Most income investors find their way to business development companies (BDCs) by screening or searching for big yields. And there’s no doubt these listed payouts do appear impressive! Here are the five largest BDCs (ranked by assets under management):

A first-level look at this table may have you wondering why anyone would buy MAIN when they could nearly double their dividend by choosing another ticker. Well, there’s a good reason that we’ll get to in a minute. First, let’s talk about what BDCs actually do so that we can understand what is driving these big dividends.

It all started in 1940, when Congress passed the Investment Company Act. It created a new form of lending with tax benefits similar to those currently enjoyed by REITs (real estate investment trusts). To put it simply, firms that lend to certain types of small companies get a pass on their tax bill if they pay out most (at least 90%) of their income to shareholders as dividends. Hence the big yields you see above.

Also many of these loans have floating rate kickers, so BDCs are positioned to make money in any rate environment. Really, they have a sweet setup. The problem is, their setup may be a little too sweet for the small niche they are all trying to serve. What’s to stop a small company from shopping around for their capital?

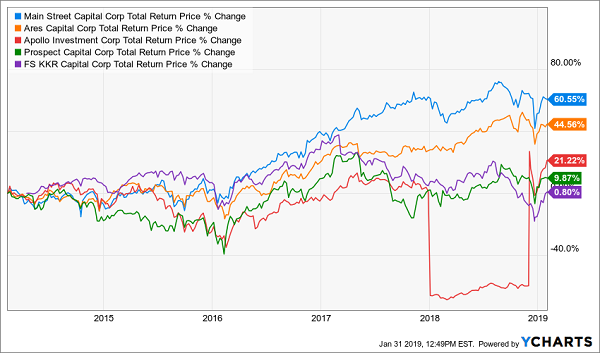

Over the long haul, very few BDCs deliver their dividends without “tapping” their investors’ pockets. In some cases, they fund their payouts partly from the income they derive from their loans (which is good) and partly by selling investors’ assets (which of course is bad). Here’s the tell: over the last five years, only MAIN has delivered total returns above its promised dividend:

Empty Payout Promises: 4 of 5 BDCs “Underperform Their Yields”

Except for MAIN, the other four BDCs delivered lower returns than their dividends promised. Two actually cut their payouts (more on these dogs in a minute). A big dividend doesn’t do us much good if we lose some (or all) of it in stock price depreciation!

Not MAIN however. Two simple yet important things set it apart:

- The firm increases its investment income annually, and

- It conservatively pays its dividend so that it never has to cut it.

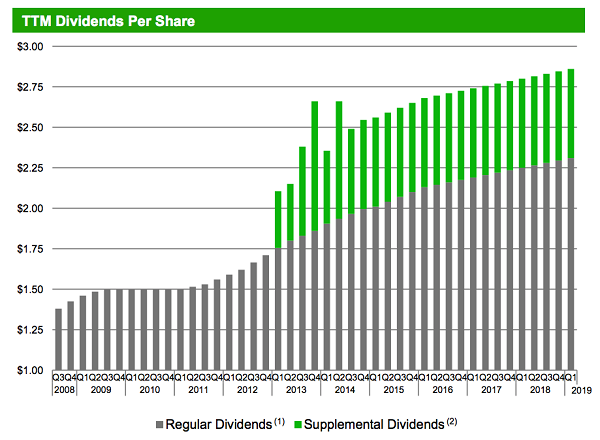

Since its IPO in 2007, MAIN has raised its dividend (which is paid monthly) is up 77%. It’s never been cut, which is rare for a BDC. The company smartly keeps a cash buffer and pays out extra income as a year-end special dividend to make sure its investors (who depend on its monthly dividend to pay the bills) are never short:

MAIN Dividends Per Share (Trailing 12 Months)

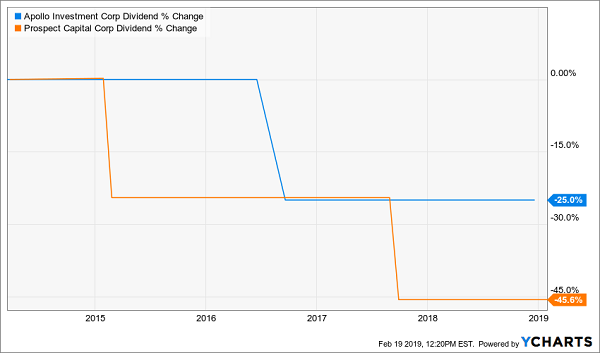

What’s so hard about this? Apparently, a lot. Two of MAIN’s four competitors mentioned above are paying lower dividends today than they were five years ago!

This shows that their lending businesses actually become less and less valuable over time. These stocks, always living on borrowed time, are not the types of investments we want in our No Withdrawal Portfolio!

