There’s an opportunity unfolding for us in one corner of the closed-end fund (CEF) market, and we can tap it for 7.5% dividends and price upside, too.

That opportunity is in CEFs that hold preferred shares. And it includes a CEF called the John Hancock Preferred Income Fund II (HPF), which not only pays a 7.5% dividend but is positioned to grow its payout. So every $100,000 you put into HPF gets you $625 a month in income, versus $119 a month you’d get from the typical S&P 500 stock. And that’s just to start.

If you’re unfamiliar with preferreds, they’re like the common stocks most people buy except they pay higher dividends (preferreds typically pay 4% or more, versus the average sub-2% yield on common stocks). They’re also less volatile and tend to rise (and fall) less than common shares (though you can still tap preferreds for strong upside when you buy through a CEF like HPF, as we’ll see in a moment). Banks and other financial firms are major issuers of preferreds.

Before we get into the details on preferred-share CEFs in general and HPF in particular, let’s first look at why preferreds are attractive right now.

Higher Rates Give Preferred Shares a Boost

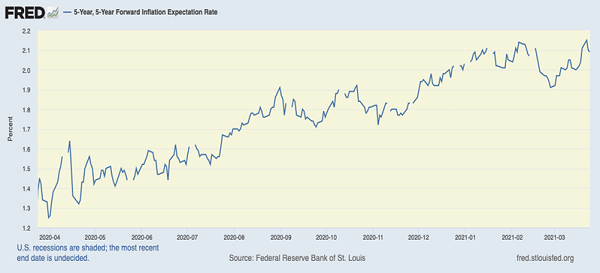

Let’s start with inflation, expectations for which have risen sharply in recent months. Even so, the jump isn’t alarming, with prices expected to rise at around a 2.1% annualized rate over the next five years.

Inflation Expectations Go Up …

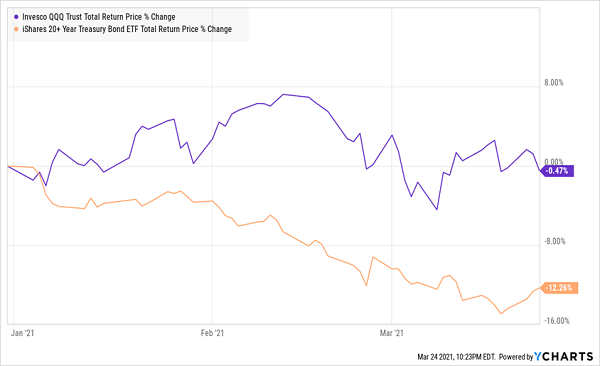

This has caused the yield on the 10-year Treasury note to rise (government bonds typically go down when inflation goes up, and yields move in opposition to prices). It has also caused a pause in the tech-stock bull run as investors reconsider what rising yields on lower-risk investments like Treasuries mean for higher-risk assets.

… and Bonds and Tech Stocks Go Down

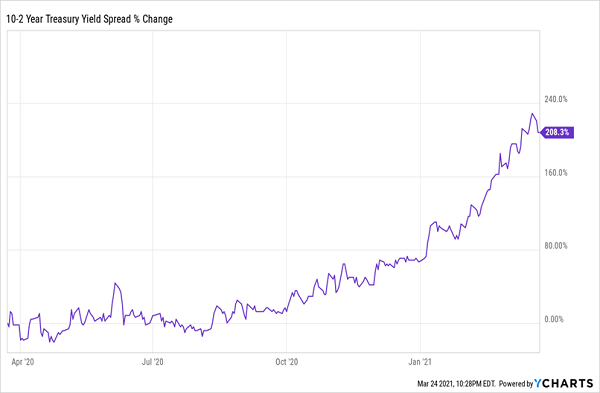

This, in turn, has caused a flood of capital out of these assets and into alternatives, including preferred shares. But it has also resulted in another dynamic that benefits preferreds: a steepening yield curve.

