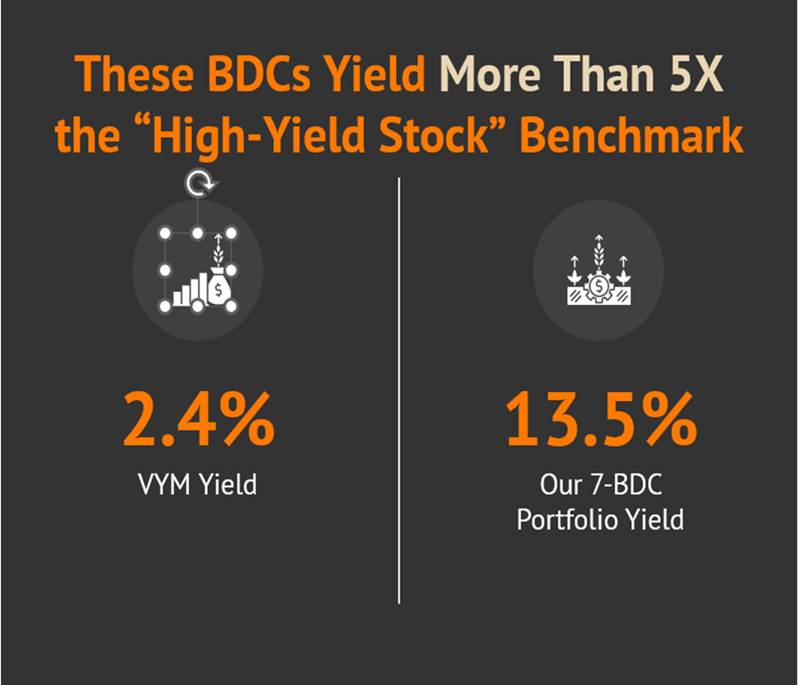

The manic market has been dumping business development companies (BDCs) left and right. Let’s talk about a seven-stock BDC portfolio (yielding 13.5%!) that is poised to bounce back when sanity returns.

BDCs, which lend money to small businesses, are on the “outs” with the Wall Street suits after countless soft jobs reports. The spreadsheet jockeys fret about an unemployment-induced economic slowdown and miss the real story: small businesses are making more money than ever thanks to AI.

Here is what’s actually happening in the Main Street economy:

- Employers—especially nimble small business owners—are implementing AI to streamline and even run their operations.

- With AI tools, fewer humans are needed.

- So, we are seeing soft jobs reports as companies rationally prioritize automation over human hiring.

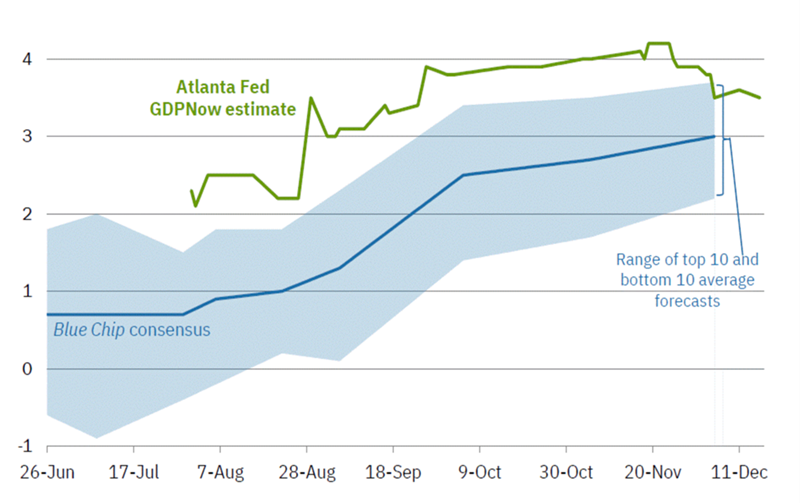

Small business profits are popping. While the unemployment numbers scream slowdown, the actual economy is booming. Check out the Atlanta Fed GDPNow’s most recent estimate—it’s solidly over 3%!

Atlanta Fed Says Economy is Cookin’

That’s no recession—it’s an efficiency boom! And a tailwind for this 13.5% portfolio:

Why not just buy any BDC fund?

It’s a competitive industry—one that creates more individual losers than winners. Buying a fund guarantees we own dozens of those losers.

We’re better off picking “the right” BDCs right now for the current interest-rate environment. BDCs tend to deal heavily in floating-rate loans. When the Fed cuts its target interest rate, it limits what BDCs can charge on those floating-rate loans, which lowers earnings.

