I know things feel pretty tense right now. But don’t be pulled into the trap of thinking everything is up in the air these days.

Truth is, there are always rock-solid trends out there that no one can change. I’m talking about sure things that outlast presidencies, wars, inflation, deflation, you name it.

One of my faves: soaring food demand, which is tied straight into global population growth—hands-down the most “baked in” (sorry, I couldn’t resist!) trend there is.

According to the UN, there will be 9.7 billion people on the planet in 2050, nearly 2 billion more than now. That means we’re going to need a lot more food. And yet …

Low Prices, Meet Surging Demand

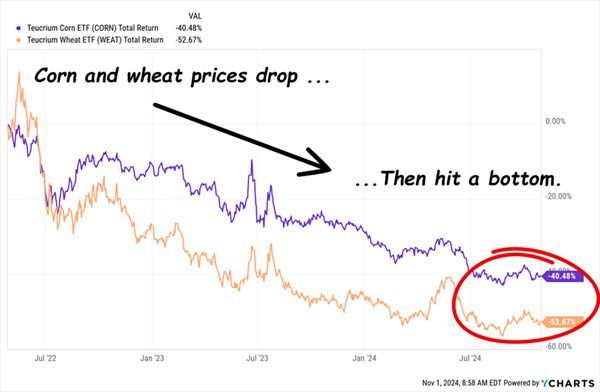

Corn and wheat prices, you may recall, spiked in the spring of 2022, when Russia invaded major wheat exporter Ukraine. Farmers boosted their output in response, spiking the prices of corn, wheat—and the fertilizer needed to grow them.

Of course, excess supply did what it always does: clobbered prices. But they won’t stay cheap because, well, they never do. Low prices are the cure for low prices, and that’ll be the case here, as farmers plant less corn and wheat in favor of something else, such as cotton, creating a supply shortfall—and setting the stage for the next price upturn.

Look at the right side of the chart above. You can see this is already happening, as corn and wheat grab a foothold. I’m also seeing companies boost their fertilizer prices.

That crop-price bottom is our opening. We’re going to grab it with two stocks growing payouts fast—starting with my second-favorite pick of our duo:

Pick No. 2: An “All-Angles” Play on Soaring Food Demand

Corteva Agriscience (CTVA), spun out from DuPont de Mours (DD) in 2019, comes at the ag biz from many angles, supplying farmers with products for pest and disease control, as well as seeds, livestock feed and nutrient maximizers, which help stabilize nitrogen levels in the soil.

All these products boost crop yields—critical because there’s no way we can get enough new farmland to feed those 1.7 billion new people. That makes Corteva a key player.

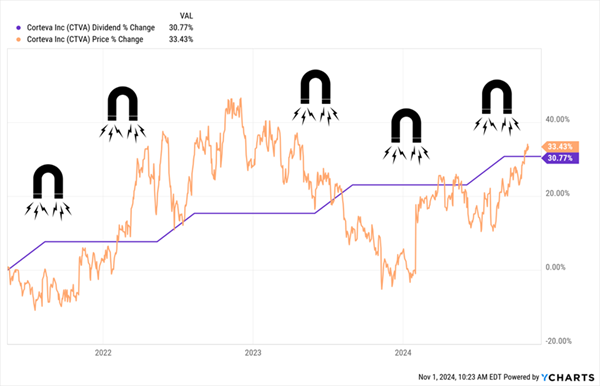

To be sure, the company’s 1.1% yield doesn’t get our pulses racing. But its dividend growth over its short life has been, well, tasty (sorry again!). After taking a bit to find their footing after the spinoff, management has delivered four straight hikes, to the tune of around 31%, in a little over three years.

Since the first hike was announced, on April 30, 2021, the stock price (in orange below) has tracked the payout (in purple) higher—sometimes running ahead, sometimes behind, but always snapping back:

Corteva’s Dividend Magnet Goes to Work

Long-time readers are familiar with the “Dividend Magnet,” and Corteva’s is strong. It can keep those hikes coming, too, with the payout accounting for 56% of the last 12 months of free cash flow (FCF). That’s a little more than the 50% I like to see, but management is calling for $1.5 billion to $2.0 billion of FCF this year, up sharply from last year’s $1.2 billion.

But as you can see in the chart above, the price is tacking a bit above the payout now, indicating that investors are clued-in on this trade. So while Corteva is a great pick to put on our watch list, our next stock—one members of my Hidden Yields dividend-growth advisory will recognize—is on our buy list. Its cheaper valuation is a key reason why.

Pick No. 1: A “Pure Play” on Rising Fertilizer Demand

CF Industries (CF) has a much simpler product lineup than Corteva: It just makes ammonia—it’s the world’s largest producer of the stuff. You can use ammonia as a fertilizer on its own or as a nitrogen additive in other types of fertilizers.

