What if I told you I’d uncovered a dividend “unicorn”: a stock with a 7.4% yield that’s hiked its payout by five digits in the last 14 years?

It’s the kind of thing that “breaks” common investing wisdom. Most folks, after all, think you can have a high yield or a fast-growing payout, but not both. Verizon (VZ) is the classic case, with its 6.9% current yield. Sure, the telco’s payout does grow, but only around a penny a year.

Verizon’s “Pay a Lot, Grow a Little” Dividend

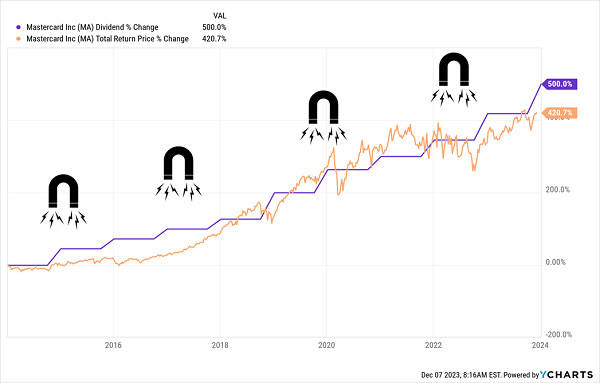

On the other side of the scale is a company like Mastercard (MA), whose dividend has soared 500% in the last decade, from just $0.11 quarterly to today’s level of $0.66.

The trade-off is that you’ll only get a 0.6% current yield, but Mastercard investors don’t care. They’re too busy counting their gains, thanks to the 421% total return they’ve booked, as the dividend marched higher with the share price.

Mastercard’s Fast Payout Growth Drives a Big Return

To be honest, we agree with both sides of the dividend-growth-versus-high-yield debate here at Contrarian Outlook. We seek out high, steady yields in our Contrarian Income Report service, whose portfolio boasts several stocks and funds yielding north of 8% as I write this. On the dividend-growth side, we have Hidden Yields, where we recommend stocks with soaring dividends, which are a key driver of share prices, as you can see with Mastercard above.

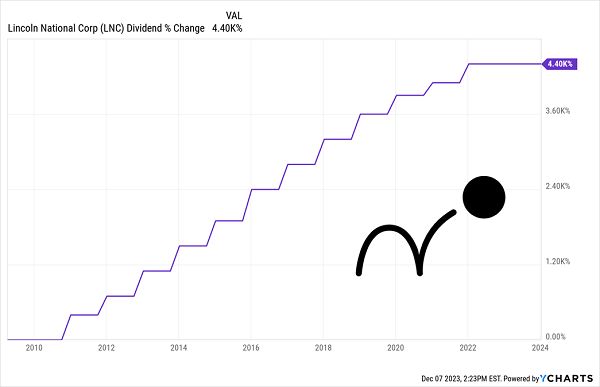

But every now and then we run across a stock like life insurer Lincoln National Corp. (LNC), which offers high yield and strong payout growth. LNC yields 7.4% today and has hiked its payout 4,400% since the trough of the 2008/’09 financial crisis in March 2009.

LNC’s Payout Bounces Back From the ’08 Crisis

LNC has already handed Hidden Yields investors a 20.7% total return in a little over seven months, since our April 2023 buy call on the stock, as of this writing. That translates to a 32.8% annualized return.

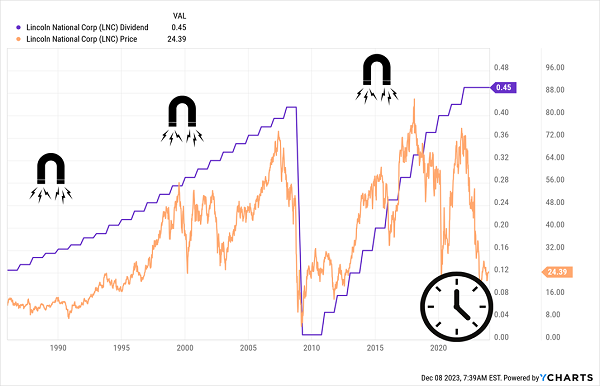

The firm is a 118-year-old insurer that’s a case study in a rising payout pulling a stock price higher—a phenomenon I call the “Dividend Magnet.” Consider the chart below: you can clearly see the pattern of LNC’s share price (in orange) tracking its dividend growth (in purple) since payouts started in the 1980s.

LNC’s Dividend Magnet Is Due

To be sure, management brought in a steep cut during the ’08/’09 crisis, but we can forgive LNC—it was far from alone, especially among financial stocks, back then.

Here’s the key thing: Every time LNC’s price drops too far behind the payout, it gets pulled back up. And right now, its Dividend Magnet is overdue to haul its stock higher again.

LNC has more going for it, too. Let’s review the tape, starting with our initial Hidden Yields buy call in April 2023.

How Our Spring LNC Buy Drove a Quick 20.7% Return

Back in April, LNC was about as cheap a stock as we’d ever seen, trading at a P/E ratio below three. Three! And it was paying a rich 8.3% yield back then, too.

These days it’s still well within the bargain category, trading at 4.5-times its 12-month projected EPS.

Why so cheap? LNC ran into some liquidity problems in late 2022, likely because it bought a bunch of Treasuries just before they plunged, as was the case with Silicon Valley Bank.

Scary comparison, I know, but that was the reason for the sale on the stock: it was priced into the company’s P/E and its book value. Back in April, LNC traded for 64% of the value of its physical assets. In other words, we had the opportunity to get its insurance, annuity, group benefits and retirement planning businesses—not to mention its 118-year-old brand—for free.

Moreover, we correctly believed the issues were transitory. Lincoln National raised money by issuing preferred shares, and let me tell ya, no one buys preferred shares of a company in trouble. What’s more, its Treasury bond positions are bouncing back as interest rates ease.

Meantime, LNC’s dividend was, and remains, sustainable. The company pays 41% of its last 12 months of free cash flow (FCF) as dividends, below the 50% “safety line” I like to see in regular stocks. (Note that some other types of investments can have higher ratios while sustaining dividends, like real estate investment trusts [REITs], which get steady, predictable rents from their tenants.)

The stock was way too cheap, so I pounded the table in the April issue of Hidden Yields, and it went on to deliver that quick 20.7% return.

As the company finishes using excess FCF to shore up its balance sheet and resumes payout hikes, it’s likely to move solidly into the “dividend growth” camp: Further hikes would attract more investors, driving the share price up and the dividend yield down. That’s a good thing—and another reason to give LNC a look now.

More on LNC—and 4 More “Dividend Magnet” Plays Set to Soar in ’24

LNC, along with 4 other dividend growers, combine to form my 5-stock “Dividend Magnet” portfolio. Every stock inside boasts a soaring payout primed to send its price skyrocketing in the years ahead.

Here’s the key takeaway: Now, as interest rates roll over, is the perfect time to buy these 5 unloved payout growers. As Treasuries and other fixed-income investments yield less, investors will flock their way.

Click here and I’ll tell you more about these 5 soaring dividends and how we’ll ride them to serious price gains. I’ll also give you a chance to download a FREE Special Report naming all five—and invite you to “road test” Hidden Yields for 60 days, too. Don’t miss your chance to grab these 5 soaring payouts now, while they’re cheap.

Recent Comments