But lower rates also bring lower financing costs for small businesses. This increases demand for new loans. Good for the BDC business. We’ll keep these forces in mind as we review seven BDCs paying us between 9.4% and 19.6%.

Sixth Street Specialty Lending (TSLX, 9.4% yield) is a standard-fare BDC. It prefers to invest in companies of between $50 million and $1 billion in enterprise value that generate between $10 million and $250 million in annual EBITDA (earnings before interest, taxes, depreciation, and amortization).

TSLX is pragmatic; it has an idea for its optimal deal partner, sure, but it also understands that they all can’t be gems. It’s pretty transparent about this fact, too, as we can see from this breakdown of some of its portfolio companies.

Sixth Street Isn’t Afraid of a Challenge

Source: Sixth Street Specialty Lending Equity Investor Presentation, December 2025

That portfolio is growing. While TSLX has hovered around 110 to 115 companies for the past few quarters, that number jumped to 145 as of Q3—the vast majority of which were structured credit investments that were smaller than the company’s typical deal size.

Sixth Street is also typical in that it primarily deals in first-lien debt (90%), most of which (96%) is floating-rate in nature. TSLX will feel the pinch as the Fed continues cutting rates.

But it’s also well-positioned to power through the pain. Sixth Street has frequently outpaced net investment income (NII) estimates, produced some of the best returns, and more-than-adequately covered the dividend. That dividend is a regular-plus-supplemental model, which has become increasingly popular among BDCs given rate uncertainty. Regular dividends account for most (8.4 points) of TSLX’s yield, with specials the remaining 1 point.

Sixth Street has long been one of the BDC industry’s best-run companies, and that shouldn’t change much despite a shake-up at the top. Current CEO Joshua Easterly will step down as CEO effective Dec. 31, 2025, to be replaced by Bo Stanley, who is currently serving as co-CEO. But Easterly will remain chairman of the board and continue to serve on TSLX’s investment committees.

Unfortunately, the stock is expensive. Sixth Street has long been one of the BDC industry’s most expensive companies, too. It currently trades at a whopping 28% premium to net asset value (NAV).

Gladstone Investment (GAIN, 10.8% yield) dishes a double-digit yield and a monthly dividend.

This BDC takes on lower-middle-market companies that generate EBITDA of between $4 million to $15 million annually, favoring firms with a proven business model, stable cash flows and minimal market or technology risk.

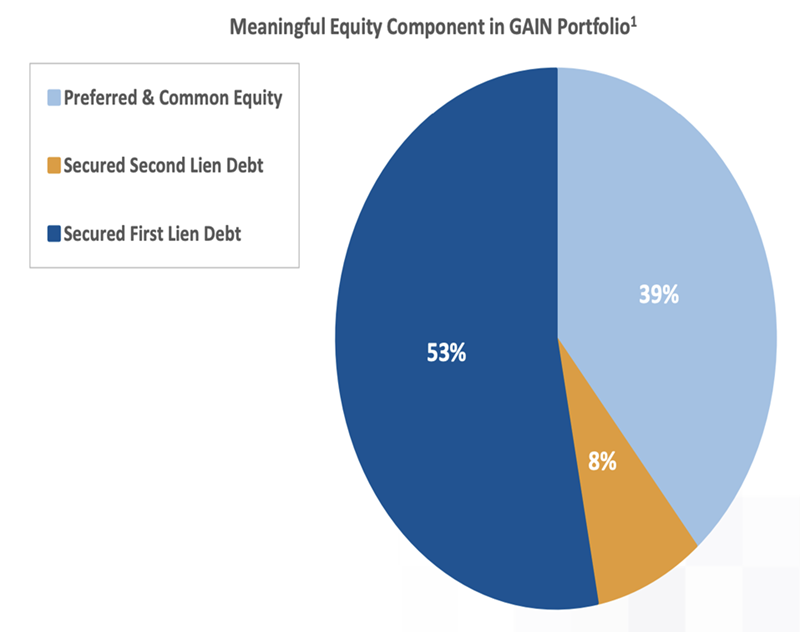

It’s an outlier in a couple of ways: a small portfolio, for one, at just 28 portfolio companies, but also a much bigger hunger for equity than the average BDC. Gladstone points out that BDCs traditionally have equity exposure of 5% to 10%.

GAIN’s Equity Exposure Is 4x the Top of That Range

Source: Gladstone Investment Quarterly Overview, September 2025

Gladstone is less exposed to interest-rate moves. This supports GAIN’s “buyout” strategy. Gladstone Investment typically provides most (if not all) of the debt capital along with a majority of the equity capital. Its debt investments allow it to pay out a still-high regular dividend, but then it also pays out supplemental distributions when they realize gains on equity investments.

