The haters are out in full force.

Wall Street “pros” are downright disgusted with high-yield stocks. Here at Contrarian Outlook, this pessimism warms our heart. With no analysts left to slap a Sell rating on these names, the future is filled with upgrades.

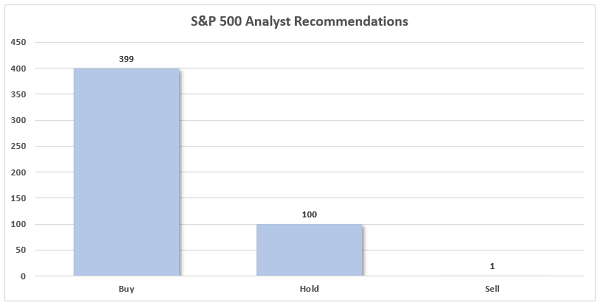

By the way: Consensus Buy calls are a dime a dozen. Analysts notoriously lean, ahem, optimistic, so there’s nothing special about a stock that’s dripping in positive ratings. But if a stock is stuffed with Sells, that’s rare, and I take notice.

How unusual are Sell calls? Just one S&P 500 stock is rated a consensus Sell right now.

One!

Source: S&P Global Market Intelligence

That’s what makes the glut of Sell calls across Dividendland so noteworthy. Let’s start with a dividend duo we have discussed recently.

Northwestern Bancshares (NWBI, 6.2% yield), a regional bank stock that operates in the Midwest and New York, made my list of stocks that are “built to withstand Armageddon.” It’s well-capitalized, and its loan profile is pretty conservative compared to the rest of the regional banking industry. The dividend is pretty safe at a little less than 80% of earnings, though there’s not much room for growth.

In Fact, NWBI’s Payout Hasn’t Budged Since 2021

Wall Street’s view of Northwestern isn’t fiercely hateful, but it’s pretty lousy—not a single Buy, but five Holds and a Sell. And I actually understand their hesitancy.

While NWBI is a sturdily built company, and while net interest margins (NIM) have been trending in the right direction, it’s also richly valued. Shares trade at more than 1.4x their tangible book value. It could be right eventually, but not right now.

The other stock is Arbor Realty Trust (ABR, 12.8% yield), which is hated by everyone. Wall Street is negative (one Buy, two Holds and two Sells), and so are investors, who have turned ABR into one of the market’s most shorted stocks.

You can check out my fuller breakdown of the stock, but it seems foolish to bet against a mortgage REIT that’s able to grow its book value when other mREITs can’t and is still growing its dividend.

2 Fat Financial Yields

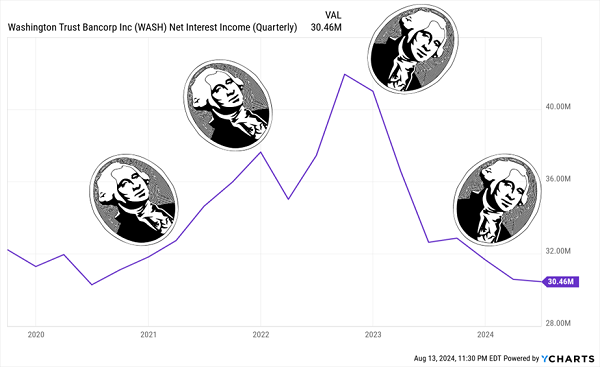

Washington Trust Bancorp (WASH, 7.8% yield) is a regional bank that is neither in Washington State nor Washington, D.C. Instead, this 224-year-old financial institution was named for the nation’s first president, and it was “the first bank to print George Washington’s likeness on currency—69 years before President Washington appeared on the federally issued one-dollar bill and 132 years before the Washington quarter appeared.”

WASH has a 50/50 split of Holds and Sells, largely because the bank’s Secured Overnight Lending Rate (SOFR)-linked loans are acting as a drag on margins. That has forced Washington Trust into a defensive position; it’s largely focused on preserving capital and keeping a cap on expenses. So, it could be a rough few quarters for WASH. Dividend coverage could float above 90% this year. But the bank’s troubles at least appear temporary in nature, and that dividend coverage should loosen up once the Fed lowers rates, which should eventually widen WASH’s margins.

Washington Trust’s NII Has Come Back to Earth

Goldman Sachs BDC (GSBD, 13.2%) is a business development company (BDC) whose management may “draw upon the vast resources of Goldman Sachs to assist in the evaluation of potential investment opportunities.” GSBD’s 155 portfolio companies typically sit between $5 million and $75 million in EBITDA annually, with investments—almost exclusively debt—ranging from $25 million and $75 million.

