It’s prime time to grab two bond funds tossing out 8%+ dividends now—and we have the Fed (of all things!) to thank for this opportunity.

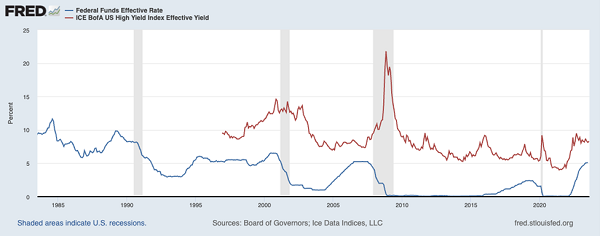

Last year, as we all know (too well), the Fed raised interest rates at the fastest pace in history, bringing them to their highest point in nearly 20 years. As a result, many corporate bonds (represented by the red line above) are yielding a lot more than they used to.

Take, for instance, two bonds from Apple (AAPL), one issued in August 2020 (when the world looked a lot more precarious than it does today, as we still had an unresolved pandemic worldwide) and one issued in May 2023. The CUSIP numbers for these are 037833DX5 and 037833EW6 respectively; any broker can look them up for you.

The 2020 issue yields 0.55%, while the newer one yields a whopping 4.85%.

In other words, if you bought a million dollars’ worth of the 2020 Apple bond, you’d have gotten $458 per month in interest. If you’d bought the bond issued in May 2023, you would be getting a $4,042 monthly income stream!

Trouble is, buying individual bonds (even from Apple) is difficult for individual investors. But that difficulty fades away when you buy your bonds through my favorite high-yield investments: closed-end funds (CEFs).

There are a couple of reasons for this. For one, we don’t need CUSIPs or other more-obscure identifiers to look these CEFs up, as they trade on public markets, just like stock or ETFs.

Second, when we buy through a CEF, we “farm out” our bond picks to a pro. The folks who run the two CEFs we’ll discuss in a second, for example, have deep connections and long experience in bond-land, as well as easy access to the best new issues. That’s key to success in the bond market, which is much smaller than the stock market.

Not all bond funds are made the same, though. You want a fund with a lot of long-term bonds that is paying a juicy yield but isn’t doing so by investing in profitless startups or firms whose businesses are fading into obscurity.

Truth is, there are a lot of CEFs focusing on bonds (CEFs focusing on bonds of various types, as well as bond-like preferred stocks, make up around half of the 500 or so CEFs out there). And as is the case with stocks, mutual funds or pretty well any other asset class, not all of these CEFs are worth investing in—some are dogs, taking on too much risk, suffering from poor management or trading at overcooked valuations.

Fortunately, there’s also a good selection of strong, cheap, high-yielding bond CEFs out there, as well. Here are two, the first of which is a recommendation of my CEF Insider advisory. The second is a fund we’ve got our eye on but isn’t currently in our portfolio.

Corporate-Bond CEF No. 1: A 9.3% Payout Backed By Well-Established Firms

Our first pick is the Western Asset High Income Opportunities Fund (HIO), whose 9.3% yield is compelling because its managers actually have to earn much less than that to keep the fund’s dividend rolling out.

That’s because HIO trades at what in CEF-land is called a “discount to NAV” (net asset value, or the value of the assets in a fund’s portfolio). In HIO’s case, that discount comes in at 9.8%. And because management only needs to cover the fund’s yield on NAV (not the yield on the discounted market price), it only needs to earn 8.4% to keep that 9.8% payout flowing our way.

Here’s the kicker: now that the average corporate-bond yield is 8.3%, targeting that return has gotten quite easy, indeed.

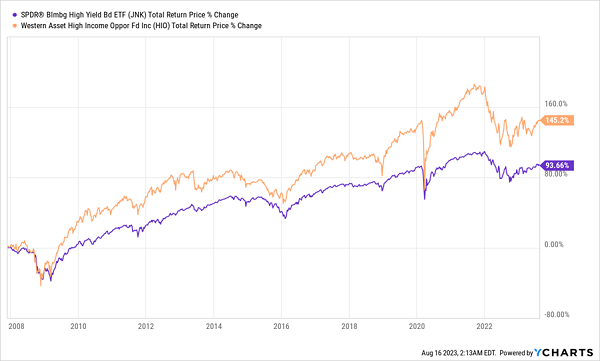

A Long-Term Benchmark Beater

As you can see by the orange line above, HIO has done a great job of beating the corporate-bond benchmark since early 2008 and providing a solid yield, even through the early- to mid-2010s, when interest rates were basically pegged at zero. But after rates went up from 2016 to 2019, HIO’s (monthly paid) dividend started growing, to the tune of a 34% increase over the last five years.