2 Dividend Dogs

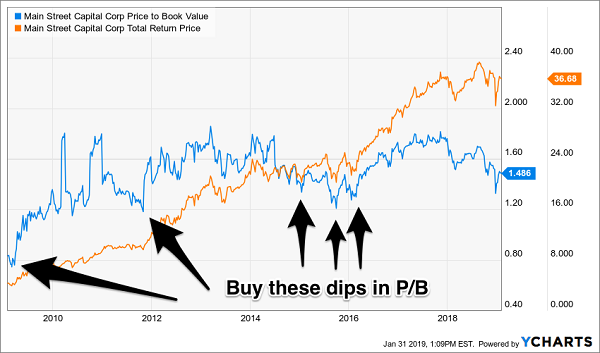

So should we buy MAIN and call it a day? It’s not that easy. As always, the price we pay matters. While most BDCs trade at a discount to their book value (or NAV, the value of the loans in their portfolio) MAIN consistently trades at a premium. Not surprising, considering that it stands out from the BDC crowd in every respect!

The trick with MAIN is to pay as little a premium as possible, because dips in price-to-book (below 1.3 or so) tend to indicate bargains in the stock price:

Dips in Price-to-Book Are Buying Opps in MAIN

MAIN isn’t quite there today, but it’s a good income stock to keep on your watch list. Other BDCs, however, tend to be yield traps. Always check the long-term track record and, unless you see one that is shaping up like MAIN’s, you should probably stay away.

Though we’re not buying MAIN just yet, I do have three more high paying plays I like even better right now with great growth potential on top of their generous current yields.

The 3 Best Bear Market Buys (with 8%+ Dividends) for 2019

With the fourth quarter’s market insanity, you’ve probably thought about dumping – or at least reducing – your stock holdings to focus on fixed-income investments as you near and enter retirement. It sounds like a smart move, but going lean on stocks leaves you open to two big risks:

- That you’ll outlive your savings, and

- You’ll miss out on the long-term gains only the stock market can offer.

So why not blend a portfolio of 8%+ bond funds with smart stock picks that provide you with similarly high yields with upside to boot? Sure, they may “sell off” a bit if the markets pull back. But who cares. Like a savvy income investor, you’ll be able to step in and buy more shares when they are cheap – without having to worry about your next capital withdrawal.

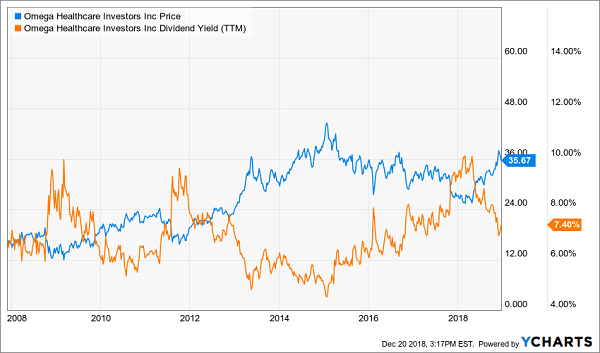

Let’s take healthcare landlord Omega Healthcare Industries (OHI). The firm’s payout is usually generous and always reliable – yet, for whatever reason, its sometimes manic price action gives investors heartburn.

But it shouldn’t. It’s actually quite predictable. Check out the chart below, and you’ll notice:

- When the stock’s yield is high (orange line), its price is low. Investors should buy here.

- When the stock’s price is high (blue line), its yield is low. Investors should hold here and enjoy their dividend payments.

Investing is Easy: Buy When Yield (Orange Line) is High

Of course this simple strategy is much easier to employ if you don’t need stock prices to stay high to retire. Most investors who sell shares for income spend their days staring at every tick of the markets.

You can live better than this, generate more income and even enjoy more upside by employing our contrarian approach to the yield markets. At the Contrarian Income Report, we live off dividends alone. And we buy issues when they are out-of-favor (like right now) so that our payouts and upside are both maximized.

Plus 8% Dividends, Paid Monthly, Make Retirement Even Easier

And by the way, you can even use my “no withdrawal” strategy to make sure you’re:

- Banking 8% annual dividends,

- Enjoying additional price upside, and

- Getting paid monthly to boot!

If this interests you, I’d recommend starting with my all-star retirement portfolio. It contains 8 of the absolute best preferred stocks, REITs and CEFs out there.

If you’re scratching your head at these terms, you’re not alone. These are investments that you won’t hear about on CNBC or read about in the Wall Street Journal. Which is why we have these fantastic opportunities available in this “no yield” world.

I’ll explain more about them in a minute. I’ll also show you why my 8% eight-pack is well diversified across all types of investments and sectors, and the cash flows funding these dividends will do well no matter what happens in the broader economy or stock market.

Plus, as I hinted, relentless dividend growth means your 8% yield will be more like 10% in short order.

I’m ready to take you inside this “no-worry” retirement portfolio now. Click here and I’ll show you the 8 bargain investments inside it and give you their names, tickers, buy-under prices and much more.

Recent Comments