Covered-call strategies can be an income investors’ best friend. Whether the broader stock market goes up, down or merely grinds sideways, selling covered calls pays.

Fortunately, we can buy covered-call funds that do the heavy lifting (“call writing”) for us. These funds yield 7%, 12% and yes even 89%. We simply buy them and collect the dividends.

But are all covered-call funds good buys? Of course not. We’ll sort through a popular four-pack in a moment. First, let’s discuss what covered calls are and how they generate income.

Degenerate traders love buying call options to make big bets on stocks. The calls provide them with leverage to acquire a sizeable position that these loose cannons otherwise wouldn’t be able to afford.

As thoughtful income investors, we take the other side of these wild bets. We sell (“write”) covered calls to these gamblers.

A call option is a contract that gives its buyer the right to purchase a stock from the seller for a certain price within a certain period of time. The buyer pays the seller a “premium” for that right.

By selling “covered” calls, we are selling call options against stocks we already own. We receive a premium for selling those options, and in return, we’re obligated to sell our shares at a certain stock price if the buyer exercises that option.

We keep the premium no matter what. If the stock hits the option’s “strike price,” there’s a good chance the shares will be “called away” (we’ll have to sell our shares to the call buyer). But if the stock doesn’t hit that strike price and the buyer doesn’t exercise their option, we also keep our shares!

Because of this dynamic, we can generate income during flat and down markets. And as I mentioned, several funds will do all of the call-writing work for us. Let’s talk about four of them.

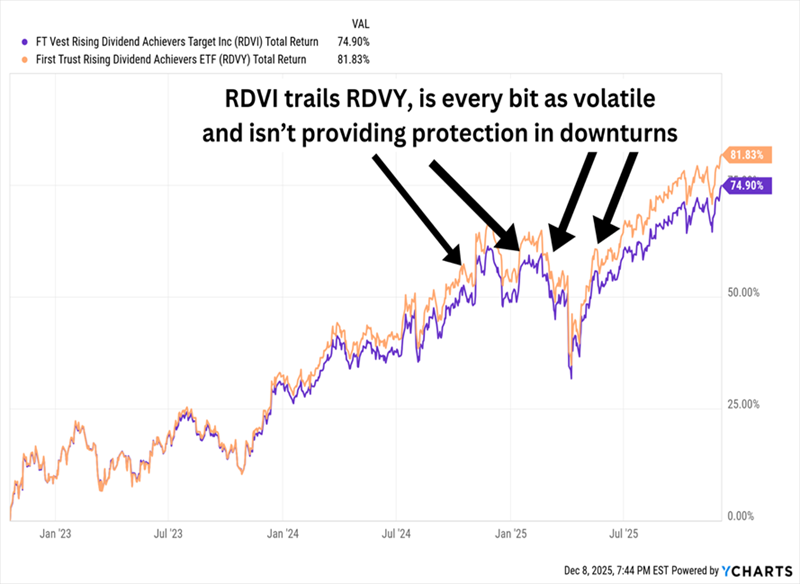

FT Vest Rising Dividend Achievers Target Income ETF (RDVI)

Dividend Yield: 8.2%

FT Vest Rising Dividend Achievers Target Income ETF (RDVI) layers covered calls on top of another equity income strategy. It’s interested in dividend growers—specifically, the members of the Nasdaq US Rising Dividend Achievers Index.

This index doesn’t have quite the reputation of the Dividend Aristocrats. Rather than requiring a baseline of 25 years of uninterrupted dividend growth, this Nasdaq index is looking for dividends that are larger than they were three and five years ago, as well as a few other financial-quality metrics.

RDVI buys Nasdaq US Rising Dividend Achievers and sells calls not against that index (which it theoretically could via the RDVY ETF), but against the standard S&P 500 (or S&P 500 ETFs) to generate income.

It’s a young strategy, so perhaps it’s too early to judge, but so far, RDVI isn’t just underperforming its underlying index (we’d expect that from a covered-call strategy amid a bull market for that index)—it’s showing very little true diversification from its underlying index.

