Are higher interest rates and lower bond prices a sure thing for 2025? Mainstream financial pundits say yes.

Which gives us thoughtful contrarians pause. Their narrative against bonds is assumed. When this happens, markets tend to move in the opposite direction of conventional wisdom.

Which means we should bet with bonds. At least in the near term to start the new year. Let’s watch bonds rally and surprise everyone except for us. The “Trump is bad for bonds” trade may eventually be correct, but my hunch again is that this “surefire” call is early.

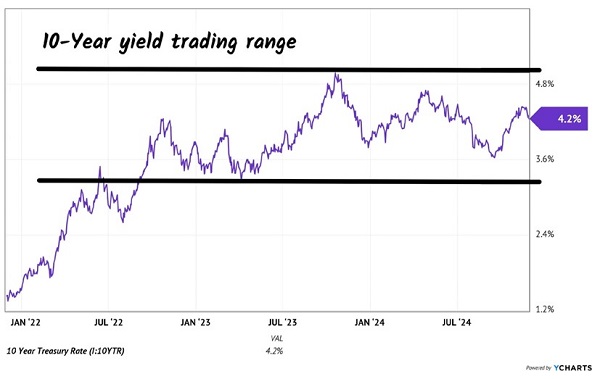

For all the recent commotion, the 10-year Treasury yield bounces between 3.3% and 5%, with an even narrower 3.6% to 4.7% range recently.

At 4.2%, there isn’t much to see here. We do better turning off the “news” (or what passes for it these days) and following a simple strategy. Buy bonds when rates rise until further notice:

Trading Range for the 10-Year Yield

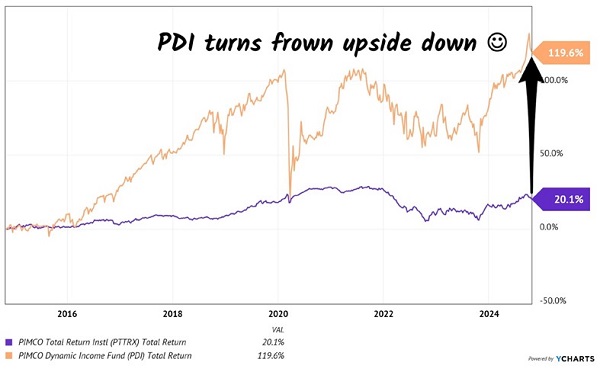

Select PIMCO funds are bargain buys on rate worries. Let’s just make sure we are talking about the famed bond shop’s closed-end funds (CEFs) rather than its vanilla PIMCO Total Return Fund!

Total Return made Gross famous and got him crowned “Bond King.” But over the past 10 years, Total Return didn’t. It eked out an embarrassingly tiny 20.1%–an unacceptable—nay, embarrassing!—2% annualized. Yikes. Not even a court jester there.

The King’s successor, Dan “The Beast” Ivascyn, was busy bestowing royal riches on other PIMCO CEFs. Poppin’ over the same timeframe, Contrarian Income Report-owned PIMCO Dynamic Income Fund (PDI) showered 119.6%—six times Total Return:

Bond Returns Fit for a King

PDI yields 13.7% as I write. Who cares if the 10-year touches 5% when you’re holding on to this fat dividend?

PIMCO archrival DoubleLine manages two monthly dividend CEFs in the same rarified-yield air. “Bond God” Jeffrey Gundlach had a famous contentious conversation with Gross in 2014 about potentially partnering up.

It ended when Gross inferred that with “only” $55 billion in assets, Gundlach could never be king!

“That’s no kingdom,” Gross quipped. “That’s like Latvia or Estonia.”

A Baltic bond diss—ouch. Needless to say, Gross and Gundlach never partnered. After this exchange, they went back to disliking each other. So far, permanently.

Their tiff is our gain—more monthly tickers to buy. Gundlach finds alpha for his DoubleLine Yield Opportunities Fund (DLY) below the investment grade or not rated bond “lines in the sand.” This would make us nervous were Gundlach not our assigned shopper.

“Shopper?” OK. There are great deals to be had sub-investment grade because, for example, pensions—the biggest buyers of bonds—aren’t allowed to own this paper. Issuers of these bonds approach Gundlach first to buy them (as business sellers often start with Buffett).

So, we benefit from not only deals others don’t see, but also the ones he believes offer the best reward versus risk. We can trust the picks that Gundlach puts in this CEF cart. It’s where the values are in Bondland, and cookie cutter ETFs and mutual funds are not flexible enough to take advantage of these deals.

We can—and do. DLY yields 8.5% today while sister fund DoubleLine Income Solutions (DSL) dishes 10.2%.

Munis, meanwhile, are also attractive here. Industry blue-chip Nuveen funds have pulled back with the bond market. Boy, do they pay! With a 7.3% yield before we consider the tax savings, Nuveen Municipal Credit Income (NZF) is a nifty play.

Finally FS Credit Opportunities (FSCO) is a unique CEF high-yield play. FSCO has been around for 10+ years but only traded publicly for the last two as a closed-end fund (CEF).

CEF investors loathe newness. So, FSCO trades at a 5% discount to its net asset value (NAV) despite its generous 10.7% yield paid monthly.

The team extends private market loans, where FS can dictate favorable terms. The recent nomination of Wall Street-approved Scott Bessent as the likely next Treasury secretary seems to be a nod not only to the financial sector but also to the small businesses that borrow from FSCO.

I asked FS Investments’ Joseph Montelione if his firm has adjusted their strategy since the election to account for more M&A:

“We agree that the M&A outlook is a bit more optimistic under a Trump administration. The consensus is that the new administration will be a lot friendlier from a regulatory and taxation perspective, which should spur a pickup in deal flow,” Montelione replied.

“The consensus amongst industry leaders and peers in the industry is that companies have been in wait and see mode for over the last few years. We are definitely observing a bit of a mentality shift today, now that the election is behind us.”

Bessent and Trump 2.0 mean more likely price upside for this 10.7% dividend. For those who have the foresight and courage to buy the bond bargains today, that is.

These are just a few of my favorite monthly payers for 2025. Believe it or not I have a veritable laundry list of 8%+ yielding monthly payers with 10%+ upside for 2025. These funds are ready to roll for Trump 2.0—don’t miss out on these dynamic dividends! Click here to access my full 8%+ monthly payers for 2025 research.

Recent Comments