2024 is hours from heading out the door, and here’s the state of play:

The Federal Reserve cut interest rates for a third consecutive meeting on December 18. Yet the yield on the 10-year Treasury is now higher than when the easing cycle began.

Wait. What?

The bond market has been screaming at Jay Powell that the job on inflation is not done. It makes sense: The economy is fine. There are plenty of jobs. The market is not hurting for liquidity.

Finally, Jay is catching on. And here’s the twist: The hawkish guidance he gave on rates at that December 18 meeting—including the Fed’s expectation of two rate cuts next year instead of four—could actually set the stage for a top in the 10-year Treasury yield.

We got a hint of that on December 20, when the personal consumption expenditures price index (PCE) dropped. It’s the Fed’s fav inflation gauge, and it came in lower than expectations, causing the 10-year Treasury rate to edge lower.

This just proves what I’ve been writing about pretty much since the election: Everyone is assuming Trump 2.0 will lead to higher interest rates. And, contrarians we are, we know that when everyone expects something to happen—something else usually does.

“High Rates Forever” Story Has Contrarian Opportunity Written All Over It

Look, I’m not saying that rates are going to suddenly plunge, or that our call for a “no-landing” economy is going to change. But I do see this “high rates under Trump” story as overplayed.

That opens the door for bonds (and bond proxies) as more investors realize this. But we’re certainly not buying Treasuries or investment-grade paper here. The yields are still too low, and Treasuries require us to lock up our cash for a decade.

Instead, we’re shopping mainly in the high-yield aisle, where the biggest bargains (and dividends!) lie. And the best way to do that is through a high-yield closed-end fund (CEF), like the PIMCO Dynamic Income Fund (PDI).

A 14.4% Dividend With a “Stealth” Discount

The simple truth in bond-land is that when 10-year Treasury rates are rising, bond prices are falling, and if Powell’s “adult-in-the-room” stance puts in the top I think it will, buying a bond CEF like PDI right now is a canny move.

The fund is run by PIMCO, specifically Daniel J. Ivascyn, who manages PDI. If you’ve read my articles for a while, you know I’m a PIMCO fanboy. And Ivascyn, who can boast deeper connections in bond-land than just about anyone else, is so respected in the bond world he’s known simply as the “Beast.”

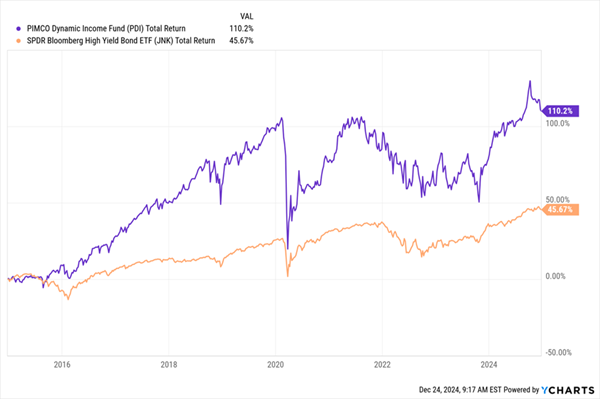

It’s easy to see why: PDI (in purple below) has posted a 110% total return in the last 10 years, as of this writing, more than doubling the go-to corporate-bond ETF (in orange), on the strength of Ivascyn’s skill and deep Rolodex (or, more accurately, iPhone contact book), which tips him off to the best new issues:

Beast Vs. Algorithm: The Winner Is Clear

Now if you’ve skipped ahead and looked at PDI on a screener like CEF Connect, you’re probably wondering why I’m recommending PDI, even though it trades at a premium to net asset value (NAV) that clocks in at 8% as I write this.

Good question! It really does mean we’re paying $1.08 for every dollar of assets here. But here’s the thing: PIMCO is a revered name in CEFs—it’s safe to consider it the Apple (AAPL) of the space—so its funds almost always trade at premiums, and often double-digit ones.

That makes PDI a bargain in disguise, especially when its current premium is below its five-year average of 9.1% and it’s seen premiums as high as 21% in the last few years.

That’s why I continue to rate PDI a buy in my Contrarian Income Report advisory. And since we’re talking dividends, there is one more thing I want to talk to you about today: tracking our portfolios’ dividend payouts—and what a pain it can be! (And a one-click solution that gets as “granular” on your dividend payouts as you want it to.)

Beyond the Spreadsheet

If you’re like me, you dread adding new high-yielders to your portfolio because tracking their payouts can be, well, a big headache.

Like most people, my bills come in every month, and most of my expenses are on autopay. Which makes income tracking more important than ever. I need to make sure I have the money in the account before it gets dinged.

