The price-to-earnings (P/E) ratio has long held a lock on investors’ imaginations. So when it jumps to near 30, like it has in the last few weeks, they’re inclined to think stocks are pricey and pull back.

Now is not the time to do that.

Instead, we’re going to do what we always do at times like these: Look to a closed-end fund (CEF) that keeps us invested in stocks but gives us a hedge against a potential pullback. Three hedges, actually:

- The sale of covered call options, which generate extra cash for the fund, supporting the dividend it pays out to us.

- A discount to net asset value (NAV) that actually stands to flip to a premium if market volatility ticks up, and …

- The dividend, which, as mentioned, yields a high 6.8% today.

We’ll dive into this unique play in a sec. First, let’s talk about that “high” P/E, because the truth is, we’re entering a new era where continued strong earnings mean the market is likely to “settle” at a new, higher P/E than we’ve seen throughout history.

Investors who know this will profit. Those who stick with the outdated view of P/E ratios will be stuck on the sidelines as stocks (and equity-focused CEFs!) move higher.

Let’s get into it.

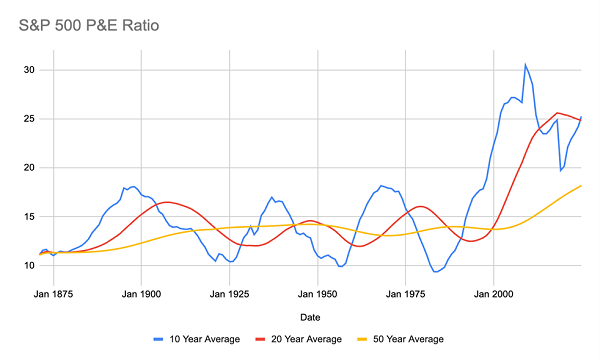

Source: CEF Insider

As you can see above (particularly in the red 20-year average and yellow 50-year average lines), through to the late 20th century, stocks oscillated between a P/E of around 10 when they were “cheap” and 17 or so when they were “expensive.”

Then the pattern broke, in a couple of ways. First, the long-term average P/E jumped (again most visible in the red and yellow longer-term lines), with clear setbacks in the early 2010s, when stocks were overly expensive, and very briefly in 2019, when they were cheap.

Those marked the second “break” here, because those two occasions were actually the opposite of what P/Es of these levels traditionally meant: The “high” P/E of the early 2010s was a great time to buy, and the “low” P/E of 2019 came, of course, just ahead of the pandemic selloff.

The takeaway? The P/E ratio doesn’t matter as much as it used to—at least not if we’re thinking in terms of the next one to five years.

But there’s another, more important, takeaway here, too: We can see that stocks are slowly settling on a new, higher level, which is most clear in the 50-year average line above. Instead of sticking around an 11.5 to 14 range, the average market P/E is climbing, and has been doing so since the late 1990s.

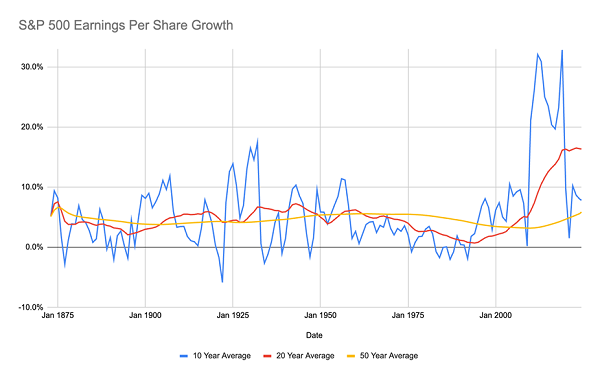

Source: CEF Insider

To see why, we need to zero in on the “E” in P/E ratio: earnings.

I know there’s a lot of noise in the chart above, but the key things to focus on are the red line, or the trailing-20-year average earnings per share (EPS), and the yellow 50-year average. What we see is that average year-over-year growth was rangebound until the 1970s.

Sure, it could vary wildly from year to year, which is why the 10-year average (blue line) is erratic. But over a generation, EPS growth stayed at that 4% range. Things got a bit worse in the 1970s, and this only really started to recover in the 1990s before soaring since. Part of the reason for that is the digitization of the US economy: Tech offers higher margins and faster growth than other sectors.