RDVI Doesn’t Achieve Any Meaningful Differentiation

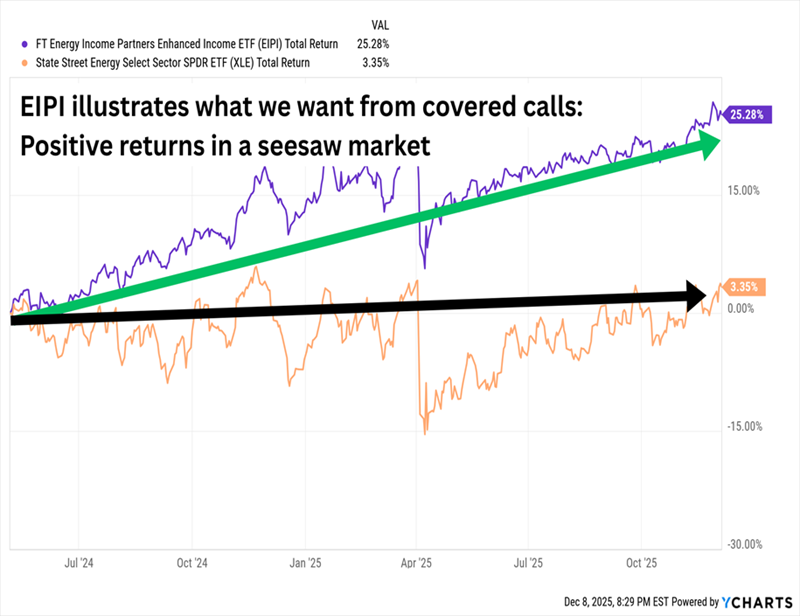

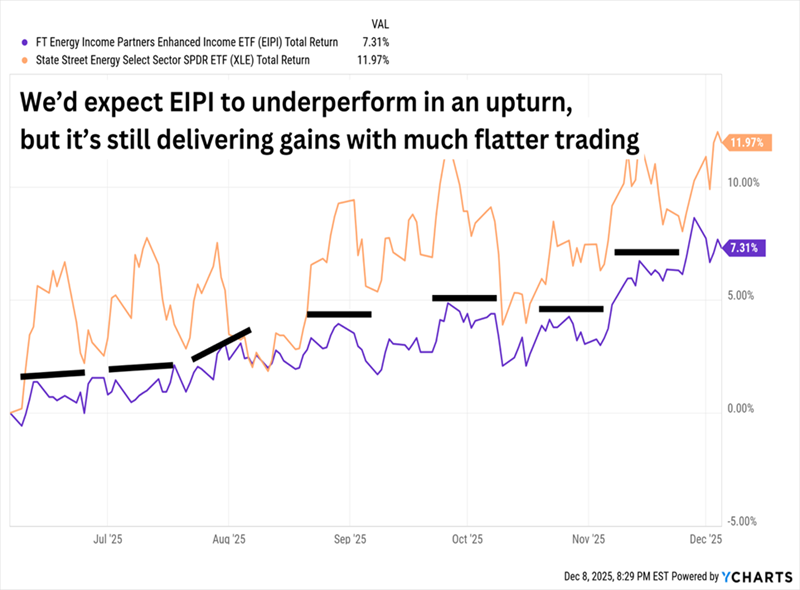

FT Energy Income Partners Enhanced Income ETF (EIPI)

Dividend Yield: 7.3%

Sector-specific covered-call funds are a rarity. Here, FT Energy Income Partners Enhanced Income ETF (EIPI) has shown promise since its 2024 launch.

The actively managed EIPI’s product description actually implies that it’s a plain-vanilla energy fund: “Under normal market conditions, the Fund will pursue its investment objective by investing primarily in a portfolio of equity securities in the broader energy market.” And the portfolio is exactly what we’d expect from an energy-sector fund—significant allocations to stocks such as Enterprise Products Partners (EPD), Kinder Morgan (KMI) and Exxon Mobil (XOM).

But not only do EIPI’s managers engage in selling covered calls—they trade options on the individual stocks, not a broader energy index. As I write this, the fund has nearly 50 options positions, which is well more than we see with traditional index-based strategies.

The yield isn’t anything special for a covered-call fund. And yet, in its short history, EIPI has:

- Beat its energy benchmark.

- Delivered smoother returns.

EIPI Outperforms Its Energy Benchmark

EIPI Delivers Smoother Returns

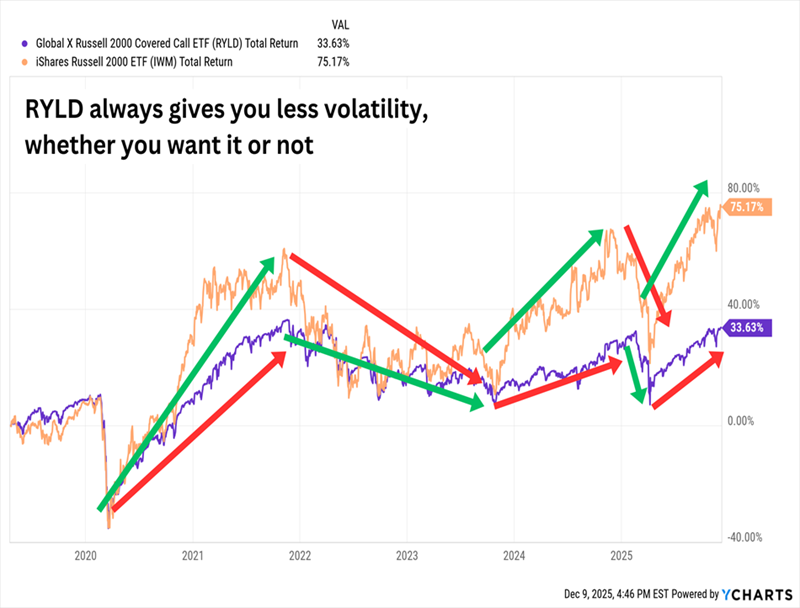

Global X Russell 2000 Covered Call ETF (RYLD)

Dividend Yield: 12.1%

Global X Russell 2000 Covered Call ETF (RYLD) uses a covered-call strategy on a lesser-known index, the small-cap Russell 2000. It’s a straightforward strategy—RYLD holds the Global X Russell 2000 ETF (RSSL) and sells calls against it.