That dividend is backed by bonds from strong companies like investment manager Voya Financial, Kinder Morgan, Carnival Cruise Lines, Delta Air Lines and Teva Pharmaceutical Industries. These aren’t crypto firms or profitless startups; they’re real companies with decades of history and strong cash flows.

And since bond yields are high and set to stay high for much longer than they did before going back to zero in 2020, HIO’s dividend hikes are likely just getting started. The market hasn’t priced this in yet, which is why the fund is still available at nearly 10% off its market price.

Corporate Bond CEF No. 2: A 10.2% Dividend Built on a “Piece of the Rock”

Next, let’s look to the Prudential Short Duration High Yield Fund (ISD), which has a similar 9.6% discount but yields even more: 10.2%. Can this income stream be sustainable?

As is the case with HIO, ISD’s main holdings are bonds from big firms like United Rentals, Pilgrim’s Pride, Voya and Tenet Healthcare.

ISD has a strong track record of finding underpriced high-quality bonds from firms with a solid cash flow. This should surprise no one; ISD’s management firm, PGIM Fixed Income, has ties to Prudential—the insurance firm you may remember from its cheeky “Get a piece of the rock” ad campaign in the 1970s.

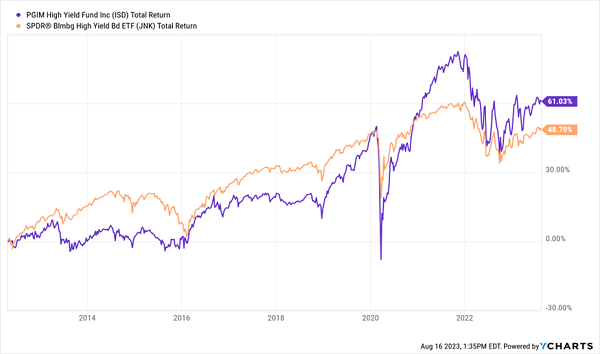

Prudential, of course, has decades of experience in the insurance business, making it ideal for identifying risk and extending credit to the right companies. This has also helped ISD return more than the benchmark high-yield bond index in the last decade:

ISD Outruns the Bond Market

The thing to remember here, too, is that due to its high dividend (its current yield is 10.2%), ISD has delivered more of this return as dividend cash than holders of the ETF (current yield: 6.5%) would have received. And ISD’s payout has held up nicely:

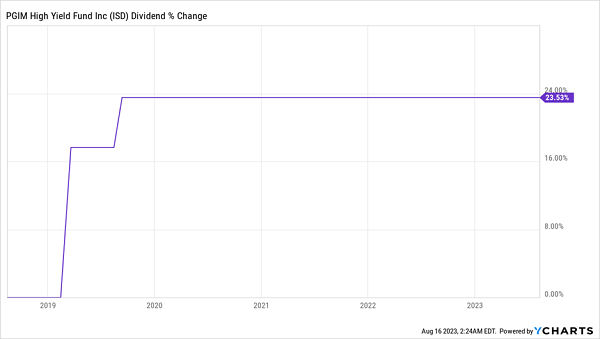

A Steady 10.2% Payout

Higher interest rates in the late 2010s again helped drive ISD dividends up, but the even higher payouts from 2022’s sharp rate hikes have not shown up in the fund’s payouts—yet. When they do, ISD’s 9.6% discount will likely vanish.

These CEFs Pay BIG Dividends (and Make Money 90% of the Time)

My research into CEFs has turned up something shocking: of the 343 CEFs out there that are a decade or older, only 34 have lost money in the last decade!

That’s a 90% win rate.

And if you drop energy funds (which are highly volatile, of course) from the equation, that win rate jumps to 99%! Through wars, a pandemic, inflation, soaring interest rates, you name it.

That speaks directly to the safety of these life-changing, especially if you hold them for the long haul (as I recommend).

To help you secure the biggest, safest CEF dividends out there, I’ve assembled a “mini-portfolio” of my 5 very best CEF picks. They yield an outsized 10.6% on average and are cheap—so much so that I’m calling for 20%+ price gains in the next 12 months.

I’m ready to share them with you. Click here and I’ll tell you more about the overlooked reliability of these funds and give you the chance to download a Special Report giving you my latest research on the five 10.6%-paying CEFs I’ve hand-picked for you.

Recent Comments