Today, the 10-year Treasury pays just 2.7%. Put a million bucks in T-Bills, and you’re banking $27,000 per year. Barely above poverty levels!

Hence the appeal of closed-end funds (CEFs), which often pay 8% or better. That’s the difference between a paltry minimum-wage income of $27,000 on a million saved or a respectable $80,000 annually.

And if you’re smart about your CEF purchases, you can even buy them at discounts and snare some price upside to boot!

Unfortunately this rising-rate environment has income seekers scared of CEFs. Many of my readers have asked me if they should bail on our high paying vehicles. The financial media is in their heads, and they’re concerned that their funds are suddenly going to drop in price.

Please, don’t toss yourself into poverty by following this misguided herd!

With the markets in flux, we should review the principles of successful CEF investing. They are more nuanced than classic stock picking, because we’re analyzing managers, strategies and holdings versus simple businesses models. After all, for lazy investors, it’s easier to count on dividends via AT&T’s (T) declining subscriptions than it is to determine how much China exposure the Aberdeen Asia-Pacific Income Fund (FAX) has!

(The answer? Only about 5%. But that bit of extra bit of research will lead you to a secure 8.9% yield, versus a fallible 5.6% for AT&T!)

CEF Rule #1: Be Careful With Price Charts

PIMCO’s Dynamic Income Fund (PDI) has been a great performer since its inception almost five years ago – but you’d never know it from its price chart:

Looks Like Sleepy Gains…

… Until You Add the Payouts Back!

Make sure the chart you’re reading includes dividends paid (so that it reflects total returns).

CEF Rule #2: Demand Alpha

Past performance can be an educational indicator about the quality of the management team and its strategy. PDI has had the benefit of the brightest bond minds on the planet calling the shots (from “Bond King” Bill Gross to current superstar Dan Ivascyn) and it delivered 97% total returns over the last five years, with most of these coming in the form of cash payouts.

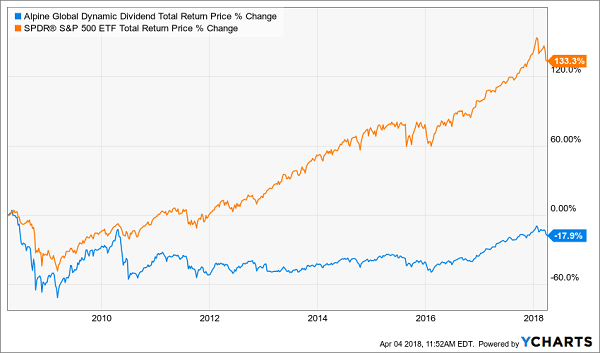

Meanwhile Alpine’s Global Dynamic Dividend Fund (AGD) has delivered the worst of all worlds to dividend investors. It crashed harder than the broader markets in 2008, then provided almost no rebound as stocks themselves bounced back.

Dynamic dividends? Not here – this dog is still down 18% over the last decade!

More Downside, None of the Upside

Don’t be fooled by the siren song of its fat 7.5% current yield. Which brings me to our next point…

CEF Rule #3: Check Every Yield’s Back Story

Some funds pay big distributions that look great – but they’re not sustainable. However they continue to attract new (sucker) investors because they are able to fund their payouts – they just happen to shed their net asset value (NAV) at a similar pace!

For example, here are two more dogs that have grinded sideways or worse over the last three years (even when accounting for dividends paid):

Big Yields, But Lackluster Returns

CEF Rule #4: Know What’s Funding Your Distributions

A closed-end fund can pay you from some combination of:

- Investment income,

- Capital gains, and/or

- Return of capital.

Of the three, investment income is preferable because it’s usually the most reliable. Many CEFs pay monthly distributions, so it’s best if they match up their payouts with steady income streams themselves.

Capital gains from rising bond or stock prices can further boost distributions. But they are at risk of disappearing if the markets turn unfavorably.

Finally, everyone assumes return of capital is bad, because it’s simply shipping your money back to you. But as my colleague, the “CEF professor” Michael Foster, recently wrote, it’s often very good for investors.

What’s more, if the fund trades at a sizeable discount, this can actually be a savvy way to kick start the closing of a discount window. More on this shortly.

