have $40,000 in annual income. Not quite a 7% “No Withdrawal” Retirement Portfolio, but respectable.

(Pro tip: Always use SEC Yield when evaluating bond funds. This is the distribution stat developed by the Securities and Exchange Commission itself to support a truer yield measurement. The trailing twelve-month yield gets “stale” quickly.

SEC Yield reflects the interest the fund earned, minus expenses, over the past 30 days. It’s the best guide for us today and tomorrow, way better than the TTM payout. For bond yields, we want to know where we’ll go, not where we’ve been.)

So is TLT finally a buy now after its 31% markdown? The 4% yield is nice, and it will get paid, but we want limited downside and some upside. (Why not have it all, right?)

The fund has two drivers that determine its—and any bond’s—price direction:

- Duration risk: Higher future rates are bearish. Lower future rates are bullish.

- Credit risk: What’s the chance that the bond issuer can’t pay us back in the future?

Credit risk is not a concern with Treasuries. If Uncle Sam gets into a bind, he’ll just print more money!

Duration headaches are the reason TLT lost 31% last year and why every other bond and bond fund on the planet has plummeted. But this “threat” is topping out because the Federal Reserve is engineering a recession.

Last year, TLT was repriced. The good news for bond buyers is that the markdown is near completion.

How to play this to win? We contrarians generally prefer bond closed-end funds (CEFs). It’s rare that we consider bond ETFs.

But when we do, we cherry pick deals. And TLT could be one: it’s poised to rally when long-term rates cool down.

But again, TLT doesn’t pay enough to fund a retirement. We need 7% yields or better. Fortunately, they are abundant today!

Thanks to the bond bear of 2022-23, there has never been a better time to put together a “No Withdrawal” Retirement Portfolio. Please read on for the details so that I can share my favorite yields up to 10% with you today.

Recent Comments