In theory, small caps would be a great place to see the power of covered calls come alive given their significantly higher volatility compared to larger stocks. Higher volatility means higher premiums, which means more income for us. In practice, RYLD’s returns have been lackluster:

RYLD Has Underperformed Its Index Significantly

The good news is RYLD consistently provides the limited downside we’d expect whenever the Russell 2000 slides. The bad news is RYLD consistently provides the limited upside we’d expect whenever the Russell 2000 runs. It underperforms its index by too wide a margin for us to get excited about.

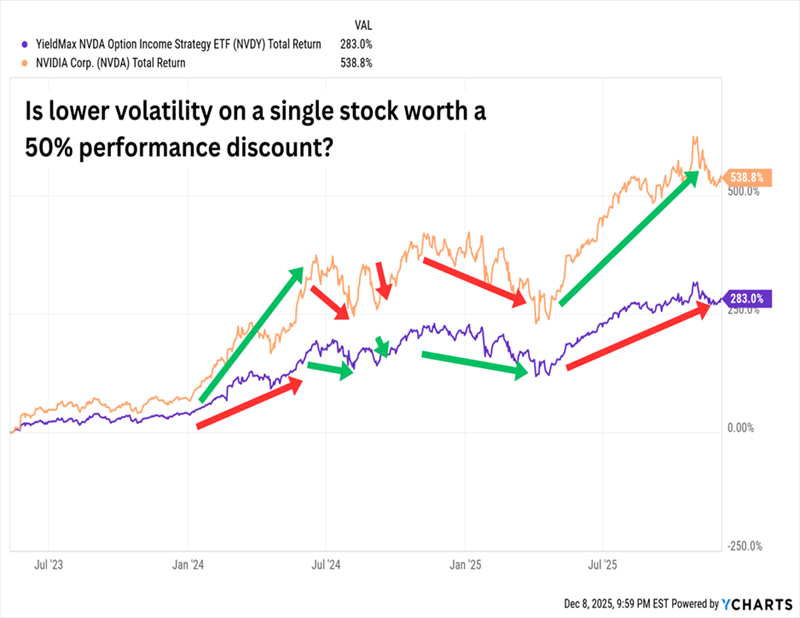

YieldMax NVDA Option Income Strategy (NVDY)

Dividend Yield: 88.9%

YieldMax NVDA Option Income Strategy (NVDY) buys shares of NVIDIA (NVDA) and sells calls against them. This is a cash machine on paper but in practice NVDY gets lapped by NVDA itself:

NVDY Can’t Keep Up with NVDA

NVDY is a bit more exotic than the average covered-call fund, trading not just covered calls, but also call spreads (buying a call with a lower strike price, then selling a call with a higher strike price). That helps to generate a downright laughably high yield of nearly 90%.

Problem is, these returns may not be sustainable if NVDA’s rocket ship ever stalls. This whole strategy is predicated on NVDA trading forever higher.

The Easiest Way to Sell Covered Calls on Your Portfolio

A few covered-call and other options-income funds hit the mark, but many of them struggle because, as funds that make their money from trading options, they’re forced to trade options … even when the environment isn’t quite right.

The problem? If their timing is off, depending on their strategy, they could see:

- A core portfolio position “called away” (covered calls). Sounds like a winning trade, but this is problematic as we now have to decide when to re-enter the position. And from a tax standpoint, this type of overtrading can leave us with a big tax bill at year end.

- A truckload of shares we don’t want (or can’t afford) being “put” to us (selling puts) because we didn’t pick a strike price far enough below the current sea level of a stock. This is happening a lot these days with manic markets taking perfectly good positions down dramatically over the course of a few days.

That’s why I designed OptionSignals. And that’s why I’m letting readers try it for 60 days at no cost whatsoever.

OptionSignals is an easy-to-use, automated tool that automatically flags the optimal times to sell calls and puts on positions you already own. We built it in-house, at Contrarian Outlook, adapting my buying-and-selling timing system with signals that are different from those used by mainstream Wall Street analysts and quants.

You can set up custom watchlists using any optionable stock or fund on the market, or sync up your own portfolio to the service in just a few clicks. And if you’re a subscriber to Contrarian Income Report, Hidden Yields, and/or Dividend Swing Trader, you can import those entire portfolios into OptionSignals and generate options income from them!

And every morning, before the market opens, you’ll receive an easy-to-read alert identifying any tickers that have entered a profitable setup.

If that sounds like a system you’d like to try out, now’s your chance—I’m offering you a 60-day trial to OptionSignals completely free of charge. Click here for a quick tour, and you’ll be ready to turn your portfolio into a perpetual income machine.

Recent Comments