Today we’re going to talk about the single biggest risk you face in your golden years.

But don’t worry—I’ll also show you how to clobber that risk and set yourself up for an easy $40,000 in cash for every year of your retirement. More on that below.

Let’s address the nasty risk first—the very real chance you’ll outlive your nest egg. A sweeping study says you could be very wrong about the length of your retirement.

A Hidden Danger

Here’s what the numbers say: in 1992, the University of Michigan asked 26,000 Americans 50 years of age and older how long they thought they’d live. The results, 25 years later, are in, and they’re staggering.

When first asked, 7 percent of participants said they had zero chance of making it to 75. But despite their pessimism, 49.2% did just that. Of the folks who gave themselves a 50/50 shot, 75% went on to do so.

So now might be a good time to rethink your expectation of how long you’ll live—because you’ll likely be around a lot longer!

Don’t Buy Wall Street’s Retirement “Solution”

Here’s where Wall Street comes in, with a “solution” only it could cook up.

It’s called the 4% withdrawal rule, and it recommends supplementing your dividend income by withdrawing 4% from your capital every year in retirement.

Trouble is, every few years you get a situation like this:

The 4% Plan’s Fatal Flaw

As you can see, you’d be forced to sell shares of Microsoft (MSFT) and withdraw your money at exactly the wrong time. Microsoft’s dividend is fine, but you still need to sell shares for extra income.

Remember dollar-cost averaging, which you may have used to build your nest egg? This is the same phenomenon but in reverse! In this scenario, you’re selling more shares when prices are low and fewer when prices are high.

It’s a straight path to prematurely running down your savings. And it pains me that so many folks take it as gospel.

But don’t despair, because there’s an easy solution: build a retirement portfolio with an outsized dividend yield. I’m talking an 8% average payout or better. That would be enough to live on dividends alone with as little as $500,000 saved up.

I’ll show you the 3 investments that hold the key just a little further on.

But bear with me, because before we build our high-yield retirement portfolio, we need to purge the “sacred cows” that look safe but actually drain your returns—starting with these 3:

Fixed Income

As I write, 10-Year Treasuries yield 2.4%. You could get the same from a CD … if you lock away your cash for 5 years.

That’s a lot to ask for 2.4%. And this is the definition of “dead money,” because you’ll get no capital gains, just your cash back after the 5 years is up.

This may sound safe, but inflation will eat most of that 2.4%, leaving you right back where you started. And if you did try to retire on it, you’d need to invest $1.7 million to drive a $40,000 yearly income stream. That’s just not realistic for most folks.

Dividend Aristocrats

You’ve probably heard of these 50 companies, which have raised their dividends annually for 25 years. Some of America’s best-known firms make the cut, like Walmart (WMT), 3M (MMM) and McDonald’s (MCD).

And there are some decent picks among the so-called aristocracy. But the average Dividend Aristocrat, as measured by the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), pays even less than the 10-Year: just 1.8%! So you’d need north of $2.2 million to get our theoretical $40,000 income stream.

Worse, your average Aristocrat has underperformed the S&P 500 over the 4 years since NOBL was launched.

Aristocrats Humbled

That’s disappointing because dividend growth is the No. 1 driver of share prices, so these companies should have a built-in edge.

The problem? Too many Aristocrats—AT&T (T) and Colgate-Palmolive (CL) among them—churn out tiny yearly increases just to stay in the club, and it’s not enough to tempt the income-starved masses.

Consumer Staples Stocks

The third “sacred cow”? Consumer staples stocks with household names like General Mills (GIS), Coca-Cola (KO) and Kimberly Clark (KMB).

The conventional wisdom says it’s smart to put your nest egg in these stocks because people buy their products no matter what the economy does.

But it’s not that simple. Because as I wrote a couple months ago, many big consumer staples names are on the wrong side of a growing food trend: more folks opting for fresh over packaged fare.

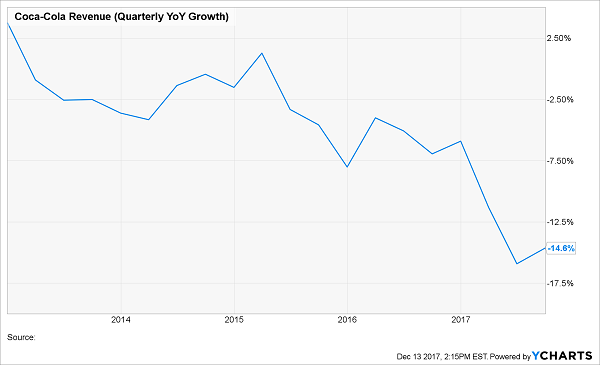

Meantime, homegrown competitors are eating the big guys’ lunch. Take Coke, which has only posted quarter-over-quarter sales growth once in the past 19 quarters!