Now we have a better option than the spreadsheet many of us have been stuck with: a specialized “toy” whipped up by our IT team here at Contrarian Outlook called the Income Calendar.

Let’s do a quick run-through, using three strong income plays from our Contrarian Income Report portfolio—PDI, natural gas pipeline operator Antero Midstream (AM) and major utility Dominion Energy (D).

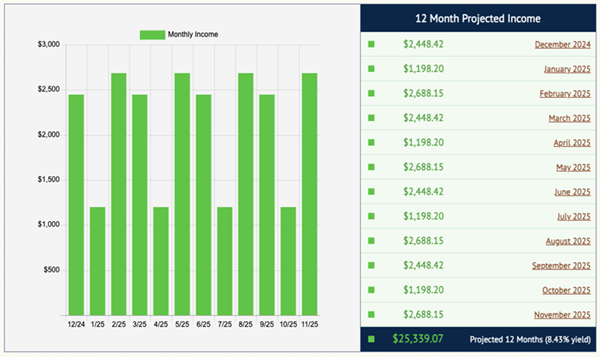

These three pay dividends both monthly (PDI) and quarterly (AM and D). Let’s go ahead and plug them into Income Calendar, allocating $100,000 to each one, for a $300,000 sample “mini-portfolio.”

Right away, IC gives us the vitals—no finicky Excel formulas needed!

On the left, we’ve got an “at a glance” custom income forecast served up for us in an easy-to-read bar chart. And on the right, Income Calendar gets granular, giving us a dollars-and-cents monthly forecast, including our total projected income for the year of $25,339.07, good for an 8.4% average yield. Not bad!

(And note that we intentionally don’t forecast dividend growth in IC, to be as conservative as possible, but it’s possible we could bank a bit more than 8.4% as 2025 plays out.)

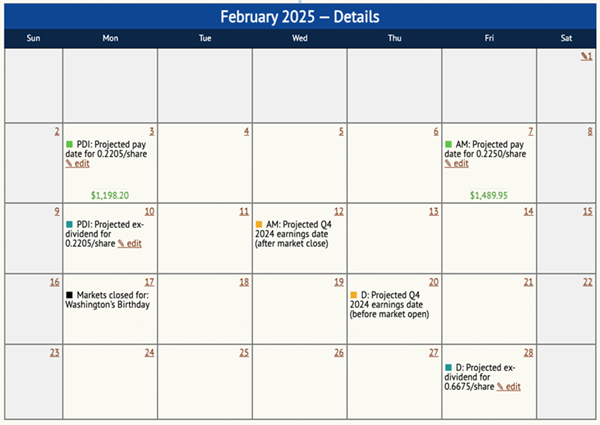

There’s more. Let’s dial up February 2025, one of our highest-paying months, in which we get paid by two of our three holdings.

You can see that Income Calendar not only tracks our payouts (including the exact amount from each stock, in green) but forecasts other key dates, like the ex-dividend date (or the date by which you need to be a shareholder to receive the next payout) and non-dividend-related events like market holidays. It’ll also tip you off to expected earnings dates (we see one of those, for Antero Midstream, on February 12).

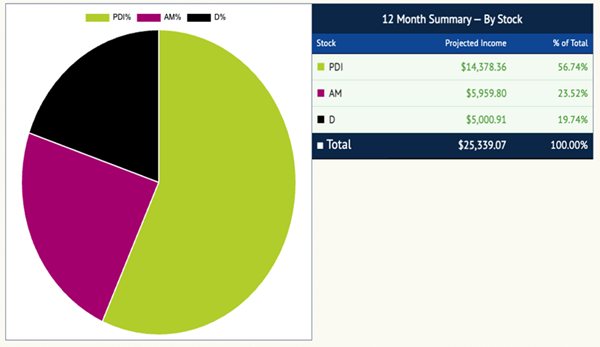

Moreover you can get a sweet breakout by stock, too (no surprise that PDI is the star of the show here, thanks to its 14.4% current yield):

Let’s see an Excel spreadsheet do all that! Income Calendar really is a complete roadmap that makes sure you’re always on top of what’s coming up for your holdings, and you’re never caught short of dividend cash when you need it.

There’s more, too, like real-time email alerts every time a dividend drops into your account, a “week-ahead” summary telling you exactly how much we’ll get paid and when, a handy tool that instantly tells you your “yield on cost” (so you can see the “true” yield on each of your stocks, based on the timing of your original buy) and more.

Click here and I’ll tell you more about this powerful dividend planner and give you the opportunity to “road test” it for yourself. I’m sure you’ll love it.

Recent Comments