Those supplementals make up a large portion (about 3.8 points) of the yield, and they’re awfully variable. Gladstone Investment paid out $1.48 per share across five supplemental distributions in 2023, but then just 70 cents across 1 extra payment in 2024, and 54 cents in a single supplemental in 2025.

Recently, GAIN has been among the top BDCs we can buy. And yet, its valuation remains reasonable—the stock trades at a 3% premium to NAV.

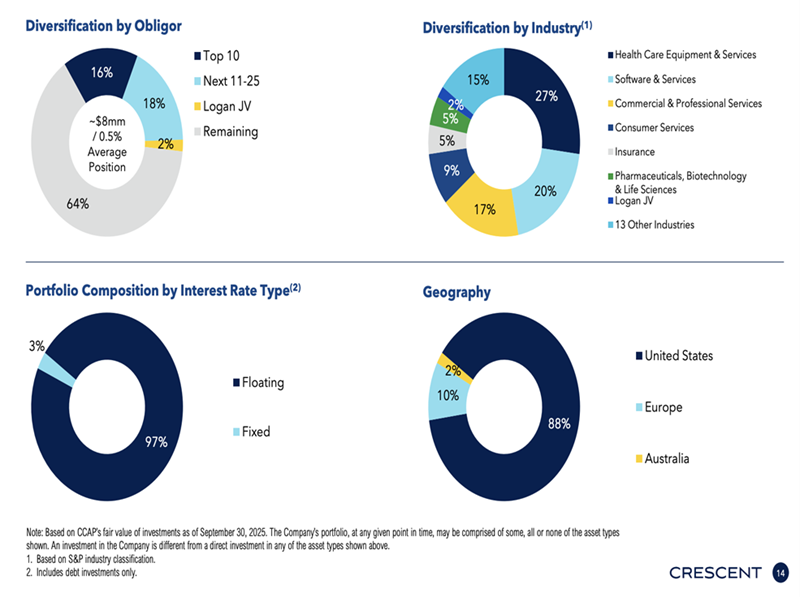

Crescent Capital BDC (CCAP, 12.3% yield), like many other BDCs, is paired with (and enjoys the resources of) a larger investment company—in this case, below-investment-grade credit specialist Crescent Capital Group. Its wide 187-company portfolio, which boasts a median annual EBITDA of about $29 million, spans 18 industries. We also get double-digit exposure to international companies (mostly Europe with a little Australia). It’s a diverse portfolio—but one that’s easily affected by Fed rate changes given that its deal mix is 90% first lien and 95% debt overall.

And Virtually All of That Is Floating-Rate

Source: Crescent Capital BDC Q3 2025 Quarterly Earnings Presentation

CEO Jason Breaux acknowledged the danger in the company’s most recent earnings conference call: “Looking ahead, we anticipate that a lower base rate environment may gradually reduce portfolio yields and place some pressure on net investment income.” But when pressed on the dividend, he added “I think for the immediate near term, we do believe that we are going to cover our base dividend with NII.”

But it still merits a close watch: A few analysts’ earnings estimates for 2026 fall below the dividend. That would help explain the stock’s current 23% discount to NAV, as would its 15% loss including dividends year-to-date.

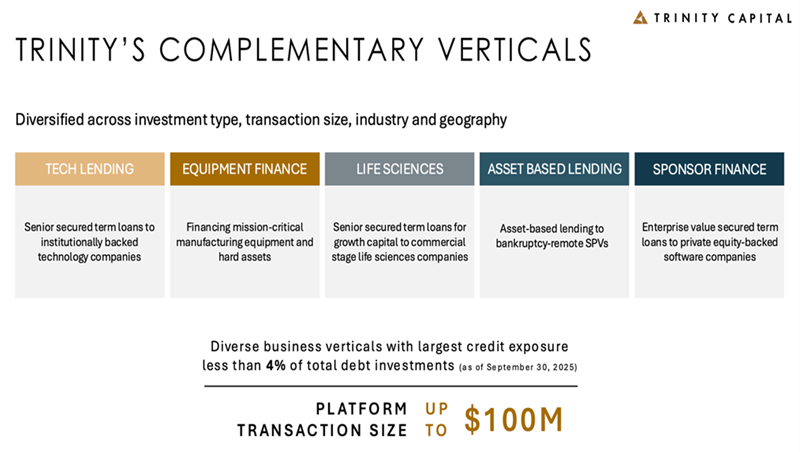

Trinity Capital (TRIN, 13.5% yield) is a growth-focused BDC with a bleeding-edge portfolio of 178 companies including the likes of quantum computing leader Rigetti Computing (RGTI), spaceflight safety firm Slingshot Aerospace, and 3D orthodontics firm LightForce.

