The spike in volatility we’ve seen in the last month has gotten me thinking a lot about the last decade—when bonds were a bust and tech ruled the day.

Put yourself back in that (seemingly innocent) time for a second.

If you had money to invest back then, you had one choice: stocks. With rock-bottom interest rates, bonds were a bust. And stocks—particularly tech stocks, which tend to do better when rates are low—soared.

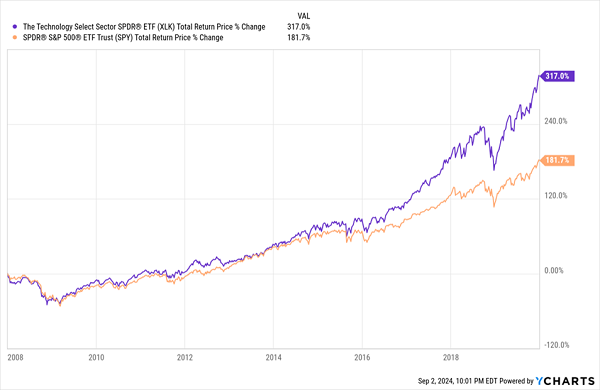

You can clearly see the massive scale of the 2010’s tech surge in the chart below, with tech shown by the benchmark ETF for the sector, in purple. The go-to S&P 500 index fund is in orange.

Cheap Money Fueled the Tech Run of the 2010s

Technological breakthroughs require a lot of upfront investment. But if those investments pay off, the returns can be huge, since tech firms tend to have bigger margins than other businesses. So tech made a lot of sense back then. Funny thing is, it still does, since those margins are still large, tech is still innovating, and the best firms have adapted to today’s higher interest rates.

But here’s where that time differs from today: Now, thanks to those higher rates, we don’t just have to put all our cash in stocks, 2015-style, since bonds pay quite a bit (with some bond-focused closed-end funds, or CEFs, yielding north of 10% as I write this).

This means they give us reliable income regardless of what happens in volatile stock markets. And the last few weeks have shown us quite a bit of volatility.

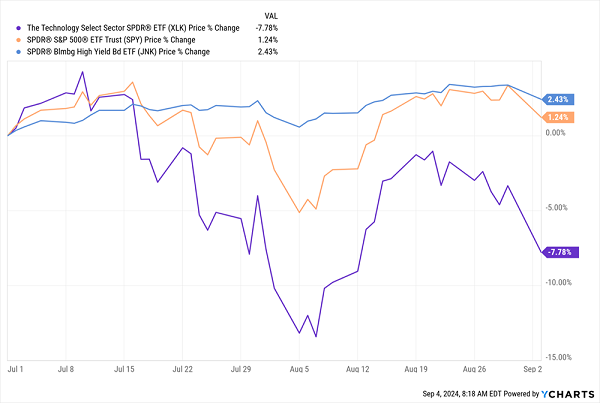

Bonds Have Been a Lifeboat in Late-Summer Market Storms

The above chart shows that even the highest-risk, lowest-rated corporate bonds, shown in blue by the benchmark SPDR Bloomberg High-Yield Bond ETF (JNK), have been mostly calm through the summer, when S&P 500 (in orange) dropped and then bounced back. Tech (in purple) in particular, tanked and still hasn’t recovered.

This is different from what happened in the 2010s, when corporate bonds would typically fall right alongside stocks in a panic.

That’s because back then it made a lot less sense to stick with low-yielding corporate bonds in a selloff, so they sold when stocks did. But with corporate bonds yielding a lot more today, investors hold tight to them in good and bad times. As a result, bonds are a lot more popular today than they have been in a long time.

The financial press has noticed. A couple weeks ago, Bloomberg noted that “Bonds are back as a hedge after failing investors for years.” And growing demand for bonds has helped German insurer Allianz grow its profits more than analysts expected.

That’s because Allianz owns PIMCO, one of the world’s biggest bond investors and bond-fund managers. If you’re a CEF investor, you’ve likely heard of this firm, a vaunted name in CEFs. We also buy PIMCO funds in the portfolio of our CEF Insider service when they’re cheap, though this is rare.

And right now, as usual, PIMCO funds are far from bargains. Luckily, there are other options beyond PIMCO that are still available at attractive prices.

Take, for instance, the 10.9%-yielding BlackRock Debt Strategies Fund (DSU), which has posted a near-40% total return in the last two years, outrunning PIMCO’s more popular funds.

On top of that, the 6.2-year weighted average length to maturity on DSU’s bonds means it has locked in the high yields on its portfolio for a long time, ensuring it will keep its value even as the Fed cuts interest rates, which it has signaled it will start doing ASAP, possibly even later this month.

A mix of strong management (BlackRock is the world’s biggest asset manager) and growing market demand for bonds have also contributed to DSU’s strong performance.

And while I still view DSU as a good pick-up here, it is true that the fund’s near-15% discount to net asset value (NAV, or the value of its underlying portfolio) from a couple years ago is now a small premium of around 1.8%. That might make it sound like we’re late to the party, but I expect that premium (and DSU’s market price) to grow significantly.

However, if you’re a bargain hunter wanting discounts, I get it. The good news is, there are dozens of other CEFs investing in similar assets and trading for less than their portfolio value. They include most of the funds in our CEF Insider portfolio’s corporate-debt bucket.

September Special: Get Full Access to Our Full 9.3%-Yielding CEF Portfolio Now

With September—typically a volatile month for stocks—here, now is the time to hedge your portfolio against a crash by picking up some of the best (and highest-yielding) bond CEFs.

Our CEF Insider portfolio (which yields 9.3% as I write this) currently holds 6 buy-rated corporate-debt CEFs with yields up to 12.3%. Unlike DSU, nearly all trade at discounts!

There’s more: Our portfolio also contains CEFs holding other assets that tend to move in a different direction than stocks, further boosting your portfolio’s safety. They include real estate investment trusts (REITs), municipal bonds, preferred shares and utilities. We’ve also built in a small holding of covered-call funds, which use a sneaky-smart option strategy to slash volatility and pay steady income streams up to 13%.

Look, history tells us we’re almost certain to see some rocky times this month. It’s critical that you have the tools you need to deal with them.

Near the bottom of the page, you’ll get to download a free Special Report naming 4 of my top CEFs to buy now (average yield: 9.8%). And you’ll get a no-risk 60-day “all access” trial to CEF Insider (including our full portfolio), too.

Don’t miss this unique opportunity for safety, high dividends and gains. See you inside!

Recent Comments