Most vanilla investors limit their retirement income ideas to the exchange-traded funds (ETFs) advertised on TV.

Don’t do it!

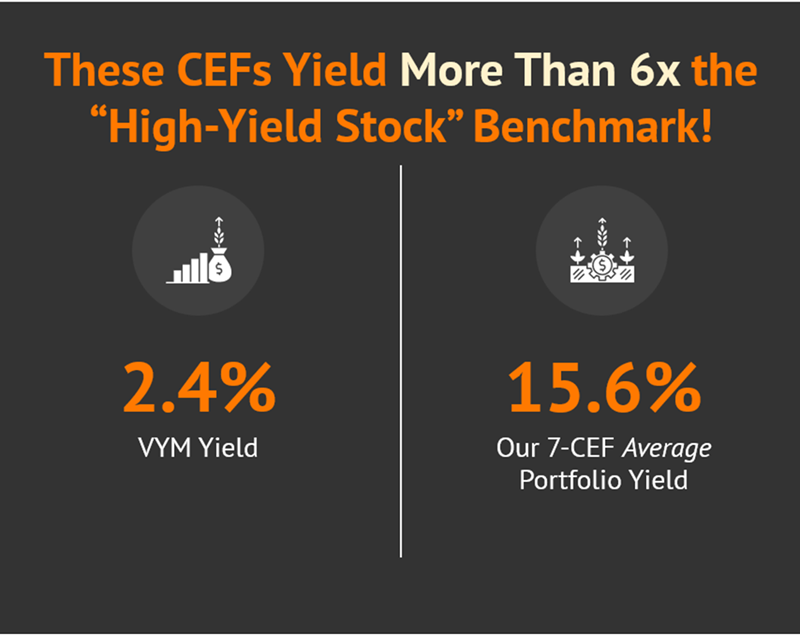

These lame mainstream ETFs tend to yield 1% or 2%. That is only enough income for retirement if we are talking about a $10 million nest egg.

There are better buys beneath the popular surface. And they will fund retirements on far more reasonable savings figures. For example, we’ll discuss funds today that dish dividends of 9%, 10%, even 11%.

This is $55,000 in annual income on a $500k investment. Now we’re talking.

And these funds feature active management. Ironically, they often boast better caretakers than the large ETFs, which are highly automated and contain more marketing sizzle than alpha.

We’ll gladly buy these “CEFs” instead of “ETFs” to collect the generous payouts and take advantage of the thoughtful portfolio constructions.

CEFs is short for “closed-end funds,” and while they’re not nearly as well-known as mutual funds and ETFs, they boast certain characteristics that give them an edge over both, including:

- Regularly trading at discounts to their net asset value (NAV)

- Leveraging debt to double down on their highest-conviction picks

- Trading options to generate cash

- Owning privately held investments

And let’s be honest, why do we really love CEFs? Their sky-high yields. Let’s consider the seven-CEF portfolio we’ll discuss today, which pays $78,000 on a half-million investment. This is many times more than what we could get from traditional “high-yield” ETFs!

But like with traditional investment funds, we need to do our homework before buying closed-end funds. So let’s make sure these 9.3% to 33.5% paying CEFs are yield opportunities, not yield traps.

I’ll start with a pair of bond funds from the world’s top asset manager: BlackRock (BLK).

I’ve called the BlackRock Core Bond Fund (BHK, 9.3% distribution rate) a “north-south football” type of fund. Nothing fancy here. We get big doses of investment-grade credit, U.S. government debt, securitized debt, agency mortgages. Credit quality is generally high, though about a quarter of the fund is “junk”-rated. And while it often trades at NAV, it’s currently priced 4% below as I write this.

This is an extremely long-dated portfolio with a weighted average life to maturity of more than 20 years. No wonder, then, that the Fed’s easing hasn’t done much for BHK over the past couple of years.

But it’s positioned right if we get a downturn in long rates. Just note that high leverage of 33% makes BHK less of a “core” holding and more of a boom-or-bust play.