Yield Spread Stretches to a 5-Year High

This chart represents the difference between yields on a 2-year Treasury bond versus yields on a 10-year Treasury bond. This is known as the “yield curve,” and the bigger the difference, the wider that curve is. And we can see that the yield curve is now at its widest since 2015.

This is where HPF comes in, because it holds preferred shares issued by banks, the biggest beneficiaries of the wider yield curve.

Why Banks, Why Now

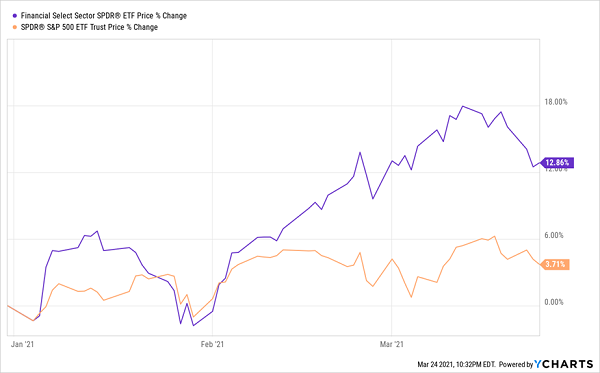

Banks benefit from this setup because they borrow at rates similar to the lower short-term bond yields and loan to businesses and individuals at rates tied to the higher long-term bond yield. They profit off the difference between the two. That’s a big reason why financials are one of the best-performing sectors today.

Bank Stocks Soar on Higher Profits

But we haven’t missed our opportunity here: we can benefit from the financial sector’s good fortune through HPF, which is still available to us at an attractive valuation.

A 7.5% Dividend Set to Grow

HPF invests about three-quarters of its assets in preferred stocks, including preferreds issued by major banks such as Wells Fargo & Co. (WFC) and Morgan Stanley (MS), which are both pulling in higher profits due to the new yield-curve dynamic.

Thus, HPF’s 7.5% dividend is safe, especially since it buys undervalued preferreds that have higher yields, and there’s a good chance the payout will rise as preferred stocks’ prices continue to float higher.

So you could buy HPF now and enjoy your stable high dividend while you wait for its payouts to rise. But if you’re planning to make this move, you should act fast: HPF trades at par to its net asset value (NAV, or the value of the preferred stocks in its portfolio), compared to a 5% discount to NAV just a few weeks ago.

But even though the discount is history, there’s a good chance this fund will rise to a premium as more investors realize that the steeper yield curve is great for banks and, by extension, preferred shares.

Revealed: A 5-Fund “Mini-Portfolio” With a 7.1% Dividend (and 20% Upside!)

The CEF market goes well beyond preferred shares: there are CEFs that hold bonds, blue chip stocks, real estate investment trusts (REITs), utility stocks—you name it. And as I write this, the average CEF yields 7%—nearly 5 times more than what regular stocks pay.

Best of all, these funds are safe: according to my latest research, 96% of CEFs that have been around for 10 years or more made money in the last decade! And when you cut out CEFs in the energy sector, that percentage jumps to an amazing 99%.

The bottom line is that if you’re investing for the long haul, you must have CEFs in your portfolio. These funds, with their high dividends, proven safety record and (in many cases) discounts are the key to generating a safe, high income stream, no matter what the economy throws at us.

I’ve hand-picked 5 CEFs I see as perfect buys right now to create a 5-fund “instant portfolio” containing CEFs from across the economy. They yield 7.1%, on average (with the highest payer of the bunch throwing off an outsized 8.6% payout). Plus, all 5 trade at bargain valuations.

The bottom line? I’m calling for 20%+ price upside from each of these 5 funds, to go along with their huge dividend payouts.

I’ve put everything you need to know in an exclusive investor report that I want to share with you now. Go right here to read it and get full details on these 5 amazing income plays.

Recent Comments