This private-credit mess we’ve been talking about lately has raised a question no one wants to ask: Is 2026 shaping up to be another 2008?

It’s easy to see why some investors may be thinking along those lines. And it’s something I’ve been giving a lot of thought to lately. But here’s the twist: There’s another year I think 2026 resembles a lot more than 2008.

That would be 2023.

If you remember, that year was a buying opportunity in stocks—and to pick up the closed-end fund (CEF) we’re going to discuss today. In fact, both 2008 and 2023 ultimately turned into strong setups for this 7.7%-paying fund.

And today’s private-credit woes open the door to another strong run from here.

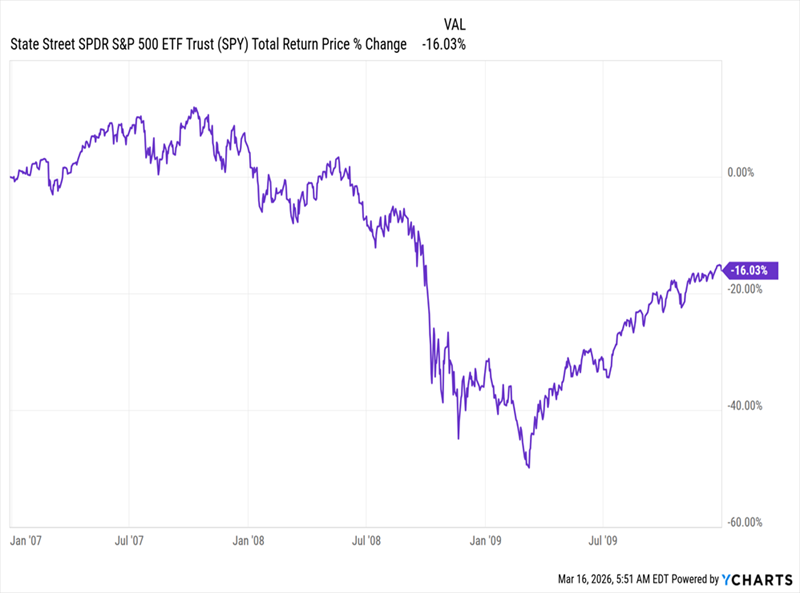

2008, of course, needs no introduction. Back then, a housing bubble inflated by subprime mortgages took down the global economy. (If you’re too young to remember, I’d recommend watching The Big Short.) The S&P 500 fell more than 50% from its 2007 peak till it reached the trough in early March 2009. Stocks didn’t see that 2007 high again until mid-2012.

2009 Was the Start of a Long Grind Back …

Then there’s the other (and in my view more likely) possibility that if we do see a disruption this year, it’ll look more like 2023, a time we can all remember.

Early that year, the failure of Silicon Valley Bank and some other regional lenders brought back dark memories of what had happened 15 years earlier. But if we look at what’s happened since, it quickly becomes clear that the 2023 dip was a fantastic buying opportunity:

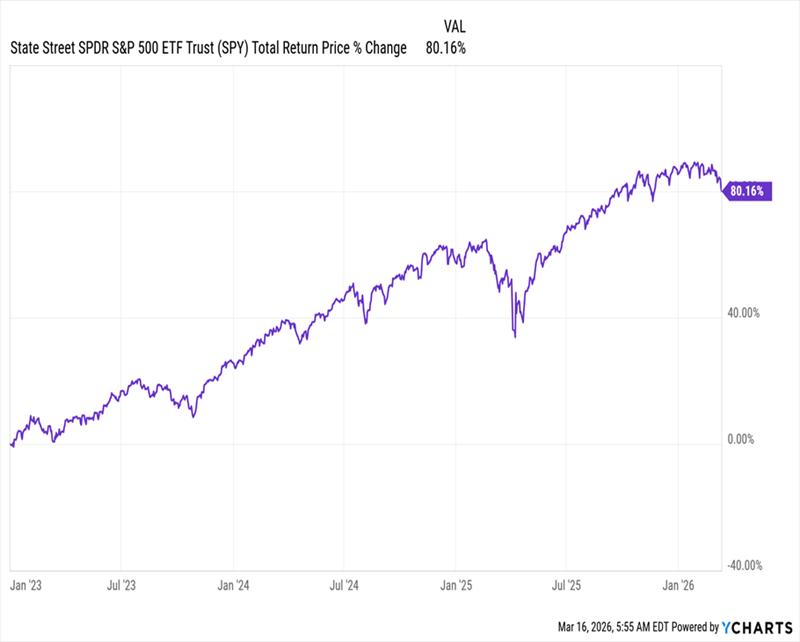

… While 2023 Signaled the Start of a Big Market Surge

While 2008 was a year that brought the global economy to its knees, 2023 ended up being a strong year for stocks, returning 26.2% from beginning to end. And since the trough of the March 2023 selloff, the S&P 500 has gained a solid 80%, as of this writing.