TRIN is not only highly diversified in headcount, but also in how it does its deals.

Trinity Capital’s Five-Pronged Model

Source: Trinity Capital Q3 2025 Investor Presentation

Debt is still Trinity’s most prominent investment type, but at about three-quarters of the portfolio at fair value, that’s a smaller allocation than many other BDCs. (Equipment financings make up another 15%, with the rest filled out by equity and warrants.) Floating-rate is also a smaller-than-most share, at a little more than 80% currently.

Trinity is a lot like Sixth Street in that it’s an industry outperformer with good dividend coverage—and a premium valuation, at 14% more than its NAV right now. A silver lining? That’s less frothy than the 22% premium it commanded just a few months ago.

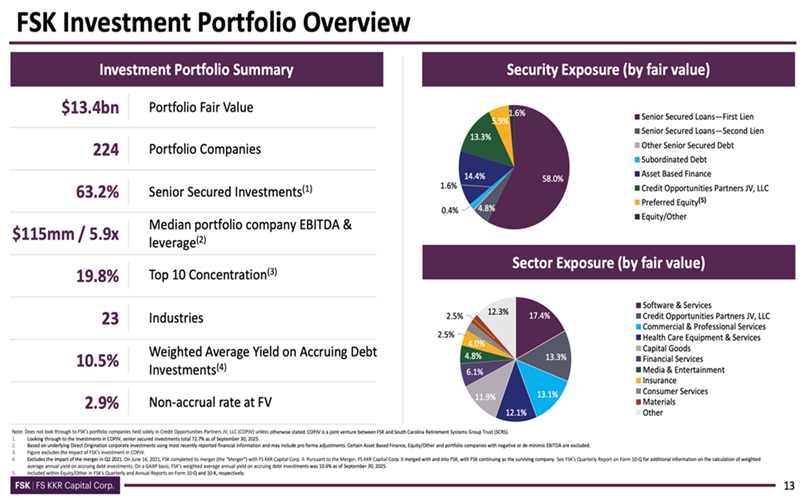

FS KKR Capital (FSK, 14.5% yield) is one of the largest publicly traded BDCs—a $4 billion business funder that can call upon the resources of its managers: alternative investment manager Future Standard and global private equity giant KKR (KKR).

Its portfolio spans 224 companies across 23 industries including software/services, health care equipment/services, commercial/professional services, capital goods, media and more.

This is an extremely diversified portfolio by investment type—debt, which is mostly senior secured (and a little less than 90% floating-rate), is just less than two-thirds of the portfolio at fair value, and it has significant positions in asset-based finance, preferred equity, common equity, and a joint venture, Credit Opportunities Partners JV.

FS KKR Is Happy to Chase Opportunities Anywhere It Finds Them

Source: FS KKR Capital Investor Presentation, November 2025

FSK delivers one of the highest yields in the space and trades at one of the deepest discounts to NAV, at just 69 cents on the dollar. However, FSK would be yielding more if it weren’t for a deep dividend cut.

FS KKR had been paying out a 64-cent base and 6-cent supplemental for nearly two years. Until November, when the company announced a new quarterly distribution “strategy” for 2026 that targeted a 45-cent base. A 30% cut—yikes.

Much of FSK’s problem over the past few years has been bad loans. Non-accruals (loans that are delinquent for a prolonged period, usually 90 days) were a high 5% of the portfolio at cost. Perhaps the portfolio is now “falling out of the basement window” as this actually represents an improvement recently.

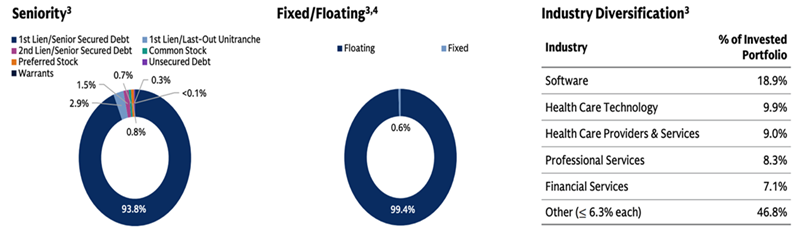

Goldman Sachs BDC (GSBD, 14.7% yield) also cut its dividend in 2025. GSBD’s clear draw is the ability to harness $270 billion global investment bank Goldman Sachs (GS). Its manager, subsidiary Goldman Sachs Asset Management (GSAM), prefers companies with annual EBITDA of between $5 million and $75 million. GSAM has built a portfolio of 171 such companies across a more concentrated dozen industries or so (including software at nearly 20% of the portfolio at fair value).