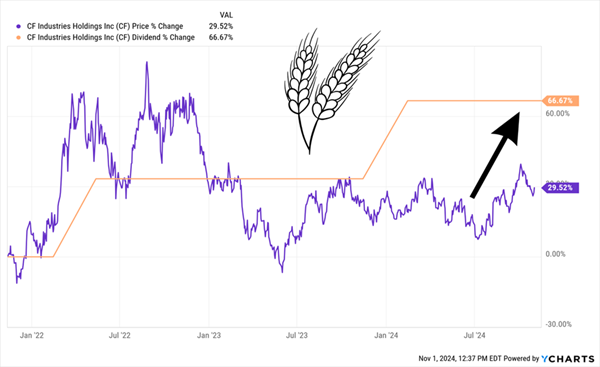

That “clean” connection to rising food demand is one reason why CF is our top play here. The stock’s yield also doubles that of Corteva, at 2.4%. To be sure, that’s nothing to get too worked up about—until you look at CF’s payout growth.

Rising Dividend Points to a “Bumper Crop” of Stock Gains

In less than three years, CF has boosted the payout by more than two-thirds—and while the stock kept pace for most of that run, it broke away early this year. Shares have also moved lower since wheat and corn prices spiked in the spring of ’22. That gives us a nice buy window as “low prices cure low prices.”

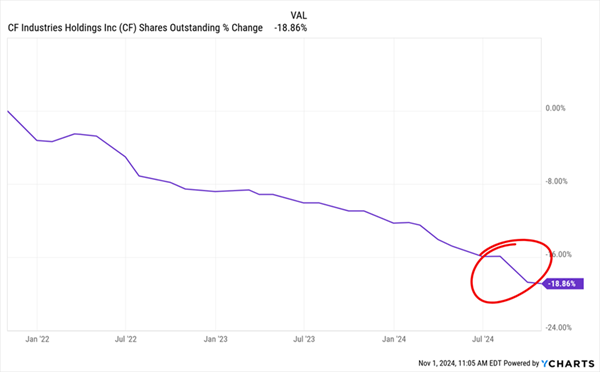

Management agrees the stock is a bargain: In 2024 alone, it ramped up these buybacks as crop prices stabilized, repurchasing 7.5% of the company’s float. That took the total to 18.9% in the last three years, with most coming after the crop-price spike of early ’22.

Buybacks Accelerate at Just the Right Time

There’s lots of room for more buybacks and payout hikes, as CF’s sales and earnings gained in the third quarter, with profits getting an assist from a drop in the price of natural gas, CF’s main feedstock, from $2.58 per million British thermal units a year ago to $2.08.

Cheap North American gas, by the way, gives the company a big edge over its overseas competitors.

Finally, those buybacks cut the number of shares on which CF has to pay dividends, setting the stage for bigger hikes in the future. They also boost EPS and other per-share metrics, throwing a lift under share prices. The fact that the payout accounts for a very safe 19% of the last 12 months of FCF seals the deal.

BREAKING: “Secret” Strategy Delivers FAST 61%+ Gains (More to Come)

The Dividend Magnet is nothing less than the beating heart of the strategy I use to pick stocks for Hidden Yields. And I want to share the entire thing with you right now—today.

This powerful plan has let us bag a surging income stream and BIG, fast gains on winning calls like these:

TD Synnex (SNX): Up 83% in 3 Years

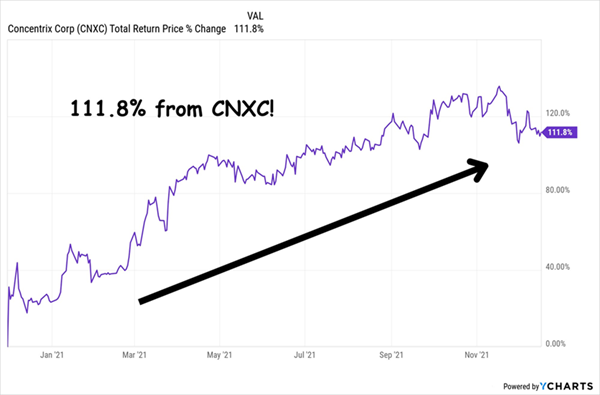

Concentrix (CNXC) Up 111.8% in Just 1 Year!

Or Popular (BPOP), Which “Popped” 61% in a Little Under 3 Years!

I’ve put together a special investor bulletin that walks you through each step and shows you exactly how to use it yourself. You’ll also discover the names and tickers of my NEXT 5 Dividend Magnet winners.

Recent Comments