I don’t know why you’d try to cobble together an income stream with miserly ETFs when, thanks to this selloff, we’ve got a huge sale on closed-end funds (CEFs) throwing off life-changing 7%+ payouts.

Why are CEFs a great deal now?

In short, the coronavirus scare has caused a “panic disconnect” between many of these funds’ share prices and the value of the assets in their portfolios, known as the net asset value, or NAV.

These discounts are a quirk that only exists with CEFs, and they make our plan simple: buy when discounts are particularly wide, then ride these markdowns higher as they evaporate—pulling the fund’s market price up with them.

Let’s go through two critical areas for any diverse portfolio: real estate investment trusts (REITs) and corporate bonds. As we do, we’ll hit on two low-paying ETFs to avoid—and two discounted, high-paying CEFs that are much better options.

Buying Bonds? CEFs Are a No-Brainer

You may have heard the old excuse for picking passive funds over actively managed ones, like CEFs: that few active managers manage to beat their indexes, so why pay the extra fees?

To be honest, there’s a grain of truth here—but it mainly has to do with stocks. In other corners of the market, human managers beat the algorithms on the regular.

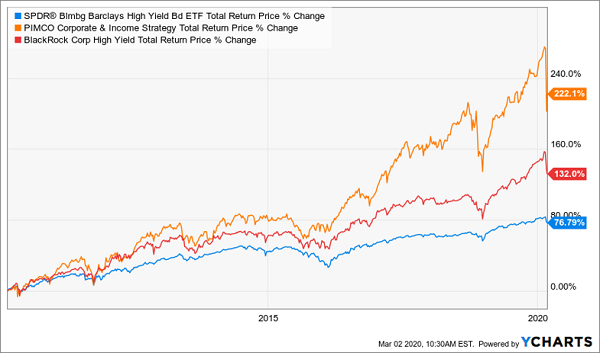

One place where this happens all the time is in corporate bonds. Consider the one-stop high-yield bond ETF everyone knows about: the SPDR Bloomberg Barclays High-Yield Bond ETF (JNK).

A simple screen reveals that JNK has been handily beaten by two other actively managed bond CEFs, the PIMCO Corporate & Income Strategy Fund (PCN)—in orange below—and the BlackRock Corporate High-Yield Fund (HYT), in red, in the last decade:

CEFs: 1, ETFs: 0

Why? Because PCN and HYT are run by PIMCO and BlackRock, two giants of the investment world, managing $1.9 trillion and $7 trillion of assets, respectively.

That unthinkable amount of cash gets you the kind of first-mover advantage you and I can only dream about: when companies issue new bonds, the first calls go to PIMCO and BlackRock. That’s a key difference from stocks, where IPOs are available to a much wider group.

What’s more, you’re getting most of your return in cash from these two CEFs, with PCN yielding a hefty 7.5% and HYT yielding 8.4%, far higher than the 5.6% you’d get from JNK.

So which of these two bond CEFs is the better buy? I’d lean toward HYT, for both the higher payout and its 6% discount to NAV. PCN, for its part, trades at a 22% premium to NAV, even after the market selloffs we’ve seen.

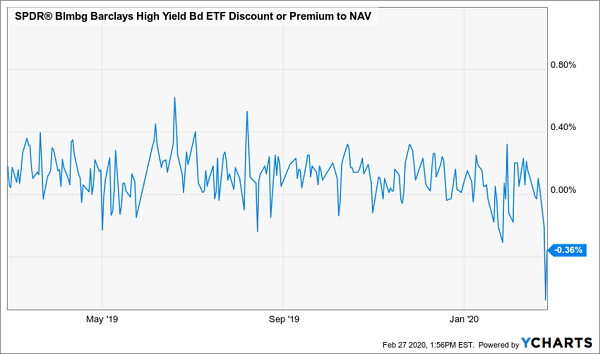

JNK? It’s always priced to perfection:

JNK: No Deal Here

REITs: Pick This Discounted 7% Payer Over the Popular ETF

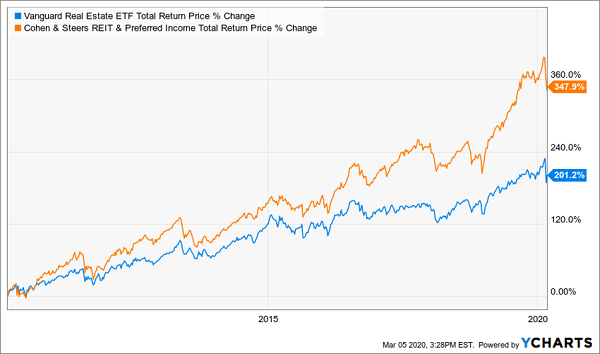

Finally, let’s talk about REITs, high-income “landlords” that have held up better than stocks so far this year, going by the ETF that commands the market, the Vanguard Real Estate ETF (VNQ):

REIT ETF Outperforms SPY …

One reason why so many investors flock to VNQ is its low fees: it charges just 0.12% of assets. Top holdings include Public Storage (PSA), data-center operator Equinix (EQIX), cell-tower REITs American Tower (AMT) and Crown Castle International (CCI), as well as housing REIT AvalonBay Communities (AVB).

VNQ yields 3.6% as of this writing, nearly double SPY’s 1.9%.

But if you focused on fees alone, you’d have skipped the Cohen & Steers REIT & Preferred Income Fund (RNP), which charges 0.87%. Hefty by ETF standards but well worth it. Here’s why.

First, bear in mind that all the returns I’ve shown you in this article (and show you in all my publications, including my Contrarian Income Report high-yield service) are net of fees. And RNP has crushed VNQ over just about every timeframe you can imagine: one year, three years, five years and over the last decade … while charging higher fees!

The Cost of Fee-Focused Investing

I’m guessing you wouldn’t mind paying higher fees for a return like that. And here’s something else to keep in mind: RNP trades at a 6% discount to NAV as I write this. Since that discount is higher than the fund’s management fees, we’re essentially getting the services of RQI’s top-performing managers for free! (In addition to the upside this discount gives us.)

And yes, just like with HYT, you’re getting most of your return in cash, thanks to RNP’s dividend, which yields 6.4% today.

5 “Pullback-Proof” Dividends Paying Up to 9.8% (Buy Now)

At times like this, the best move you can make is to buy the 5 “pullback-proof” stocks I’m recommending now.

These 5 are trading at even more attractive discounts than the CEFs I just mentioned, and they yield an incredible 8.5%, on average. The highest payer of the bunch throws off a massive 9.8% payout!

Think about that for a moment: with nearly 10% of your initial buy boomeranging straight back to you every year in dividend cash, you’re getting a built-in “shock absorber” to protect you in a downturn.

If you hold on for 10 years, you’ll have recouped all of your investment in dividend income alone. At that point, you can ignore the stock price, because everything you bring in—in price gains or dividends—is gravy!

That’s the very definition of safety, and I can’t wait to share these 5 cash-rich dividend-payers with you, along with my complete strategy for surviving—and thriving—in a market storm.

Don’t deny yourself the peace of mind (and high income) you need in these uncertain times. Click here and I’ll give you my full safe-investing plan and everything I have on these 5 “pullback-proof” dividends: names, tickers, buy-under prices, dividend histories and a full rundown of their downturn-resistant businesses.

Recent Comments