Source: Goldman Sachs BDC Q3 2025 Investor Presentation

In fact, quality issues—namely high non-accruals (loans that are delinquent for a prolonged period, usually 90 days) and dropping net investment income (NII)—finally forced Goldman Sachs BDC to cut its regular dividend by nearly 30% in February.

Investors skated until recently, when GSBD cut its regular dividend from 45 cents per share to 32 cents starting in Q1. Still, this translates to a nearly 15% yield at current levels.

Goldman Sachs BDC has been a dog since COVID—so much so that its mid-teens yield and 8% discount to NAV don’t seem enticing enough. That said, keep an eye on its portfolio. GSBD continues to shed its legacy portfolio and has become much more aggressive in dealmaking of late.

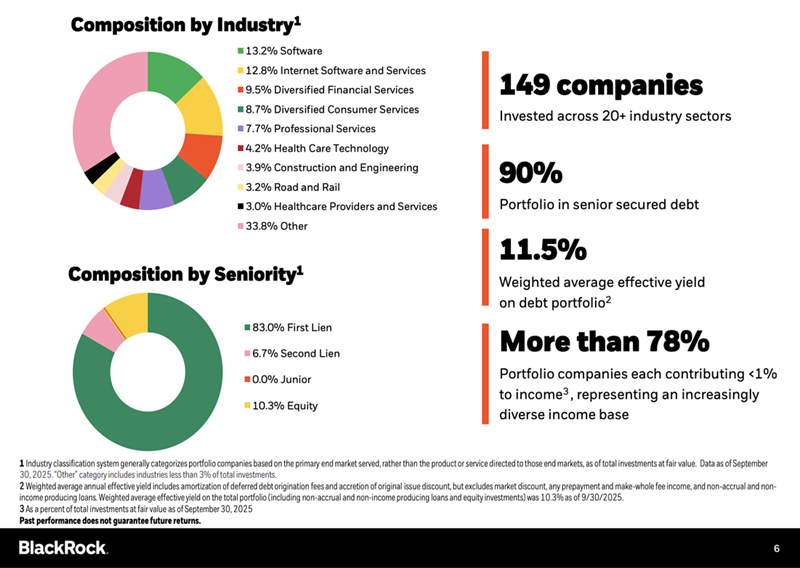

BlackRock TCP Capital Corp. (TCPC, 19.6% yield), managed by BlackRock (BLK) subsidiary BlackRock TCP Capital, invests in companies with enterprise values of between $100 million and $1.5 billion. It currently boasts 149 portfolio companies across more than 20 industries; debt is 90% of the portfolio at fair value, and 94% of those debt investments are of the floating-rate variety.

Source: BlackRock TCP Capital Q3 2025 Investor Presentation

BlackRock TCP Capital says investments may include “complex situations requiring specialized industry knowledge.” That must be another way of saying “challenging,” which would explain TCPC’s struggles of late—since the start of 2023, TCPC has delivered a 30% loss with its massive dividend included while the BDC industry has returned a little more than 40%.

That massive dividend isn’t as big as it was a year ago, though. TCPC cut its dividend by 26% in early 2025, to 25 cents per share. Coverage was better, and it blunted some of that loss with a few specials from Q1 through Q3, but the company recently announced only the base dividend for Q4, which annualized would drop its dividend to closer to 17%. And further rate cuts could put that number in jeopardy.

If we wanted to gamble while BlackRock TCP Capital continues to exit its large non-accruals, we wouldn’t have to pay much to do so. TCPC has been on perpetual discount most of the year, currently priced at just 68 cents on the dollar.

My Can’t-Miss 11% Dividend for 2026

I love the diversification BDCs offer—I just don’t love some of the risk profiles I’m seeing right now.

But what if we could get this kind of diversification from a double-digit-yielding fund …

… that is also poised for stock-like gains in 2026 …

… and unlike these BDCs, it can’t wait for Jerome Powell (or the next Fed chair) to continue hacking away at interest rates?

That’s the exact scenario my “One 11% Dividend to Own Now” is staring down in the New Year.

This fund doesn’t just throw off an incredible 11% dividend—it also has a history of hiking that payout. And this pick’s manager (a top name in the bond world!) regularly throws us special dividends, too!

I call this a “life-changing” yield for a reason. Even a hundred grand invested in this stock would generate $11,000 in annual income. If you could throw $500k at it, this fund would pay you $55 grand per year.

The time to grab a position is NOW while this 11% payer is still at buy-worthy prices. Click here to learn more about this fund, download a free Special Report revealing its name and ticker AND get lined up for its next big monthly payout.

Recent Comments