BlackRock’s Core Fund Swings for the Fences, For Better or Worse

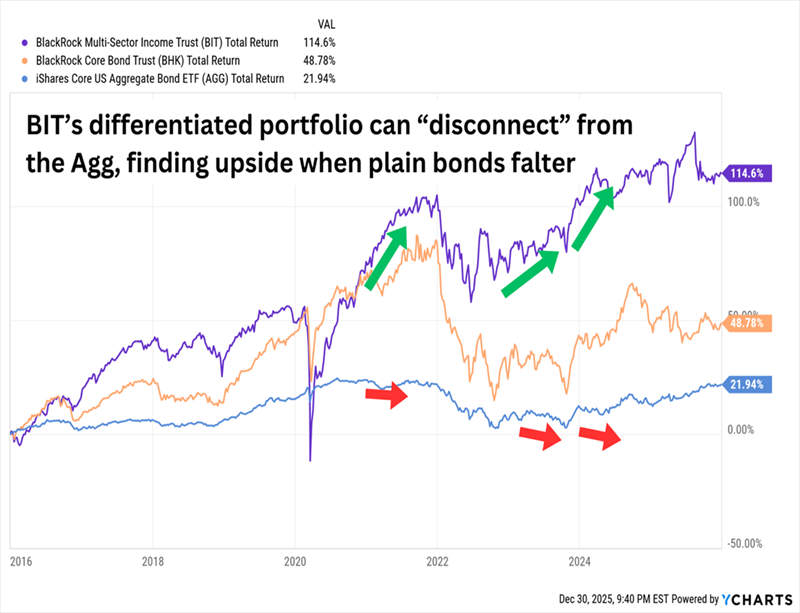

The BlackRock Multi-Sector Income Trust (BIT, 11.3% distribution rate), despite being a “junkier” debt portfolio, is calmer in a number of ways.

Half of BIT’s assets are invested in high-yield corporates, and most of the rest is in securitized debt, agencies and developed-market sovereigns. But the average maturity of 13 years, while not short, is far shorter than BHK. Leverage is high at 29%, so it won’t be the serene ride of a plain-vanilla ETF—but it has been much less volatile than BHK and more productive over the longer-term.

BIT tends to stick close to NAV, too, but it’s currently trading at 95 cents on the dollar. Income is extremely consistent, too—it’s a managed distribution that has remained level (with the exception of one raise) since 2013 inception.

Next up, let’s explore some equity-focused CEFs.

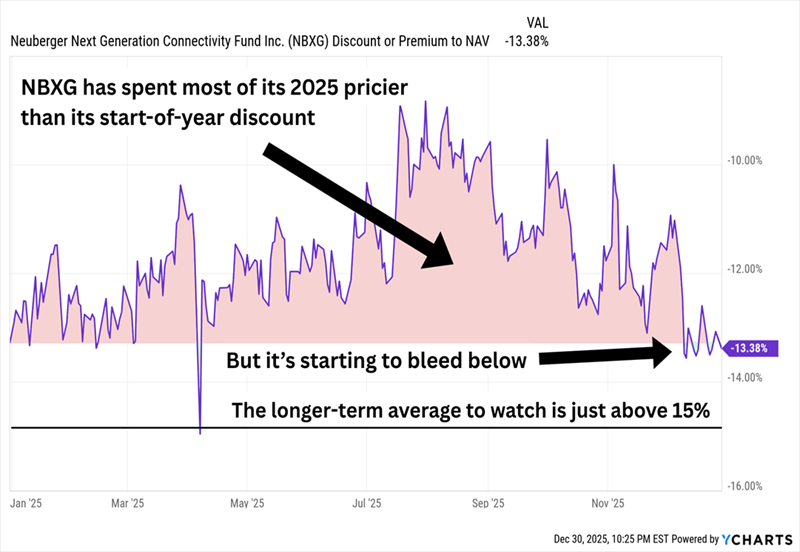

The Neuberger Berman Next Generation Connectivity Fund (NBXG, 9.9% distribution rate) delivers a nearly double-digit distribution, paid monthly, from a few dozen technology, communications, and consumer stocks.