Now, here’s the thing: If stocks’ average EPS growth is rising over time, the stock market’s P/E ratio needs to settle at a higher level, as well, to fairly price in the higher profit growth. That’s why today’s P/E ratio of around 30 isn’t as alarming as it would have been in the past.

And it’s why, over the long term, holding US stocks is likely to remain profitable, especially with earnings growth on the rise.

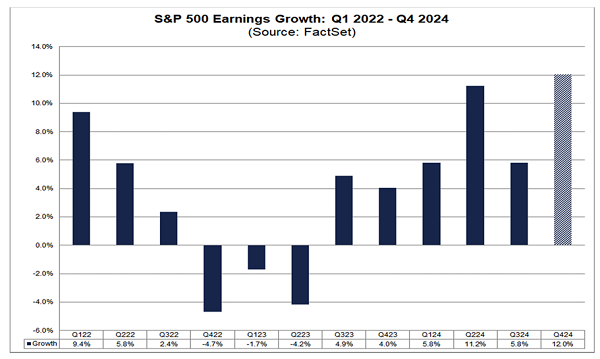

In 2024, we’ve seen stocks’ earnings grow consistently, and if the fourth quarter gives us the 12% growth analysts expect, market gains will likely continue. If not, we might be in for a pullback.

In situations like this, we CEF investors aim to divert a bit of money to something that keeps us exposed to the market but insulates us, too (while keeping our dividends rolling in). This is where a covered-call fund like the Nuveen S&P 500 Dynamic Overwrite Fund (SPXX) comes in.

As the name says, it holds the stocks in the S&P 500—just like an index fund. But one key difference is that SPXX sells call options on that index. These options give the buyer the right to buy the fund’s stocks at a fixed price at a fixed future date. The fund keeps the money it charges these buyers. That helps fund the dividend, which currently yields 6.8%.

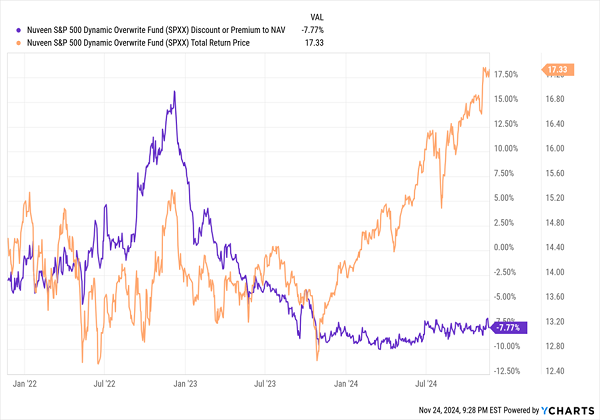

SPXX’s Total Return Gains While It Gets Cheaper

That strategy has helped SPXX’s market price-based return surge in the last year (orange line above) as it rides the waves of the market. But its discount to NAV (in purple) has widened and now sits in a tight range around its current level of 7.8%.

Why the bigger discount compared to 2022, when the fund traded at a premium? Because investors are bullish now. But if sentiment turns bearish (like if earnings growth disappoints), SPXX’s discount will likely flip to a premium as its option-selling “hedge” gains appeal among investors.

At that point, you could sell the SPXX shares you bought at a discount to these buyers at a premium. Until that day, though, SPXX will pay you a 6.8% dividend yield.

It’s Not Just P/E Ratios. Investors Missed the Boat on These 9.6% Dividends, Too

Our look at P/E ratios above shows that, just by doing a bit of digging, you can find an indicator, trend or individual ticker that gives you an edge over other investors.

So it goes with CEFs, which are ridiculously overlooked by the mainstream crowd. There’s simply nothing else out there that gives you the average historical return of the stock market (around 8% or so annualized, depending on the time period you’re looking at) in dividends alone.

And that’s before you factor in any price upside!

But as interest rates fall, I expect more investors to pile into these income wonders. Let’s beat them to it.

We’ll start with the 5 “hidden” CEFs I’m pounding the table on today. They come from across the economy and yield an incredible 9.6% between them. And they sport such big discounts I’m calling for 20% price upside from them, too!

Recent Comments