We’re now well on our way to Trump 2.0, and I’m getting a lot of questions from readers about where things head from here.

I see the new administration as overall bullish for stocks. But the truth is, fortunes will be made in the next four years and, sadly, retirements will be lost.

My job is to keep you on the right side of the financial markets. One thing I can say is that the next four years will be challenging for two kinds of investors:

- Buy-and-hold (or as I like to call them, “buy-and-hope”) types, and …

- Those who sit in index funds like the SPDR S&P 500 ETF Trust (SPY).

Those strategies won’t cut it in the next four years, which will be a stock picker’s market. Moving into, and out of, particular stocks in a timely way will be key.

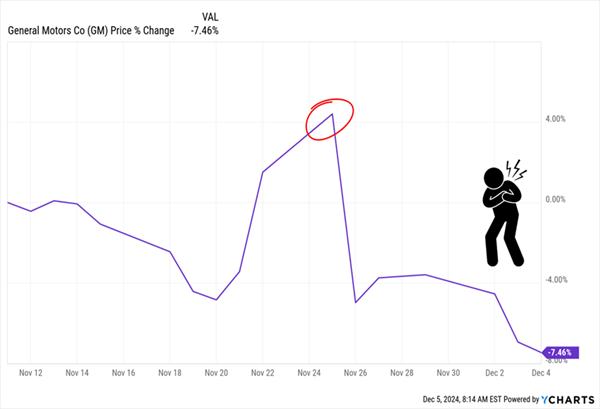

Just look at what investors who got caught sitting in General Motors (GM)—which is as tariff-exposed as they come—have dealt with since the president-elect announced potential new tariffs on Canada and Mexico on November 25.

“Buy and Holders” Get Run Over

In our November 26 article, we discussed other stocks to sell (or avoid) during Trump 2.0, too. Like Mattel (MAT) and Hasbro (HAS), both of which still make a lot of their toys and games in China, leaving them vulnerable to tariffs.

But there are plenty of winners-in-the-making, too. Which brings me to defense stocks—one defense stock in particular.

Our Contrarian Defense Play Starts With … AI?

When it comes to defense stocks, one question leaps out about Trump 2.0: If Trump does cut a deal with Russia to end its war on Ukraine—or with China to calm tensions in the Pacific—is the associated “peace dividend” bearish for defense stocks?

At large, perhaps, but if it does, its main impact will be on defense firms that haven’t diversified away from what I’ll call physical weapons.

Consider, for example, Lockheed Martin (LMT), which leans on systems like the F-35 Joint Strike Fighter, missiles, helicopters, such as the Blackhawk, and space systems, for the bulk of its revenue.

Those products will stay in high demand as countries around the world keep boosting defense spending. And they’re likely to escape import tariffs if trade tensions do ramp up in the months ahead. However, while Lockheed does have strong prospects, defense spending does tend to ebb and flow in the long run, with the rhythm of world events.

But there is one thing that will continue to be a threat no matter what’s happening geopolitically: cyberattacks.

Cybersecurity and information technology (IT) upgrades are the sales straw that stirs the drink at General Dynamics (GD). In the third quarter, the company pulled 29% of its earnings from its technology division.

That business’s gross margins jumped to 9.7% in the latest quarter from 9.5% a year ago. That helped it chip in the highest operating earnings of any of the company’s other divisions (which include aerospace, marine systems and combat systems), at $326 million.

GD Is a Tech Stock in Disguise

In February, General Dynamics Information Technology (GDIT) was awarded a $922-million contract to upgrade the US Central Command’s (CENTCOM) IT infrastructure. This follows a big year, 2023, that included $2-billion GDIT contract wins.

To be sure, the company’s physical weapons—like the Abrams tank, Stryker combat vehicle and nuclear subs—are why GD finds itself in the same bucket as firms like Lockheed, Boeing (BA) and Northrop Grumman (NOC), not cybersecurity stocks like CrowdStrike Holdings (CRWD), Fortinet (FTNT) and Palo Alto Networks (PANW).

But at my Hidden Yields service, we mainly hold the stock because of its overlooked value as a cybersecurity play. We also like it because it’s a backdoor play on AI automation at the federal level.

AI plays a central role in GDIT’s strategy—it has deployed a Luna AI system that uses machine learning to draw insights from large reams of data. Luna is designed specifically for government and defense applications.

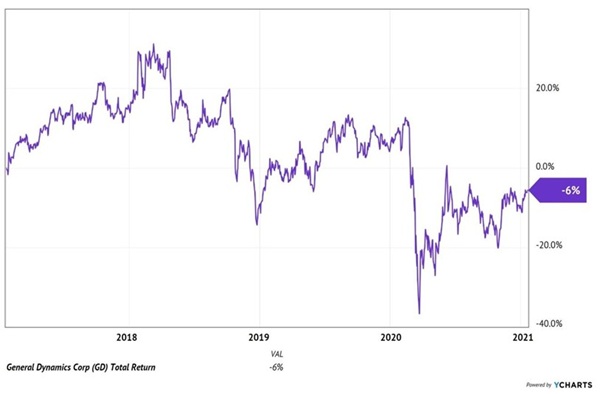

GD flatlined during Trump 1.0, but we have higher expectations this time around given the AI angle.

Trump 1.0: GD Flatlined

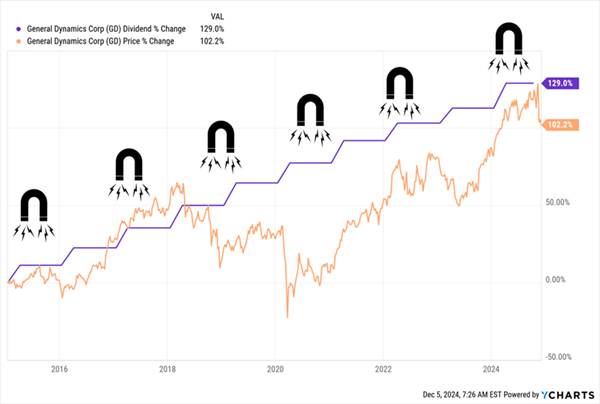

What’s more, GD’s “Dividend Magnet”—or the tendency for a stock to track its dividend higher over time—is also telling us that the stock is undervalued: As you can see below, the shares have fallen a bit behind, setting us up for future “snap back” upside:

GD’s Payout Sets the Mark for Price Gains

The drop you see on the right side above is due to an overdone reaction to the company’s Q3 earnings, which did come up short of expectations, even though EPS jumped 10.2% year over year.

That’s our opportunity. As is another source of hidden value: GD’s outsized order backlog, with a total estimated contract value of $137.6 billion as of the end of Q3.

The Dividend Magnet: Our Roadmap to Surging “Trump 2.0” Profits

One thing has held true no matter who is in office: A rising dividend is the No. 1 (and 2 and 3!) driver of share prices.

We saw it above with GD. And I can show you chart after chart after chart of how soaring dividends have delivered big price gains for us in the past, too.

With that in mind, I’ve zeroed in on 5 stocks I see as the best plays for surging payout—and share-price—growth through 2025 and beyond. I want to share them with you now, so you can grab them before their share prices “snap back” to their payout growth.

Recent Comments