This is a play on next-generation connectivity, buying stocks that benefit from 5G mobile networks. But it’s hard not to look at its top holdings and see a standard, unimaginative “AI whatever” portfolio, given holdings like Meta Platforms (META), Nvidia (NVDA), Microsoft (MSFT), and Taiwan Semiconductor (TSM).

Investors are not impressed with the lack of creativity. NBXG trades at a 13% discount to its NAV, which means shares are trading hands for just 87 cents on the dollar:

NBXG’s 13% Discount to NAV

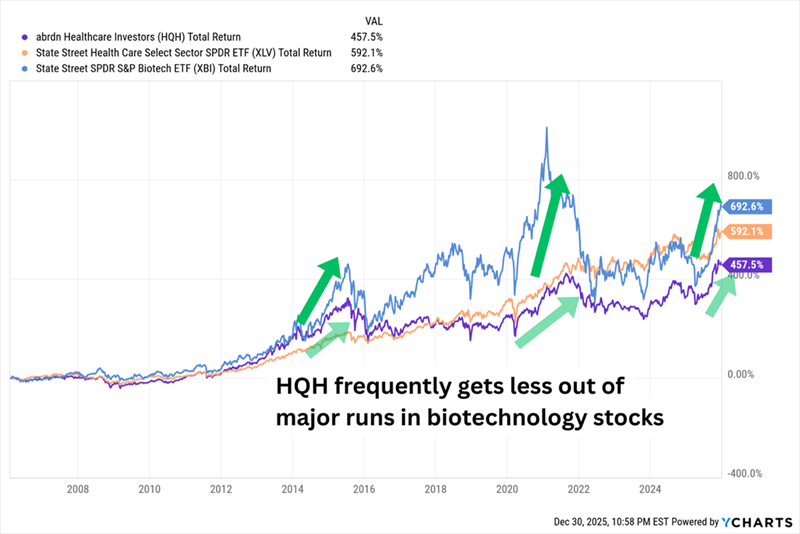

From a 5G poser we move to healthcare and abrdn Healthcare Investors (HQH, 12.1% distribution rate). The name says healthcare but it is basically to a biotech fund. Two-thirds of assets belong to biotech; the rest is spread across pharmaceuticals, healthcare equipment, life sciences tools and services, managed healthcare, and more.

HQH doesn’t use any leverage—the high distribution rate is part of a managed distribution policy that currently is set to pay 12% across the 12-month period beginning with the distribution payable June 2025. These holdings are low yield stocks, however—so where does this dividend come from? It is funded by returns of capital and income from selling (“writing”) covered calls on holdings.

In this scenario, the underlying stocks had better go up. Lately they have but the overall result, unfortunately, is something that has less “boom potential” than pure biotech:

HQH Underperforms Biotech to the Upside

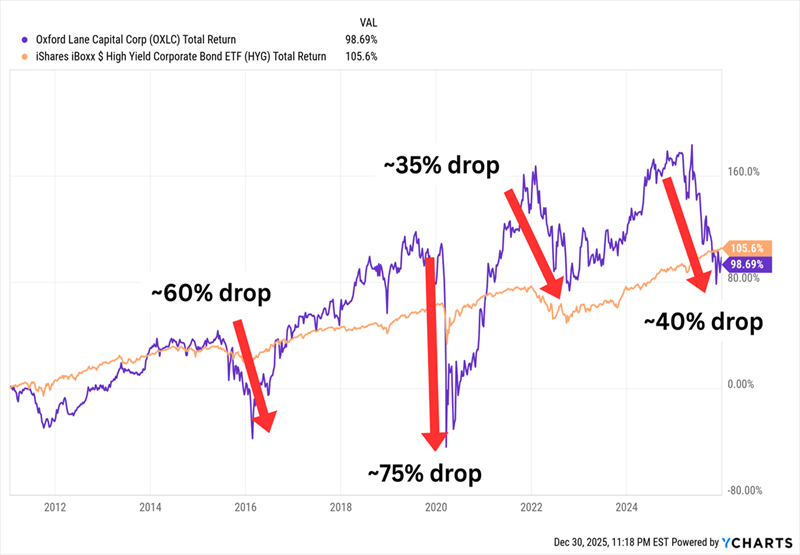

Oxford Lane (OXLC, 33.5% distribution rate) is a CEF that invests primarily in debt and equity tranches of collateralized loan obligation (CLO) vehicles. CLOs are like mortgage-backed securities (MBSs) in that they’re pooled investments; but rather than pooled mortgages, CLOs typically are pooled corporate loans.

CLO equity in specific can be dangerous because it sits at the bottom of the “waterfall.” Cash flows down, first to the senior-most debt, then down to unsecured and subordinated debt, and CLO equity sits at the bottom. Basically, CLO equity only gets paid once all CLO debt gets paid—and thus CLO feels the pain before any other part of the “waterfall.” And that pain can be debilitating:

This 33% Distribution Might Just Be a Siren’s Song

Take OXLC as a warning: CLOs are extremely opaque investments that we can’t even get sufficient information about, and that the average investor will struggle to even understand. And that makes OXLC—even with its mighty distribution rate well above 30%—a blind gamble, not an informed investment.

Besides: As we can see over OXLC’s life, we’re risking a lot of volatility just to get a total return similar to what we could get from a basic junk fund.

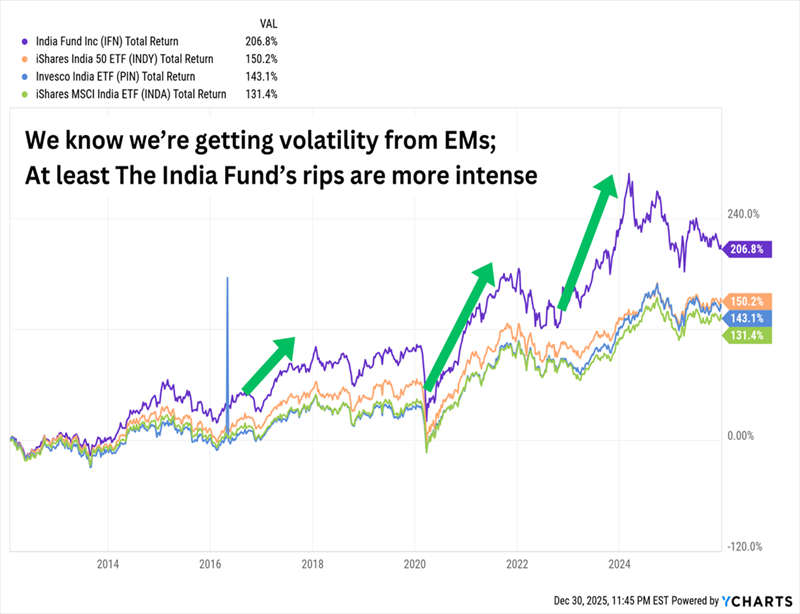

The India Fund (IFN, 16.1% distribution rate) is a better brand of income spice.

IFN owns about 50 predominantly large-cap Indian equities, led by financials HDFC Bank (HDB) and ICICI Bank (IBN) that are blue-chip enough to trade on the NYSE.

The India Fund is poised to take advantage of strength in Indian stocks in 2026. They underperformed last year—so they are due! When this market “goes” IFN captures the upside better than its unflavored ETF competitors:

Head and Shoulders Above the ETF Competition

IFN is trading at a nearly 8% discount to NAV. So, it can be bought for 92 cents on the dollar while other India ETFs fetch the standard 100.

