How’s your bond portfolio doing? It should be a rock of stability right now.

Of course we may need to look past prices, which can swing wildly, and focus on net asset values and income, which are more reliable anchors.

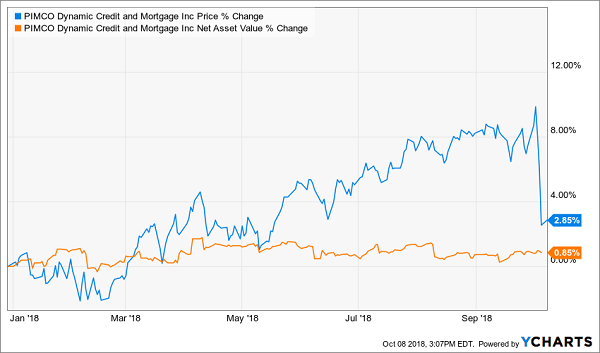

For example I’ve been hearing from readers who were concerned that our excellent PIMCO Dynamic Credit and Mortgage Fund (PCI) isn’t “acting well.” Its price has whipsawed around this year, mostly in our favor. But lately it’s pulled back amidst the broader market drama and subscribers are worried the market “knows something” that we don’t.

Let’s put this price volatility in perspective. The market actually knows nothing – it is simply crazy! If it were sane, it wouldn’t send PCI’s price (blue line below) higher and then lower even though its underlying portfolio value (orange line) stays steady and collects monthly coupon payments:

PCI’s Price Volatility Makes Little Sense

PCI’s own bond portfolio (its net asset value, or NAV) hasn’t budged. And let’s not confuse this stability with malaise. When we add in the fund’s distributions, we’ve earned 11% year-to-date. In fact, by owning PCI, we’ve doubled the riskier S&P 500 by smartly buying secure bonds:

Safe Bonds Double Up Risky Stocks

PCI is still a good buy today, though it’s not quite the screaming bargain it was then. The fund’s “free money” window – its generous discount to NAV – has nearly closed. This initial deal helped us collect 8.6% returns in just over nine months.

So where’s the next bond bargain with “1% per month” potential? I’ll outline 17 great plays that are not currently in our Contrarian Income Report portfolio in a moment.

First, I want to make sure you’re not buying popular marketing vehicles by mistake. You need to stick with handpicked CEFs (closed-end funds) and not be lured by the fancy and frequent advertisements run by the sales wonks promoting their latest ETF (exchange traded fund).

Please, Whatever You Do, Don’t Buy Bond ETFs

Be careful how you buy your bonds. The most popular tickers have a few fatal flaws that’ll doom you to underperformance at best, or leave you hanging in the event of a market meltdown at worst!

Let’s pick on the widely followed and owned iShares iBoxx High Yield Corporate Bond ETF (HYG) as an example. It has attracted nearly $15 billion in assets because:

- It’s convenient, as easy to buy as a stock.

- It’s diversified (for better or worse, as we’ll see shortly) with 998 individual holdings.

- It pays 5.2% today.

The accessibility of funds like HYG appears cute and comfortable enough. But remember, ETFs are marketing products. They are designed to attract capital for the managers, not necessarily to earn you a return on the capital you invest.

And year-to-date, HYG has done exactly what its marketing managers intended. It’s attracted a boatload of money, paid its dividends, and… delivered zero value to shareholders:

HYG: The Worst of Both Worlds

Big money is spent on television, print and online advertisements for ETFs. Less cash and thought is put into the actual income strategies that ETFs employ, and their lagging returns reflect it.

Let’s pick on the three biggest flaws most bond ETFs suffer from. Then, I’ll share a superior way to buy bonds that is just as easy.

ETF Fatal Flaw #1: Underperformance

Investors who typed in “HYB” instead of “HYG” have typo’d their way to a richer retirement. The CEF New America High Income Fund (HYB) is a way better way to buy high paying bonds. It’s outperformed its ETF cousin by a 60%+ margin over the last 11 years:

Since its own inception 30 years ago, HYB has delivered outstanding returns of 9.6% per year with most of it coming as cash distributions.

And it still looks like the better play for new money today. The fund pays 7.9% today and it trades at an 13.4% discount to the NAV of the bonds it holds. In other words, you can buy it for less than 87 cents on the dollar.

HYG meanwhile pays just 5.8% and trades at “par” to its portfolio – or 100 cents on the dollar. No deal there.

