Jay Powell is finally making noises about kicking his money-printing habit, and we’re going to set ourselves up to profit with an overlooked dividend payer primed to surge in ’22.

(This company isn’t sexy, which is why the herd has ignored it, but it makes a product every food or drink maker must have—and its dividend has tripled in the last five years!)

A couple weeks ago, we talked about investing legend Martin Zweig’s landmark book Winning on Wall Street. In it, Zweig devotes 40 pages to teaching readers why they should “go with the flow” with respect to the Fed’s trend at any given moment.

Zweig’s point equally applies to Jay Powell’s utterances. And while I don’t think Jay has turned full hawk on us just yet, last week before the Senate, he said the Fed could wind up its corporate bond buying program much sooner than planned. That would move up the timetable for rate hikes.

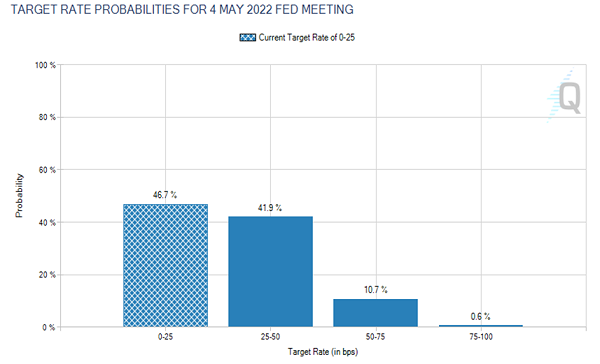

Traders betting through the Fed futures market think so: they’re betting on a hike at the Fed’s May meeting, compared to a majority that favored June a week ago:

Source: CME Group

Far be it for us to defy Zweig’s wisdom and fight the Fed! So let’s go where Powell’s telling us and snap up stocks that will benefit from his drive to steamroll inflation.

How to Time Your “Powell-Powered” Buys

By the way, we’re not going to pile in all at once. With volatility running hot, we’ll give ourselves a margin of safety with my best strategy for “timing” the market. That would be dollar-cost averaging, where you invest a fixed amount in a stock, or collection of stocks, monthly, say. That way you’re naturally buying more shares when they’re cheap and fewer when they’re pricey.

But instead of going all in on DCA, we’ll hold some cash back to hit stocks that are opportune buys, like the “Powell-powered” dividend grower we’ll get into now.

Our “Pick-and-Shovel” Play on a More Aggressive Fed

This company supplies beverage makers with the cans they need to finish their products. And it stands to benefit if Powell takes a more hawkish stand on inflation, because lower inflation would put a lid (sorry, I couldn’t resist!) on its costs, and those of its customers, too. That would let them free up cash to drive sales volumes and invest in new drinks—resulting in higher revenue for our company!

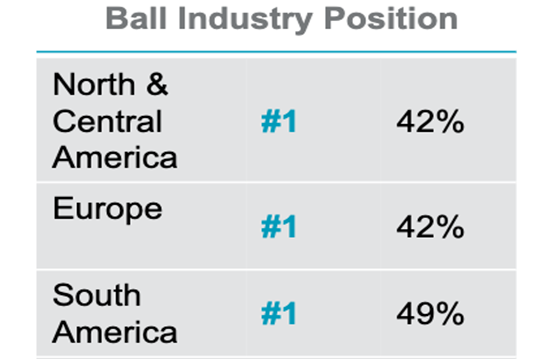

The firm in question is can king Ball Corp. (BLL), which counts Coca-Cola (KO), Anheuser-Busch InBev (BUD) and Molson Coors (TAP) among its clients and holds the leading share of the market for aluminum cans in its three main markets:

Source: Ball Virtual Investor Day presentation, October 6, 2020

A Smart Play on a Growing Environmental Trend

Ball is also in the driver’s seat as consumers demand environmentally friendly packaging, creating an opportunity for aluminum, which, unlike plastic, can be recycled infinitely—according to Ball, 75% of the aluminum produced is still in use!

That’s helping drive adoption, with demand for cans projected to rise by some 100 billion units by 2025, with the North American market expected to post a fat 6.3% compounded annualized growth rate. Cans account for 84% of Ball’s yearly revenue (the other 16% comes from aerospace).

An Accelerating Dividend

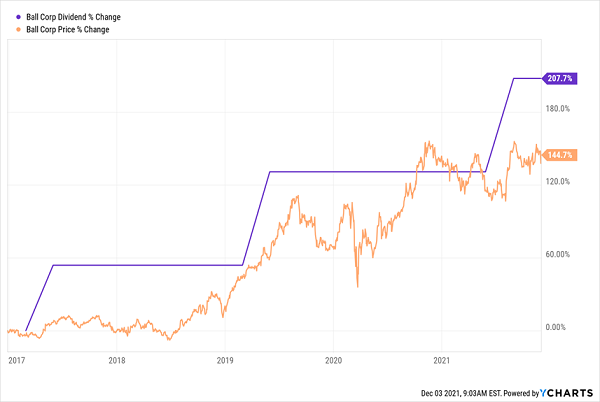

The real hook here is the dividend—which most people would turn up their noses up, with a current yield of just 0.89%. But that ignores the fact that the company’s payout has tripled in just the last five years!

And readers of my regular columns will know that we love a rising payout like this, not only because it boosts our income but because a surging payout is the No. 1 driver of share prices.

I’ve seen it again and again—management hikes the payout, investors take note and buy in, driving the price higher. The result is what I call the Dividend Magnet, and you can see it at work on Ball’s share price in the last five years, with the payout soaring a massive 205% in that time, pulling the share price up 145%. And whenever a gap opens up—as we have now—it’s the time to buy, before the price inevitably reels the payout back in.

Dividend Guides Share Price Higher (The Gap Is Our Upside)

The nice thing is we’re grabbing Ball as it has momentum, with sales up 46% in the last five years, driving a 98% rise in adjusted EPS. A push against inflation from Jay Powell would boost those numbers, with minimal impact on Ball’s borrowing costs: its $8.5 billion debt is reasonable compared to its $20 billion in assets.

The bottom line? If you’re looking for a play on a more aggressive Fed, Ball is definitely worth a look.

7 MORE “Dividend Triplers” Set to Soar (No Matter What the Fed Does)

As we just saw, Ball tripled its dividend in the last five years—and I expect it to pull off a rare “triple-triple”—growing its dividend 3X again in the next five years.

It’s not the only one. I’m pounding the table on 7 other stocks primed to do the exact same thing. These surging payouts are key because, as we just saw with Ball, they drag a company’s share price higher point for point, no matter what Jay Powell, the markets or the economy as a whole throw at us.

My full list of these 7 “dividend triplers” is waiting for you now. The best time to buy them? Right now—as more than a few are primed for imminent dividend hikes. You want to get in before that happens.

Don’t miss out: click here to get the vitals on all 7 of these stout dividend growers—names, tickers, best-buy prices, current yields, the works.

Recent Comments