CEF Rule #5: Don’t Be Cheap About Fees

Most investors are conditioned by their experience with mutual funds and ETFs to search out the lowest fees, almost to a fault. This makes sense for investment vehicles that are roughly going to perform in-line with the broader market. Lowering your costs minimizes drag.

Closed-ends are a different investment animal, though. On the whole, there are many more dogs than gems. It’s an absolute necessity to find a great manager with a solid track record. Great managers tend to be expensive, of course – but they’re well worth it.

The stated yields you see quoted, by the way, are always net of fees. Your account will never be debited for the fees from any fund you own. They are simply paid by the fund itself from its NAV.

CEF Rule #6: Ignore Short-Term Interest Rates

Many funds are selling at bargain prices today thanks to the headline worry that higher rates hurt CEFs. But that’s just not true.

Libor is tied closely to the Fed funds rate. And the last time the Fed hiked its rate significantly, CEFs did just fine.

In June 2004, Fed chair Alan Greenspan began boosting rates from then-historic lows. Over a two-year period, he increased the federal funds rate from 1% to 5.25%. An earthquake.

How’d CEFs perform? Three prominent funds all outperformed the market during Greenspan’s aforementioned run:

Higher Rates No Problem for Top CEFs 2004-06

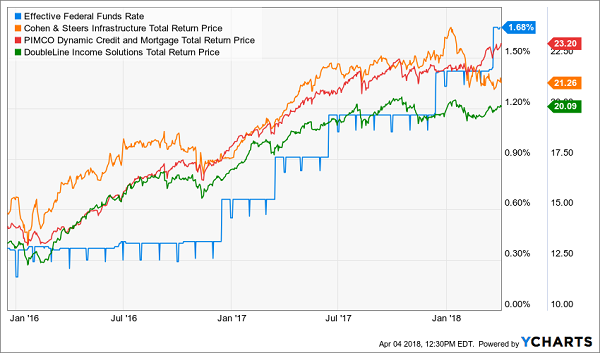

Regular readers will recognize the Greenspan example quite well, because I’ve been using it repeatedly to drive this point home. And I’m glad to share another data point – our own profits from this rate hike cycle!

The chart below illustrates three of my CEF recommendations rolling higher in lockstep with the Fed funds rate (and that rate is the orange line stair stepping from the lower left to the upper right):

This Rate Hike Cycle, Our CEFs Have Rolled Higher

Once again, the best CEFs are gaining value in the face of rate rises.

CEF Rule #7: Demand a Discount

One aspect of the CEF structure lends itself perfectly to contrary-minded investing: fixed pools of shares.

Mutual funds issue more shares whenever they want. But closed-ends have a fixed share count, with their funds trading like stocks. As a result, from time to time a fund will fall out of favor and find its shares trading at a discount to its NAV.

This is basically “free money” because these underlying assets are constantly marked to market. If a fund trades at a 10% discount, management could theoretically liquidate the fund and cash out everyone at $1.10 on the dollar immediately. Or it can buy back its own shares to close the discount window (and boost the share price).

A discount is a great start, but do make sure that management has a plan to close that window!

CEF Rule #8: When Possible, Buy Along Insiders

It’s rare to see any fixed income manager put his or her own money on the line at all, unfortunately. According to a recent Barron’s article, nearly half of all closed-end funds have no insider ownership whatsoever.

Why would we want to own any of them, if the managers don’t?

The 3 Best Closed-End Funds to Bankroll Your Retirement

Closed-end funds are a cornerstone of my 8% “no withdrawal” retirement strategy, which lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well that’s not exactly right.

Their principal is more than 100% intact thanks to price gains like these! Which means principal is actually 110% intact after year 1, and so on.

To do this, I seek out closed-end funds that:

- Pay 8% or better…

- Have well funded distributions…

- Trade at meaningful discounts to their NAV…

- And know how to make their shareholders money.

And I talk to management, because online research isn’t enough. I also track insider buying to make sure these guys have real skin in the game.

Today I like three “blue chip” closed-end funds as best income buys. And wait ‘til you see their yields! These “slam dunk” income plays pay 8.2%, 9.9% and even 10.1% dividends.

Plus, they trade at 10 to 15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and I’ll explain more about my no-withdrawal approach – plus I’ll share the names, tickers and buy prices of my 3 favorite closed-end funds for 8.2%, 9.9% and 10.1% yields.

Recent Comments