GSBD doesn’t have a large analyst following, but the few who cover it don’t love it. Shares have 3 Holds and a Sell, and I’m with the analysts on this one. The dividend is actually quite well covered, ranging between 67% and 80% over the past four quarters, yet it hasn’t budged since the company’s IPO in 2015 (though it did pay a few meager special dividends in 2021). Past that, though, GSBD’s almost entirely floating-rate portfolio could struggle when rates dip. Shares are fairly valued at best. And despite the Goldman Sachs credentials, it has spent years underperforming the industry.

1 Familiar Name

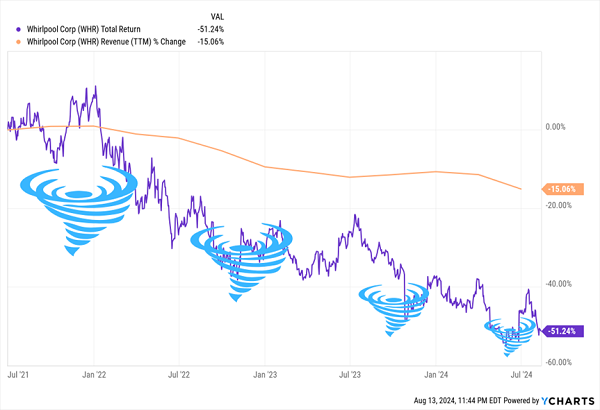

Whirlpool (WHR, 6.8%) has long been a staple of American kitchens and laundry rooms, producing dishwashers, clothes washers, cooktops, microwaves, and much, much more. It does so as Whirlpool, but it also does so under the KitchenAid, InSinkErator, Amana, Maytag and myriad other brands.

Whirlpool has one of the best-covered dividends here—this is a nearly 7% yield that’s a little less than 60% of the company’s earnings. But analysts are surprisingly lukewarm, at 3 Buys, 5 Holds, and 3 Sells.

OK, maybe it’s that Whirlpool is mired in a multiyear losing streak that has seen the company shed nearly 60% of its value.

Or maybe it’s that potential acquirer Bosch has seemingly abandoned its recent interest in acquiring the ailing manufacturer.

Or maybe it’s Wall Street’s expectations for a 25%-plus drop in profits this year.

Whirlpool Is Being Drained Fast

WHR does trade for less than 9 times earnings estimates, and it could be a value play at some point, but for now, it’s just cheap.

1 High-Energy, High-Yield Name

I said in February that Cheniere Energy Partners LP (CQP, 6.8% yield) could be a rough ride, and it has. Shares are down slightly despite a 10% rise in the energy sector. And analysts still hate it—it’s void of Buy calls but rich in Holds (8) and Sells (7).

CQP—a subsidiary of Cheniere Energy (LNG)—owns the Sabine Pass LNG (liquefied natural gas) terminal in Louisiana, which includes production, storage, and vaporizer facilities, as well as marine berths. It also owns the Creole Trail Pipeline, which connects the Sabine Pass terminal with other pipelines.

The Sabine Pass terminal has a lot to do with the Street’s cool views of CQP. Cheniere Energy Partners is looking to begin a massive expansion of the system—an expansion that hasn’t yet received approval, that would take years to complete, and that will require CQP to stash years’ worth of cash to finance. In fact, I mentioned in February that investors could expect a distribution reduction—in less than a month, they got one. Cheniere Energy Partners maintained its regular distribution at 77.5 cents quarterly, but reduced its variable distribution to 3.5 cents per share from 22.5 cents previously. That projects out to the midpoint of CNQ’s $3.15-$3.35 full-year distribution guidance. In other words: This stock could be difficult to deal with for some time to come.

But don’t lose track of CNQ. If the expansion does come to pass, that would be a massive boon to shares and the payout alike.

Think You Can’t Retire on Just $500K? Think Again.

The analysts don’t always get it wrong—some of these high yielders really are duds! Still, a few of these names have the energy to develop into game-changing contrarian plays eventually.

But if you can’t wait to start the journey toward retiring on dividends alone, well, you don’t have to!

My 9% “No Withdrawal” Retirement Portfolio can do what your typical blue-chips-and-basic-bonds retirement portfolio can’t: Allow you to retire on dividend and interest income alone, without ever having to touch a penny of your nest egg.

In fact, by generating at least 8% annually in reliable dividends, you can sleep easy at night knowing your retirement will be secure—even if you have a smaller nest egg of, say, just $500,000.

The math is easy: If you put $500,000 to work in a portfolio yielding 8%, you’ll earn a $40,000 “salary” of dividends from your retirement account. Combine that with Social Security, and you’ll have plenty to work with once you’ve moved on from your career.

Of course, if you have an even bigger pile of cash to plug into our 9% “No Withdrawal” Retirement Portfolio, you’re looking at a downright cozy retirement!

The unloved stocks above either don’t fit the bill or aren’t ready to hatch. But I have plenty of stealth payout plays that do yield the 8% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on these secure funds with very generous dividends!

Recent Comments