ETF Fatal Flaw #2: Ranking the Worst First

“Passive” methods – building portfolios based on rules – don’t work well in the land of bonds because fixed income expertise can’t be readily pre-programmed. Though it’s so rare as to be nearly impossible in equity mutual funds, top CEF bond fund managers can and do deliver truly top returns!

Here’s the main reason why bond indexing is bad. Let’s consider stock indexes, which are weighted by company size. Generally speaking, the larger the firm, the more it matters in the index’s performance.

If you “buy by size” in the debt markets, it’s counterproductive. Stock market value for indexes doesn’t include debt. But bond markets are all debt by definition. Follow the computers in Bond-ville and you’d maximize your exposure to the bonds of the firms that borrow the most money!

That’s the opposite of what we’re looking for in bonds, where our goal is to maximize our “coupon” (the percentage yield) while minimizing our risk (and making sure we get paid back our principal).

Let’s pick on HYG again. Its fifth largest holding is Sprint (S) bonds that expire in September 2023:

That Sinking Sprint Feeling

Will this highly indebted telecom dodge bankruptcy until these coupons expire? Perhaps. This is the type of decision that I’d trust to a human manager (such as at HYB) rather than a computer (at HYG).

ETF Fatal Flaw #3: False Sense of Liquidity

And here’s the “market meltdown” kicker on why you should always avoid bond ETFs:

They are subject to meltdowns if panic selling occurs.

Here’s why. If you sell HYG today, you’ll get your money in exchange for your shares. And it will be iShares’ problem to settle up their end (by selling those Sprint bonds and more).

Problem is, we’re talking about bonds rather than stocks here, and there is no readily available liquid market for that Sprint paper. Which means if a lot of selling occurs, HYG itself may take a hit if it has to unload its bonds at a discount (say, 70 or 80 cents on the dollar) to meet investors’ withdrawals.

CEFs like HYB don’t have this problem. They have fixed pools of assets, which help their managers ride out ups and downs. So long as we hire the best managers plan, who buy good bonds that are funded by reliable cash flows, we (and they) are fine.

The Best Bond Bet: 17 “Hidden Gem” CEFs for 7.5% Yields (Often Paid Monthly)

CEFs are the underappreciated darling of savvy income investors. They are better bond bets for three reasons:

- They are actively managed by pros with a legitimate “edge,”

- Their asset pools are fixed, which means they can (and do) trade at discounts to their net asset values (NAVs), giving us safety and upside, and

- They get access to cheap money, which helps them lever up returns with minimal risk.

Add up these edges, and we have a superior long-term vehicle for fixed income returns, and we can buy them at a discount by being patient income-seeking contrarians. This means we can do even better than the 9.7% that a fund like HYB provided over three decades by “cherry picking” our purchases.

Special CEF Webcast: My Interview with “The Professor”

HYB has only $200 million in assets, which is a very good thing. It can be much more nimble than HYG with its own buys and sells. And thanks to its CEF structure, manager Ellen Terry is never forced to sell her holdings low.

This is exactly why my colleague Michael Foster – our in-house CEF Professor – specializes in these types of under-the-radar CEF opportunities. (I nicknamed him “Professor Michael” because he crunches more numbers than anyone I know.)

The Professor has his computers cranking away to identify the best niche buys that are, quite frankly, not quite liquid enough for me to get my Contrarian Income Report subscribers in and out of efficiently. (Our 11,000+ CIR subscribers would move HYB’s price too much!)

Fortunately, that’s where Michael comes in. His CEF Insider publication is dedicated to diversified, nuanced 7.5% yields and annual total returns of 15% or more.

If you like the idea of bagging bargain dividends and getting paid while you lock in big capital gains to boot, you’ll love The Professor’s research. And next Wednesday, I’m going to interview Michael to see which under-the-radar CEFs he likes the best through the end of 2018 and beyond.

I’ve convinced Michael to “tell all” on this special CEF webcast. So, out of respect to his paid CEF Insider subscribers, we’re requiring a paid subscription to his service to join us for the webcast.

His excellent publication comes with a 60-day money-back guarantee, so there’s no risk to sign up. In fact, don’t tell my publisher I said this, but you can start the risk-free trial now and cancel at day 59 if you want. That’ll get you the invitation to our webcast and a front row seat to our CEF conversation.

If you’re not already a CEF Insider subscriber (or if your subscription has lapsed for whatever reason), you can sign up for your 60-day risk free trial right here.

Recent Comments