Coke Sales Fizzle

(This isn’t the first time I’ve flagged Coke as a stock to worry about. I took a closer look at its “red flags” in my recent article “Why Coke Could Be the Next GE.”)

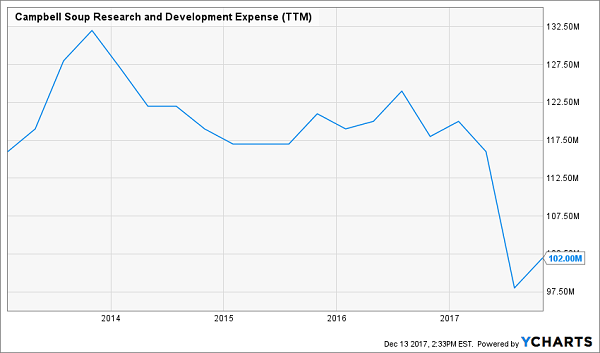

Meantime, at Campbell Soup (CPB), earnings are up—but sales are also in freefall.

Campbell: What Goes Up…

How is Campbell doing it?

Cost cuts—including to research and development, exactly where management needs to spend if it wants to fend off the competition.

Campbell Throws in the Towel

We need to do better. Which brings me to…

Your 3 Retirement Lifeboats—for Yields Up to 8%

The good news is that topping the popular choices is easy. We just need to go where first-level investors aren’t, starting with…

Closed-End Funds

Here’s something most folks don’t know: you can double, triple or even quadruple your dividend payouts by switching from the average S&P 500 stock to a closed-end fund (CEF).

And you can often do it without even switching investments!

Here’s just one example: if you own JPMorgan Chase (JPM) or American Express (AXP), you can “trade in” their payouts (1.9% and 1.3%, respectively) for a 5.9% dividend from the Gabelli Dividend & Income Trust (GDV), which has both stocks in its top 10 holdings.

Better still, GDV trades at an 8.2% discount to net asset value (NAV, or what its underlying portfolio is actually worth). That makes the dividend safer, because fund manager Mario Gabelli only has to make 5.3% of NAV—not the 5.9% yield on GDV’s market price—to keep its payouts coming. That’s a cinch for a seasoned vet like him.

Real Estate Investment Trusts

REITs—owners of properties ranging from apartments to self-storage units—don’t pay income taxes so long as they hand over most of their earnings to shareholders.

That means bigger dividend checks for us!

Take Apple Hospitality REIT (APLE), a bargain hotel REIT I showed you earlier this month: it pays a gaudy 6.2% dividend yield now—and that dividend is safe, thanks to APLE’s low (for a REIT) payout ratio of 69% of funds from operations (FFO; a better profitability measure than earnings per share for REITs).

Better yet, thanks to overblown fears that interest rates will hurt REITs, APLE is cheap today, at just 11 times FFO!

Preferred Shares

Preferreds are stock-bond hybrids that can trade on exchanges, like common stocks, but trade around a par value and dole out a fixed regular payment, like a bond.

Their biggest appeal? Massive payouts!

Many preferreds boast payouts of 7% and higher. Trouble is, the preferred-stock world can be complex, so my favorite way to tap into them is through closed-end funds. This puts an experienced pro to work spotting the best opportunities for us.

And when it comes to preferreds, the human edge makes all the difference.

Take the Cohen & Steers Preferred & Income Fund (LDP), which I showed you in August. It pays a 7.2% yield now and has crushed two of the most popular preferred-stock ETFs in the last five years:

Human Management Wins Out

The bottom line? Throw APLE, LDP and GDV in together and you’ve got an “instant portfolio” with a 6.4% yield—enough to hand you $40,000 of yearly income on a $620,000 upfront investment.

But we’re not stopping there! Because your best strategy is to go just one step further and …

Make a $500,000 Nest Egg Last Forever

The trouble with putting all your cash in APLE, LDP and GDV is that you’re betting your whole retirement on just 3 investments!

That’s just too much risk for my liking. And let’s be honest, $620,000 is still a lot of money for many folks to save.

So what if I told you that you could kick-start that same $40,000 income stream on a lot less cash—$120,000 less, to be exact.

That’s right: $40,000 of income every year on just a $500,000 nest egg.

Oh, and you’re getting a lot more diversification here, because we’ll spread your cash out over 6 rock-solid investments instead of just 3 (and yes, they’re all CEFs, REITs and preferred-stock funds).

They’re all in my 8% “No-Withdrawal” retirement portfolio, which I’ve custom built to protect your nest egg in a downturn and deliver an 8% average dividend all the time, easily enough to hand us $40,000 a year on just $500,000 in savings!

Best of all, you won’t have to worry about outliving your cash, because unlike Wall Street’s deadly 4% plan, you won’t have to draw a single penny of your capital in retirement!

I’m ready to share all the details with you now. CLICK HERE and I’ll give you my full strategy, plus the names and ticker symbols of each of the 6 winning income plays inside this portfolio.

Recent Comments