Still, I’m sure you recall the fear in the air at the time. But we saw the selloff for what it was: a chance to buy at a bargain. In a March 2023 article, I wrote that “the selloff has resulted in deeper CEF discounts—and some nice buying opportunities in our CEF Insider portfolio.”

And in the March 2023 issue of CEF Insider, we made a contrarian move, picking up the finance-focused John Hancock Financial Opportunities Fund (BTO). By the time we sold a little over a year later, in July 2024, BTO had delivered a tidy 24.1% total return. (We’ve since re-added the fund to our portfolio.)

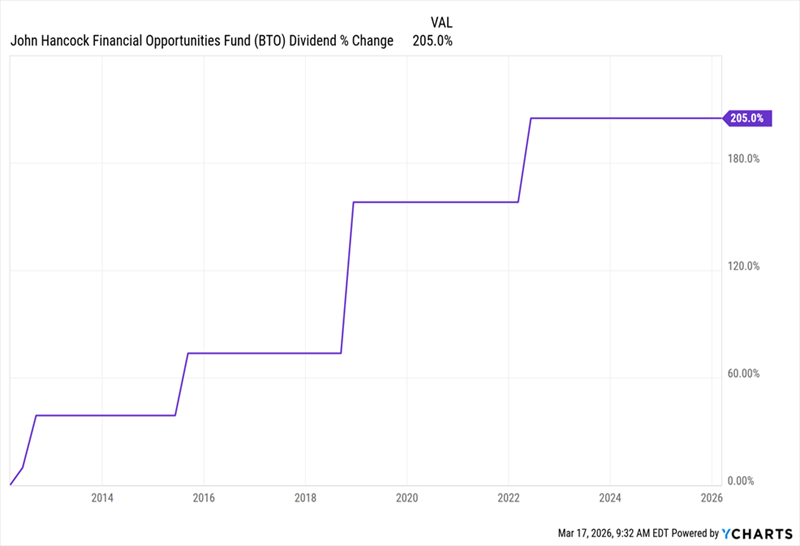

The fund also yielded 8.4% when we bought and has been steadily growing the payout for the last 15 years (the fund yields 7.7% today, due to the gain in its share price):

BTO’s High, and Growing, Payout

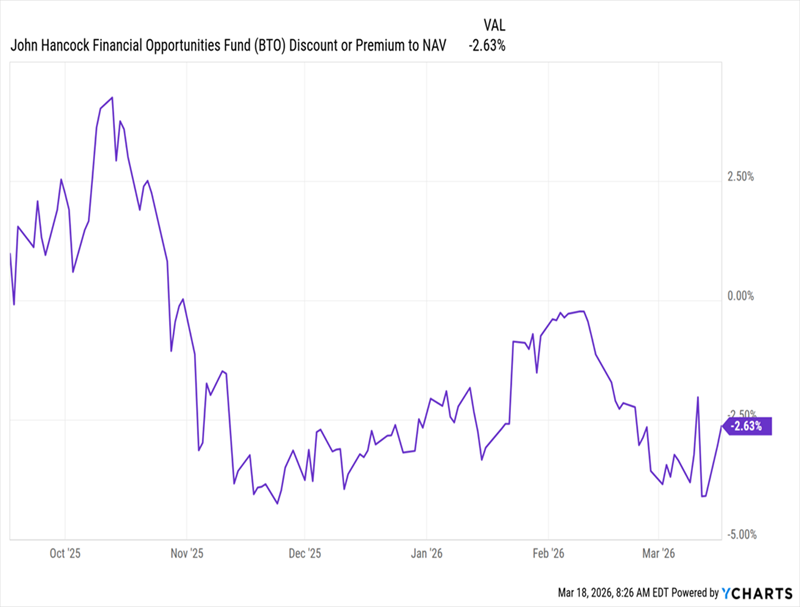

And now, thanks to this year’s volatility, we have an opportunity to buy BTO at a bargain:

BTO Flips From a Premium to a Discount

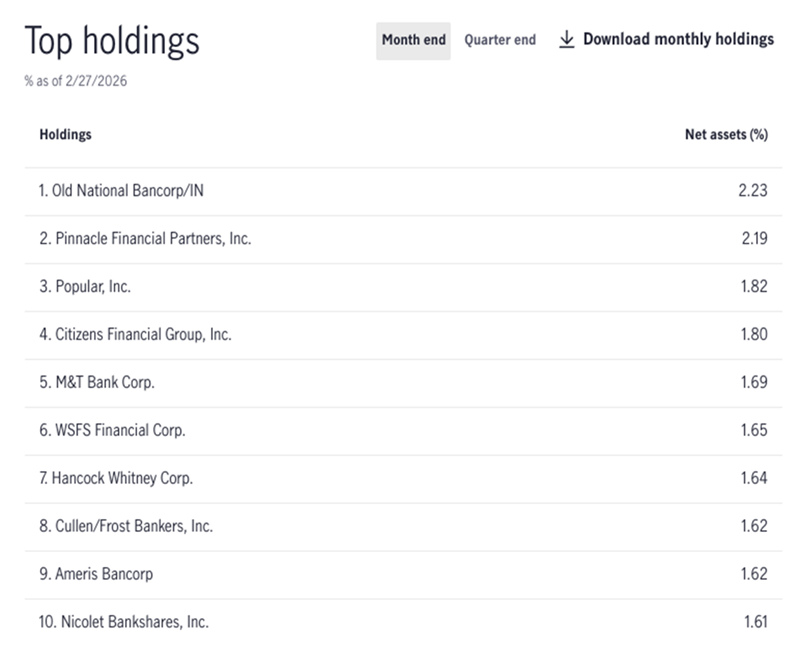

In fact, over the last decade, BTO has had a 3.7% average premium to its net asset value, making this discount to net asset value (NAV) bigger than it looks. Why is this deal in front of us? A hint is in the fund’s portfolio:

Source: John Hancock

As you can see, BTO is focused on regional banks. Old National Bancorp (ONB), Pinnacle Financial Partners (PNFP), Popular (BPOP) and Citizens Financial Group (CFG) are all regional banks that have thrived over the last few years.

That’s driven BTO to strong returns over the long haul, too: 10.7% annualized over the last decade, to be exact. Put another way, every $100,000 invested in BTO in 2016 would be worth around $319,000 as of this writing.

And even following 2008, BTO (shown in green below) performed well:

Source: John Hancock

In the decade following the Great Recession, BTO turned $100,000 into $267,478. That’s a solid positive return, showing that the fund can still deliver profits, even in the wake of the worst financial crisis in a generation.

My Take? This Private-Credit Fiasco Is More Like 2023 Than 2008

Which brings us back to private credit, and whether stocks are on the verge of a pullback due to poor risk management in this largely opaque market.

My take? Most likely, this situation is a tempest in a teapot. Consider first of all the wider context: The private-credit market is about one-sixth the size of the total corporate credit market, and the worst estimates point to private credit generally being marked to market at a 20% discount to current levels.

Second, a diversified fund like BTO is likely to hold up well even in the worst-case scenario: The fund holds 186 assets across a range of banks, insurers and other financial institutions.

A rough estimate suggests that a private-credit pullback could translate into only about a 3.3% hit to BTO’s NAV. I see that as largely priced in, due to the recent widening of BTO’s discount and the fact that this fund has generally traded around a 3.7% premium.

These are the two numbers to key in on here, as they suggest BTO—which has performed strongly over the long haul and the short—is ripe for buying, no matter how this all plays out.

I’m Issuing an Urgent Buy Call on These Four 9.2% Payers, Too

It’s not just BTO—the current market turbulence has widened the discounts on plenty of other CEFs, too. And we’re doubling down, not just on BTO but on 4 other funds yielding a rich 9.2% between them.

I call them “All-Star” funds for the strong long-term runs they’ve put up, not to mention those rich 9.2% payouts, two of which come our way monthly.

There’s no time to waste if you want to grab these 4 funds before their deep discounts slam shut. Click here and I’ll tell you more about them and give you a free Special Report revealing their names and tickers.

Recent Comments