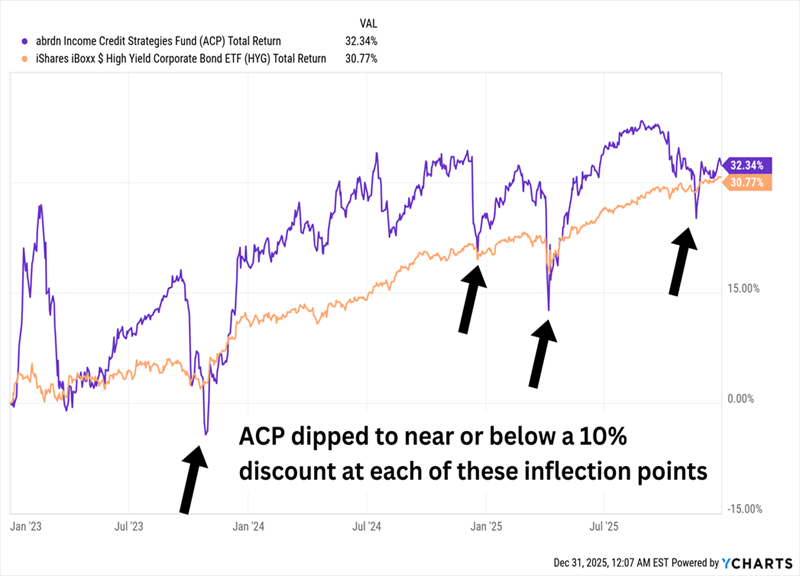

Another Aberdeen Investments product, abrdn Income Credit Strategies Fund (ACP, 17.1% distribution rate), manages to squeeze a high-teens yield out of global corporate junk.

ACP owns a little more than 150 debt issues from across the globe. The portfolio is concentrated in U.K. and U.S. debt, with the rest splashed across a variety of developed and emerging markets. Three-quarters of the bonds are short-term (0-5 years) in nature, with most of the rest between 5-10 years. And it’s plenty junky, with B-graded bonds at nearly two-thirds of assets.

Toss in roughly 30% debt leverage, and we get the kind of ride we’d expect.

But Despite Its Mid Performance, ACP Can Be Useful

The chart above shows that if ACP gets cheap enough, the market tends to react—violently. It’s not there now (the fund trades at a 7% discount), but this could be a target for our trading portfolios.

This Growing 11% Dividend Is Our Top Buy for 2026

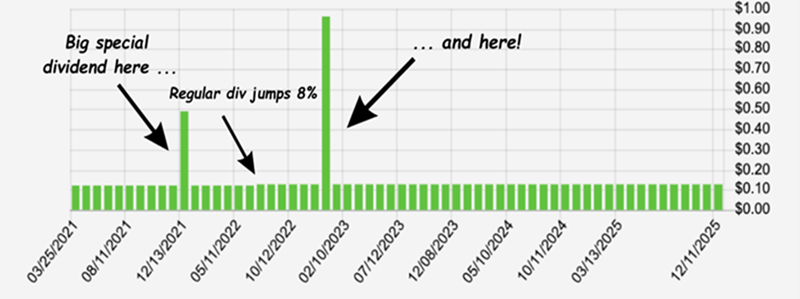

One of my favorite picks in our portfolio is the 11%-paying fund I think all investors—no matter where they are in life—MUST own.

And right now, with 2026 about to dawn, is the perfect time to buy it. As volatility picks up heading into the new year (as I expect), this solid, and growing, 11% divvie will be something to be truly thankful for.

Check out the dividend history: This fund’s monthly payout hasn’t just held steady—it’s grown, and its shareholders have pocketed periodic special dividends, too!

This 11% Payday Is the Real Deal

It’s also run by one of the best managers in the bond business—he’s been recognized as the top talent in the field on multiple occasions. And because this fund is actively managed, it can drop in and hoover up sudden bond discounts that index funds simply aren’t built to identify and snare.

That’s how this fund not only pays an 11% dividend, but can grow it, too!

All of this is why I see this “battleship” fund as a must-buy for all income investors, especially as we head into an uncertain new year.

I’m ready to share my complete research on this fund with you now. Click here and I’ll introduce you to this powerful 11% payer and give you a free Special Report revealing its name and ticker.

Recent Comments